Market developments in India point to rapid electrification of the two-wheeler vehicle parc. Why is this happening, and what does it mean for the motorcycle oil (MCO) market? In this article, we will try to answer these questions.

The Indian lubricants market is the third-largest in the world. Within it, MCO accounts for 9% of total demand, making it the third-largest product category behind process oils and heavy-duty motor oils (HDMO). Among all lubricants product categories, MCO was one of the least impacted by the COVID-19 pandemic and one of the fastest to recover. According to current estimates, the MCO market is growing at 3.7% per year, making it one of the most attractive product segments for lubricants marketers. Growing electrification will change that and create new challenges for market participants.

Two-wheelers mainstay of personal mobility in India

Two-wheelers are one of the most important and easiest modes of transportation in urban as well as rural India. Motorcycles are the most popular type of two-wheeler used, followed by scooters and mopeds. While the share of mopeds in the two-wheeler parc is shrinking, the share of scooters is growing rapidly. In India, two-wheelers are primarily used for transportation (personal commute). Most two-wheeler owners use their vehicles to commute to their place of work. Business activities are the second-largest in-service activity in the two-wheeler market. Businesses such as food and goods delivery services, as well as mail and courier services, extensively use two-wheelers. Two-wheelers also are used as bike taxis and self-drive rentals, which is a growing business segment. There is a niche market that uses two-wheelers primarily for recreational purposes.

Due to the importance of two-wheelers for personal mobility, India is the largest market for these vehicles in terms of sales and population. Two-wheelers dominate automotive sales with more than 80% of annual sales across personal mobility and heavy-duty vehicles. Leading two-wheeler OEMs include Hero, Honda, TVS, Bajaj, Suzuki, Royal Enfield, Yamaha, Mahindra and Vespa. Some of the brands operating primarily in the premium two-wheeler market are Kawasaki, Harley Davidson, Triumph, BMW, Indian Motorcycle and KTM.

Electric two-wheelers gaining ground

Support from the government has been pivotal in pushing the sales of electric two-wheelers. Faster Adoption and Manufacturing of (Hybrid &) Electric Vehicles (FAME) is a scheme to promote electric vehicle (EV) adoption in India. The FAME 1 scheme, which operated from Financial Year (FY) 2015-2016 to FY 2018-2019, supported both slow-speed and high-speed electric two-wheelers. However, FAME 2 (FY 2019-2020 to FY 2021-2022) has a budget outlay to incentivize a million electric two-wheelers that are high speed and use batteries with advanced chemistry. Due to increased technical specifications in FAME 2, the incentivization has helped only about 10% of electric two-wheelers sold to date during the period. This has resulted in utilizing only about 5% of the budgeted outlay, even as two-thirds of the scheme period has elapsed.

In June 2019, the Indian government proposed banning sales of two-wheelers under 150cc cylinder capacity after March 2025 and allowing sales of electric two-wheelers after this time as part of its bid to promote a rapid transition toward electric mobility in India. Under 150cc cylinder capacity, motorcycle sales account for just under 100% of two-wheeler market leader Hero MotoCorp’s two-wheeler sales and 83% of Bajaj’s sales. If this ban were to proceed, these OEMs would be forced to electrify.

The Indian government slashed goods and service tax (GST) on EVs, from 12% to 5%, in July 2019 to promote EVs in the country; this translates to a price reduction of $110 to $137 (INR 8,000 to INR 10,000). GST also was slashed on EV chargers, from 18% to 5%, in 2019. Another step taken by the government to make EVs even more affordable for the Indian consumer includes an income tax deduction of $0.02 million (INR 1.5 million) on the interest paid on loans taken to purchase EVs. Additionally, low-speed electric two-wheelers are exempt from registration. Several state governments in India have offered waivers on road tax and registration fees for electric two-wheelers.

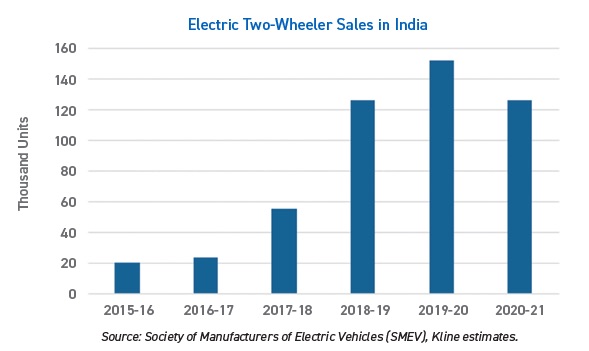

Helped by all these measures, sales of electric scooters have been growing rapidly despite the COVID-19-induced decline in 2020-2021 (

see Figure 1).

