If there were an award for strongest trending topics in 2021, semiconductors would be among the top contenders. Rightly so, considering their use in so many applications, such as automobiles, wireless communications, personal computers, servers and electromedical and various other digital technologies. As the “smartness” quotient in end-use applications continues to climb, chip demand similarly continues to experience robust growth. The COVID-19 pandemic served to further bolster this momentum, as remote operations of manufacturing and service sectors placed even greater demands on connectivity and digital hardware—to the point where manufacturers began stockpiling chips for the integrated circuits (ICs). In contrast, the just-in-time (JIT) modeled supply chains of the automotive sector froze the procurement of chips during the initial lockdown phases of the pandemic.

As the automotive sector began recovering in the second half of 2020, the industry was forced to compete with other growing end-users of semiconductors, the supplies of which were impacted due to the pandemic-fueled factory shutdowns in countries like Malaysia. Even after chip manufacturing operations resumed in Q4 2020, supplies failed to keep up with the burgeoning demand—despite the maximization of utilization rates of global manufacturing assets. Unfortunately, industry pundits do not expect the situation to be resolved anytime soon.

Automotive electronification

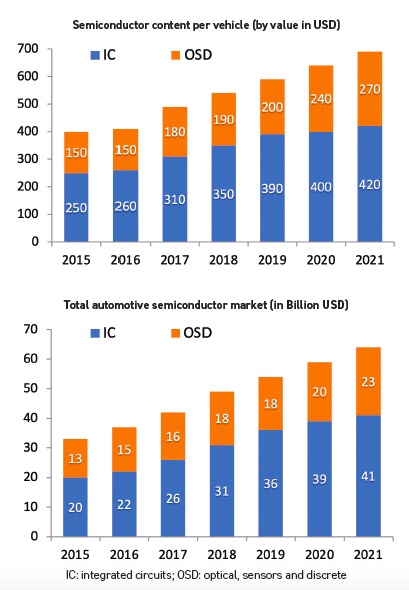

Over the last two decades, original equipment manufacturers (OEMs) have been working relentlessly toward transforming their automobiles from primarily mechanical machines to electronic devices. Integration of electronics in the vehicle hardware, like the drivetrain; controllers; infotainment; autonomous, connected, electric and shared (ACES) mobility; and safety systems—for expanding the vehicle functionality and optimizing performance and safety, while complying with emission norms—necessitated the increased use of semiconductor chips. This trend is apparent from the growing content of semiconductor chips in automotive electronics over the last five years

(see Figure 1).

Figure 1. Historical growth of semiconductor content per vehicle. Figure courtesy of IC Insights.

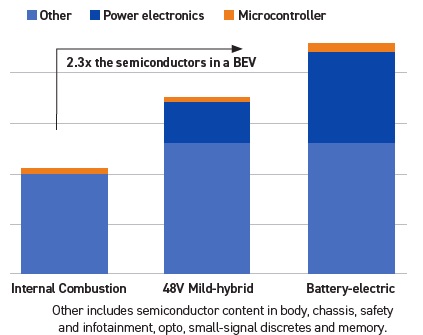

Further, growing penetration of battery electric vehicles (BEVs) and hybrids—which incorporate a greater number of integrated circuits and sensors and, consequently, higher semiconductor content—will further amplify the stress on the chip supply chains

(see Figure 2).

Figure 2. Average car semiconductor content by powertrain ($). Figure courtesy of Infineon.

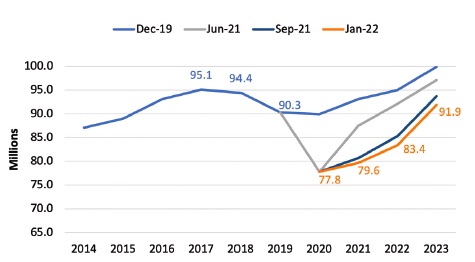

Despite the strong recovery in demand, automotive production has been severely impacted by the unavailability of chips, with many global and regional OEMs announcing production cuts or complete shutdowns of select assembly plants. LMC Automotive forecasted a decline of 8% in light vehicle sales in 2021. Further, due to the expected longer recovery path, light vehicle sales for 2022 and 2023 also have been revised downward, by 8% and 3%, respectively. These developments will have a profound impact on the entire automotive value chain. According to AlixPartners, a consulting firm, the semiconductor chip shortage led to a loss of about $210 billion for the global automotive industry in 2021

(see Figure 3).

Figure 3. Forecast for light vehicle sales. Figure courtesy of LMC Automotive.

