China is striving to become a world leader in sustainability and smart manufacturing; its efforts will drive the growing demand for higher performance lubricants and total equipment management services. This, in turn, will help modernize and optimize the enormous manufacturing hubs in China.

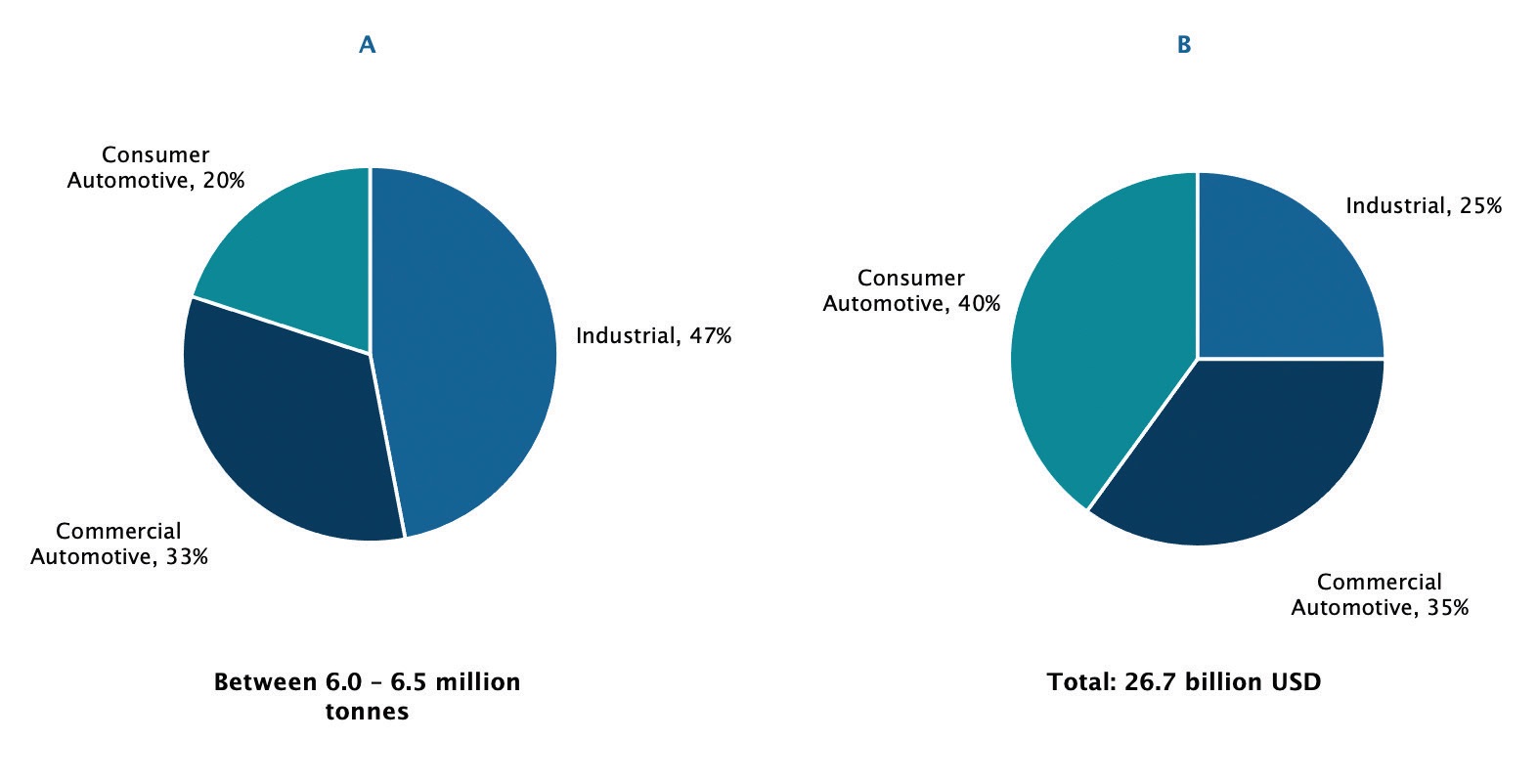

China is the world’s second-largest market for finished lubricants, consuming nearly 7.5 million tonnes of lubricants annually prior to the COVID-19 pandemic. However, the pandemic’s impact on nations, economies and businesses resulted in Chinese lubricant demand declining by almost 13% in 2020. This was nearly a million tonnes drop in demand for finished lubricant across all of the consumer, commercial and industrial lubricants segments (

see Figure 1).

Figure 1. (a) Sales volume of lubricants in China by sectors, 2020. (b) Sales value of lubricants in China by sectors, 2020. Figure courtesy of Kline & Company.

Figure 1. (a) Sales volume of lubricants in China by sectors, 2020. (b) Sales value of lubricants in China by sectors, 2020. Figure courtesy of Kline & Company.