Figure 1. Sales of electric scooters have been growing rapidly despite the COVID-19-induced decline.

Figure 1. Sales of electric scooters have been growing rapidly despite the COVID-19-induced decline.

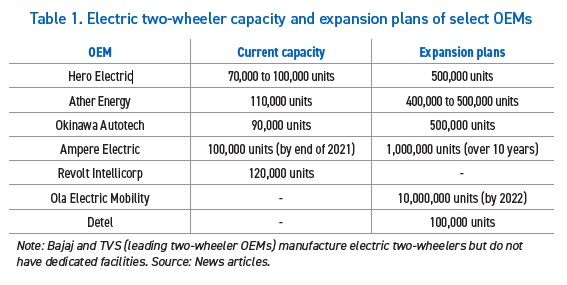

Encouraged by the growth from the favorable tax and regulatory environment and the growth in sales, many OEMs have announced plans to expand their production capacity (

see Table 1).

EV charging strategy Indianized

EV charging strategy Indianized

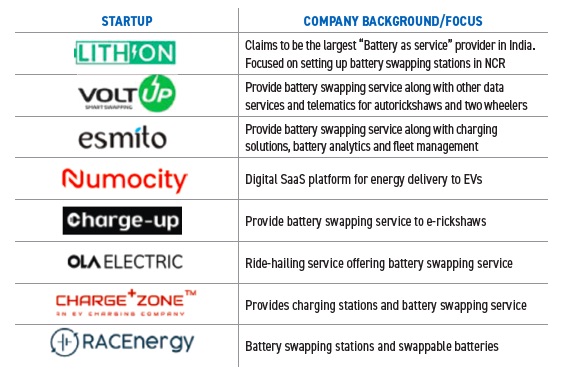

One of the oft-cited issues with EV growth in India is the poor electricity grid infrastructure and paucity of charging stations. Many power companies as well as oil companies have announced plans to develop charging infrastructures in the country. The Indian government plans to make battery swapping a key component of electric two-wheeler charging, simultaneously addressing two issues: the lack of charge points and the long charging time. In August 2020, the Ministry of Road Transport and Highways announced that it would allow the sale and registration of EVs without batteries.

1 Figure 2 shows the latest in a series of Indian government policy signals favoring battery swapping. This has led to a growing roster of startups in this space.

Figure 2. Select electric battery swapping service startups in India.

Figure 2. Select electric battery swapping service startups in India.

Even OEMs, oil companies and e-commerce companies are getting into this business. Four two-wheeler OEMs—Honda, KTM, Piaggio and Yamaha—have formed a consortium for swappable batteries.

2 Jio-bp, the mobility joint venture between Reliance Industries and BP, is conducting a pilot program for battery swapping for electric autorickshaws and has bigger plans in this area.

3 Zypp Electric has partnered with grocery, e-retail and food tech players such as BigBasket, Grofers, Modern Bazaar and Spencers.

4

Evolvement of two-wheeler vehicle parc

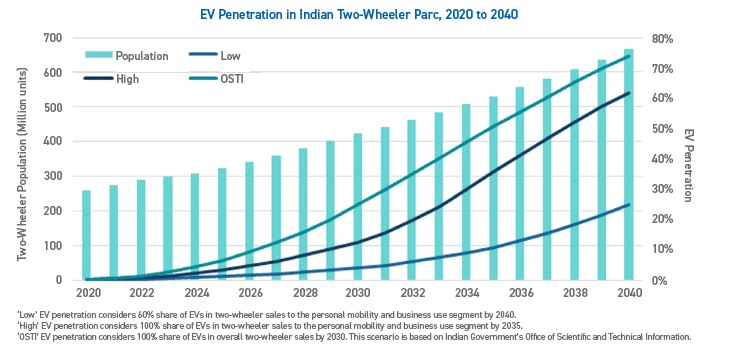

The two-wheeler vehicle parc will undergo a sea change due to all the factors described above. Kline anticipates rapid penetration of electric two-wheelers propelled by several stakeholders—government, OEMs, energy companies offering battery swapping/charging facilities and end-users (both for business and personal use). Under the three scenarios analyzed, EV penetration could grow between 25% and just under 75% by 2040. For comparison, the current penetration of EVs is effectively 0% (

see Figure 3).

Figure 3. EV penetration could grow between 25% and just under 75% by 2040.

Figure 3. EV penetration could grow between 25% and just under 75% by 2040.