Impact on the lubricant industry

Looking forward, the lubricant industry will not be immune to changes in the automotive industry; both automotive and industrial lubricants will be adversely affected. This will have strong implications for the lubricant suppliers, against the backdrop of changes in customer ambitions, preferences and buying considerations.

On the B2B front, the volumetric impact on factory fill volumes for engine oil, transmission fluids, grease, coolants and other lubricants will be immediate and certain due to its direct correlation with automobile production. In addition, the demand for factory maintenance fluids and metalworking fluids (MWFs) in assembly plants and auto-component manufacturing facilities will be gradual and uneven—depending on the structure, operations and maintenance and supply chains of OEMs and auto-component manufacturers.

Typically, the production line is comprised of a complex integration of many rotating pieces of equipment and machines, ranging from CNC machine tools to hydraulic and geared motor systems to compressors to robotics. Based on the operation, manufacturers use a combination of central lubrication reservoirs and isolated sumps for lubricating equipment. Low utilization or partial shutdown of the plant does not directly translate into a clear, measured decline in demand for factory maintenance fluids or MWFs. In the case of the latter, calculations for modeling the impact are more complex due to defined shelf life, which is governed by biological activity and individual company practices/processes for producing machined parts. Among MWFs, the impact on straight oils and premium water-miscible removal and forming fluids will be relatively easily to decipher due to higher application-specific end-use and independent reservoirs. The impact on conventional MWFs might vary depending on the auto-component supply chains and sourcing models of the OEMs. Preventive and treating fluids will be impacted to the extent of their exposure in the metal auto-components industry and mandates issued by automotive OEMs to the component suppliers for fluid use.

Trends in the automotive industry will have a cascading impact on the upstream raw material industries, like metals, rubber and plastics, where the demand for general industrial oils and process oils will be affected. Further, the slowdown in the processing industries will have a direct impact on the extraction industries, like mining, refining and petrochemicals, where the lower utilization rates will affect the consumption of the various lubricants used in both stationary and mobile rotating equipment.

On the B2C front, the implications will be broader. The longer wait times, along with rising input costs, including fuel, will have repercussions on the market for new automobiles and the aftermarkets. All these factors will play on the customer’s mind, resulting in contraction of the pool of new buyers, or buyers being forced to compromise on their original purchase aspirations, i.e., selecting either a pre-owned vehicle, or a low-tiered model of the OEM, or choosing a different OEM in the same vehicle category. These changes will all impact the demand for automotive lubricants—volumetrically and qualitatively. Sales of light-viscosity premium engine oils like 0Ws and 5Ws will be impacted as customers opt for heavier and economical grades of engine oils, while maximizing the life of their new vehicles or newly acquired used ones. Similarly, the use of premium greases utilized in fill-for-life components and in transmission fluids will be affected.

Channel volumetric flows also will not be immune to these changes. OEM dealerships will suffer losses in their service business or will experience a dispersion of the in-warranty vehicle footfalls as customers shift their OEM preferences for purchase of new vehicles, depending on the waiting period. The used-car market also is experiencing structural shifts in many regions, with the rapid expansion of the organized business, along with the ratio of new-vehicle sales versus preowned vehicles increasingly skewing toward the latter. The IWS channel will clearly benefit from the growth in average life of the vehicles due to this short-term trend. Further, as the business models of used-vehicle providers mature, they will expand their value-added services, including vehicle maintenance and services to customers, which will emerge as an important channel for lubricant sales.

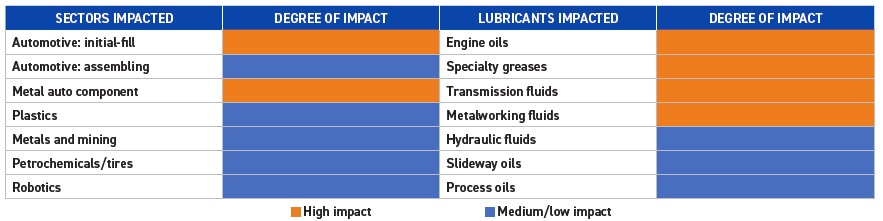

Table 1. Relative impact on lubricant consumption

Table 1 provides a simplified view of the impact the semiconductor shortage will have on lubricant consumption in various end-use sectors, along with the type of lubricants impacted. The scale and length of impact for lubricants will vary depending on the structure and profile of the customers that comprise the end-use sector, the operational and sourcing practices and, ultimately, the business exposure to the automotive value chain.

This article is adapted, by permission, from Kline & Company, Inc. To read the original article, visit www.klinegroup.com.

Satyan Gupta is a director in the Energy sector for Kline & Company based in India. You can reach him at satyan.gupta@klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries including lubricants and chemicals. Learn more at www.klinegroup.com.