Finished lubricants demand growth has traditionally followed GDP growth, and China’s GDP growth had witnessed a slow decline prior to the COVID-19 pandemic, though it was still a healthy 6.1% GDP in 2019. In 2020, China’s GDP growth did decline due to the pandemic; however, it was still the only major economy to achieve positive growth that year, increasing by 2.3% GDP. Growth is estimated to reach 8.4% in 2021 by the International Monetary Fund (IMF) as the economy rebounds from 2020. Thereafter, growth will achieve more normal rates. These trends and projections should drive a healthy rebound in China’s overall lubricants market. However, the pandemic, along with government policies, is going to drive lubricants growth in a different direction than indicated by historical performance.

In the past, China’s lubricants market has experienced strong volume growth, though that growth often came from mid- to lower-tier lubricants products, and the customer base was very broad, with many small businesses served by local distributors. This was especially true for the industrial lubricants segment, which is the largest segment by volume. This, however, is shifting toward slower lubricants volume growth despite the projected economic recovery.

Trade wars between China and the U.S. had driven the Chinese government to shift its economic growth plans away from an export-driven economy to one focused on building domestic consumption and improving the value of its export market through modernization and consolidation in its industrial segment. From 2021 to 2025, China will be starting its 14th Five-Year Plan, which aims to increase domestic consumption, modernize the supply chain in major industries, improve innovation capabilities and enhance sustainability and environmental protection while developing the economy. Based on such a plan, China’s economic structure will be transformed from export driven to both domestic and export driven, from simple manufacturing to smart manufacturing, from producing general parts to producing core parts and from an emissions producer to a more environmentally friendly nation with a sustainable future. To accomplish this, the Chinese government is heavily investing in modernizing its industrial segment and phasing out much of the outdated capacity across various industries.

The pandemic has helped accelerate those plans as the economic slowdown from the COVID-19 pandemic helped drive out many smaller producers, which tended to use outdated, inefficient equipment that produced more emissions and environmental pollution.