Does this projection look overly optimistic for EVs? Will the Indian two-wheeler parc undergo such drastic change in 20 years? Consider the following: Between 2001 and 2021, the two-wheeler parc in India grew at a compound average growth rate (CAGR) of 10%. The forecast here projects a lower CAGR for the coming 20 years of under 5%. In 2021, two-wheeler penetration in India stands at 202 vehicles per 1,000 people. In contrast, Indonesia has a penetration of 420 vehicles per 1,000 people. The projection assumes that India will achieve this penetration by 2040.

Will the share of EVs in the total population reach the levels shown here? More than 150 million EVs will have to be added in the low scenario. To achieve this, the manufacturing capacity will have to ramp up significantly in the next few years. If all of the expansion plans noted previously materialize, EV manufacturing capacity in India will exceed 12 million units per year by 2022. The expansion plans noted above do not include leading two-wheeler OEMs such as TVS and Bajaj, which also enter this market with dedicated production lines. EV assembly line capacity might not be a big issue. The bottleneck might be having sufficient battery capacity to support battery swapping.

On the demand side, pricing, features and the green tag can motivate a diverse customer base to use EVs. Most EVs offered are priced in the economy range with a price point of popular models ranging from INR 40,000 ($550) to INR 120,000 ($1,650) with only a few exceeding this price range. This makes EVs eminently affordable to much of the population. EVs are particularly attractive to young consumers, as low-speed EVs do not require registration or a driver’s license. EVs also are particularly attractive for last-mile delivery to various e-commerce and food delivery companies, due to low operating costs and the ability to demonstrate their commitment to sustainability. Battery swapping offers a convenient charging process, which increases the attractiveness of EVs.

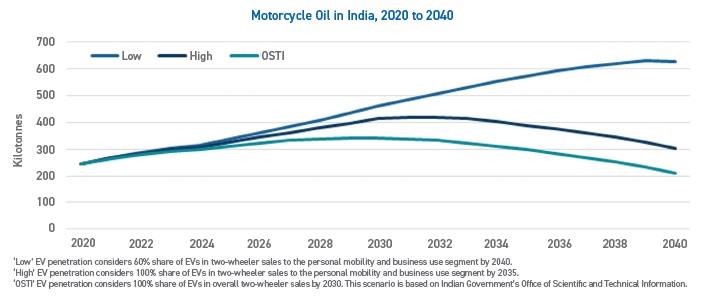

Motorcycle oil demand

The change in the two-wheeler parc composition will be reflected in the changing demand for MCOs. Depending on the scenario, MCO demand will peak between 2030 and 2040 (

see Figure 4). Two-wheeler maintenance is a huge industry involving both organized and unorganized channels. While spare part sales are an important aftermarket segment, lubricants are equally important. Lubricants used in two-wheelers include MCO, gear oil, fork oil, rear suspension oil, grease and chain oil. Given the size and growth in this market segment, MCOs attract special focus from most lubricants suppliers looking to grow or maintain their market share. Some of the leading suppliers of MCOs, to OEMs and aftermarket in India, are BP, NOCs (IOCL, HPCL, BPCL), Savita Oil and Gulf Oil with their brands Castrol, Servo, HP, MAK, Savsol and Gulf, respectively.

Figure 4. MCO demand will peak between 2030 and 2040.

Two-wheelers electrification opportunities and challenges

Figure 4. MCO demand will peak between 2030 and 2040.

Two-wheelers electrification opportunities and challenges

Industry participants, including OEMs, oil companies, retail and installer channel partners, are waking up to the change that seems imminent. While the OSTI scenario looks overly optimistic for EVs, it is inevitable that MCOs demand will see a peak within the next 10 to 20 years. That gives industry participants enough time to create a position in the EV market from maintenance to battery swapping and other services. In the short-term, oil companies will have to fight hard to retain MCO market share. OEMs are expanding their offerings of genuine oils in a bid to retain customers and engender loyalty with an eye toward future vehicle sales. EV maintenance requirements are lower than ICE vehicles, but they are not non-existent. Market participants have to focus on these, along with providing charging infrastructure/battery swapping services to stay relevant.

REFERENCES

1.

Click

here.

2.

Click

here.

3.

Click

here.

4.

Click

here.

Milind Phadke is vice president of Kline & Co.’s Energy practice. You can reach him at Milind.Phadke@klinegroup.com.

Hareesh Nalam is senior manager (Energy) for Kline & Co. You can reach him at Hareesh.Nalam@Klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries that include lubricants and chemicals. Learn more at www.klinegroup.com.