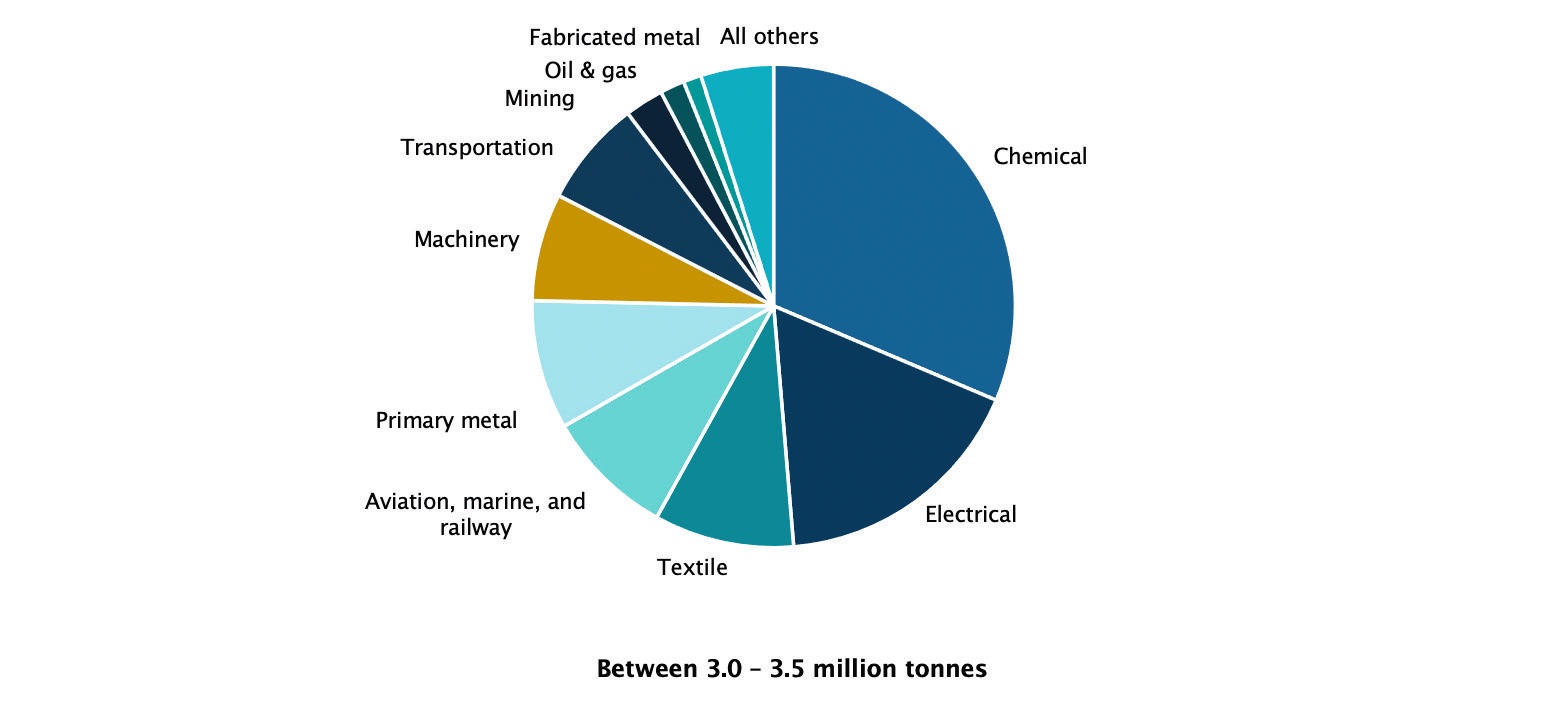

Chemicals is the largest industrial lubricants segment, consuming nearly one-third of industrial lubricants (

see Figure 2). This segment has seen a decline of over 5% in the number of businesses, though it currently still has over 55,000 participating businesses. Chemical and materials manufacturing in China is one of the most mature industrial sectors in the country. However, it also is one of the most energy-intensive sectors and generates pollution. This sector has faced environmental and overcapacity issues for quite some time. With the launch of a series of refinery projects nationwide, the production capacity for chemicals, including aromatic hydrocarbon, methanol and ethylene, is expected to expand further.

Figure 2. Sales volume of industrial lubricants in China by applications, 2020. Figure courtesy of Kline & Company.

Figure 2. Sales volume of industrial lubricants in China by applications, 2020. Figure courtesy of Kline & Company.

In 2020, over 65% of newly added chemical material capacity worldwide was in China. Although the consumption of chemicals is expected to keep growing slowly over the coming years, driven by downstream demand, the sector is expected to witness industry upgrades along with the elimination of outdated capacity. In other areas such as paint, ink, sealants and related products, the government continues to push for lower volatile organic compounds release, which will cause manufacturers to shift toward more environmentally friendly solutions, such as water-based products. The green push by the government not only refers to more environmentally friendly manufacturing processes but also to more environmentally friendly products, particularly in the pharmaceutical and cosmetics industries. This will drive a change in the type and quantity of process oils consumed by this segment.

Traditional heavy-duty industries, such as primary metals, mining, machinery and auto manufacturing, will incorporate smart manufacturing technology, and sustainability will become a very important requirement in industrial development.

The drive toward sustainability is most prevalent in the industrial segments, where the government continues to set up smart mining or manufacturing facilities to showcase the possible future and frames regulations that force businesses to upgrade old equipment toward modern, more efficient and often connected equipment. This will drive the upgrade in industrial lubricants performance as well as value-added services, such as monitoring the data streaming from all of the connected equipment and providing both cost-efficient as well as environmentally friendly lubricants service plans to maintain this equipment. This will drive further industry consolidation as smaller businesses often cannot afford to upgrade, nor do they have the scale to justify using the largest and most modern equipment. This also will affect how lubricants marketers reach their customers, as small businesses often preferred local distributors while larger companies prefer to buy directly from lubricants marketers. Greater volumes of direct sales will require lubricants marketers to shift toward a more hands-on approach to sales and support, while smaller distributors may need to transition toward logistics and warehousing.

In the automotive lubricants segment, China is driving rapid modernization of the vehicle parc as it implements its National VI emissions standards, based on Euro VI. China’s implementation of these new emissions standards phases out older, non-compliant vehicles, which either need to be sold to regions outside of Tier 1 and Tier 2 cities or sold to neighboring countries, as China’s strict policies will not permit non-compliant vehicles to be registered. The COVID-19 pandemic, however, has driven some growth in vehicle sales as the population seeks to avoid using mass transit in favor of safer ways of travel. While these trends do mean that vehicle parc growth will be slow, as much of the new vehicle sales are for replacing older vehicles, it also means the lubricants upgrade in the automotive segment will continue at a rapid pace. Commercial vehicles production, led by surging demand for trucks, grew by 20% to reach 5.2 million units. Sales also increased by 18.7% and reached 5.1 million units in 2020. The segment reached the record-high performance to exceed five million units in production and sales for the first time. It is mainly aided by growing fixed asset investment, the phaseout of National III vehicles and policies to tackle overloading issues, which drives a substantial growth for trucks. This also means growth in electric vehicles (EVs) will continue at a faster pace in China, especially given that China is aiming to become the global EV leader.

Overall, the lubricants market in China is heading toward quality levels similar to those in Europe and North America while placing a greater emphasis on sustainability. China’s lubricants market has weathered the pandemic well despite losses and is projected to grow at more than 1% CAGR until 2025. However, that slow growth will be led by growth in premium lubricants as the country modernizes at a breakneck pace.

This article is based on Kline’s recently published study, “Opportunities in Lubricants: China Market Analysis and Opportunities.” Learn more here.

David Tsui is a project manager at Kline & Co. in the Energy practice. You can reach him at david.tsui@klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries that include lubricants and chemicals. Learn more at www.klinegroup.com.