The original equipment manufacturer franchised workshop (OEM FWS), or dealership channel, is a key channel for lubricant sales, with volumes in some countries surpassing the independent workshop (IWS) channel. While traditionally this channel mainly has catered to newer vehicles and warranty service, it has steadily expanded its customer base into out-of-warranty vehicle owners, fleets and even into the IWS and fast-fit space.

Growth drivers in the OEM FWS channel over the IWS and fast-fit channels are a result of several factors. First, there is greater OEM and dealer investment in retaining customers in after-sales service. Second, legislation around emissions and fuel economy has made new vehicles more complex and expensive, which tends to bring consumers back to their dealers even when the vehicle is out of warranty. Third, consumer views of vehicles also are shifting in mature markets, where vehicles become more of a means of conveyance and less of a persona.

The main growth driver of the OEM FWS channel is increasing OEM and dealership investment in growing after-sales service market share. This is due to declining profits on new vehicle sales, as vehicle pricing has become much more competitive and transparent with internet pricing data. This has hurt overall dealer-ship profitability and is causing dealers and their OEMs to rely on after-sales service to improve profitability for both. There are several ways this is being done: through advertising campaigns, loyalty programs, complimentary maintenance, investments in phone apps and even venturing into the quick-lube/fast-fit channel, among others.

Ford has invested in an advertising campaign for “The Works” package on behalf of its dealers; it is a complete oil change, tire rotation and vehicle inspection offer at pricing competitive to local IWS chains. Dealers have been trying to shed the belief that their service is always more expensive than the IWS channel and local garages and quite often offer a competitively priced conventional oil change. Ford has also launched its FordPass Rewards program, which was designed in cooperation with companies well-versed in customer loyalty such as Marriott and JetBlue. This demonstrates how seriously Ford is taking customer retention.

Meanwhile, Hyundai has launched its own complimentary maintenance program, which offers new vehicle owners three years or 36,000 miles of free maintenance, which, at current drain intervals, gives customers six free oil changes. While complimentary maintenance would seemingly go against improving profitability, it promotes increased customer contact, during which dealership staff can build a relationship and improve customer loyalty. This loyalty tends to translate into additional service on older vehicles as well as future new vehicle sales.

Volvo has perfectly timed its Volvo Valet app and service, which launched just prior to the COVID-19 pandemic and has helped provide customers with pick-up and drop-off service from its dealership network and has helped maintain dealership traffic throughout the shutdowns. Some OEMs also have begun tentatively venturing into the quick-lube and fast-fit chain, as many North American OEMs now have dedicated quick lubes either attached to their dealership or as a stand-alone. Asian OEMs also have followed suit with their own fast-fit chains to help expand their network and reach customers. This foray into somewhat unknown market territory exemplifies OEMs’ desire to expand their market share of the after-sales service market on their vehicles.

The vehicles themselves have become much more complex as they try to meet increasingly stringent emissions and safety regulations. Vehicles are offered with technology such as advanced valvetrains, variable displacement, cylinder deactivation, stop-start and many other features designed to improve fuel economy and reduce emissions, with OEMs often proceeding in different directions. This has made vehicle service more difficult for IWS and fast-fit chains, which might not have access to the latest OEM software for vehicle diagnostics. Consumers in mature regions have been shifting back to the OEM FWS channel, as seen first in Europe but also in North America and some parts of Asia. The trained OEM certified technician becomes the primary choice for service and maintenance for these advanced vehicles. This also is being aided by the OEMs, with proprietary features that make do-it-yourself (DIY) and IWS service and maintenance more challenging, as only the OEM has access to some of these tools.

Consumer behavior in mature markets also is driving this return to dealerships for service. Growing MSRPs on new vehicles with their advanced emissions technology often mean longer loan payoff periods and greater financial impact, which tends to drive consumers to favor dealerships. Ridesharing services also are reducing the importance of vehicles to younger consumers, as vehicle ownership no longer is required to have the freedom that young adults seek. To them, vehicles simply become a means of travel, and they no longer have a connection to vehicles and take pride in caring for and maintaining them. This reduces their desire for DIY maintenance as well as their desire to select the lubricant for their vehicle, often relegating the choice to the OEM-recommended fluids if they own a new vehicle.

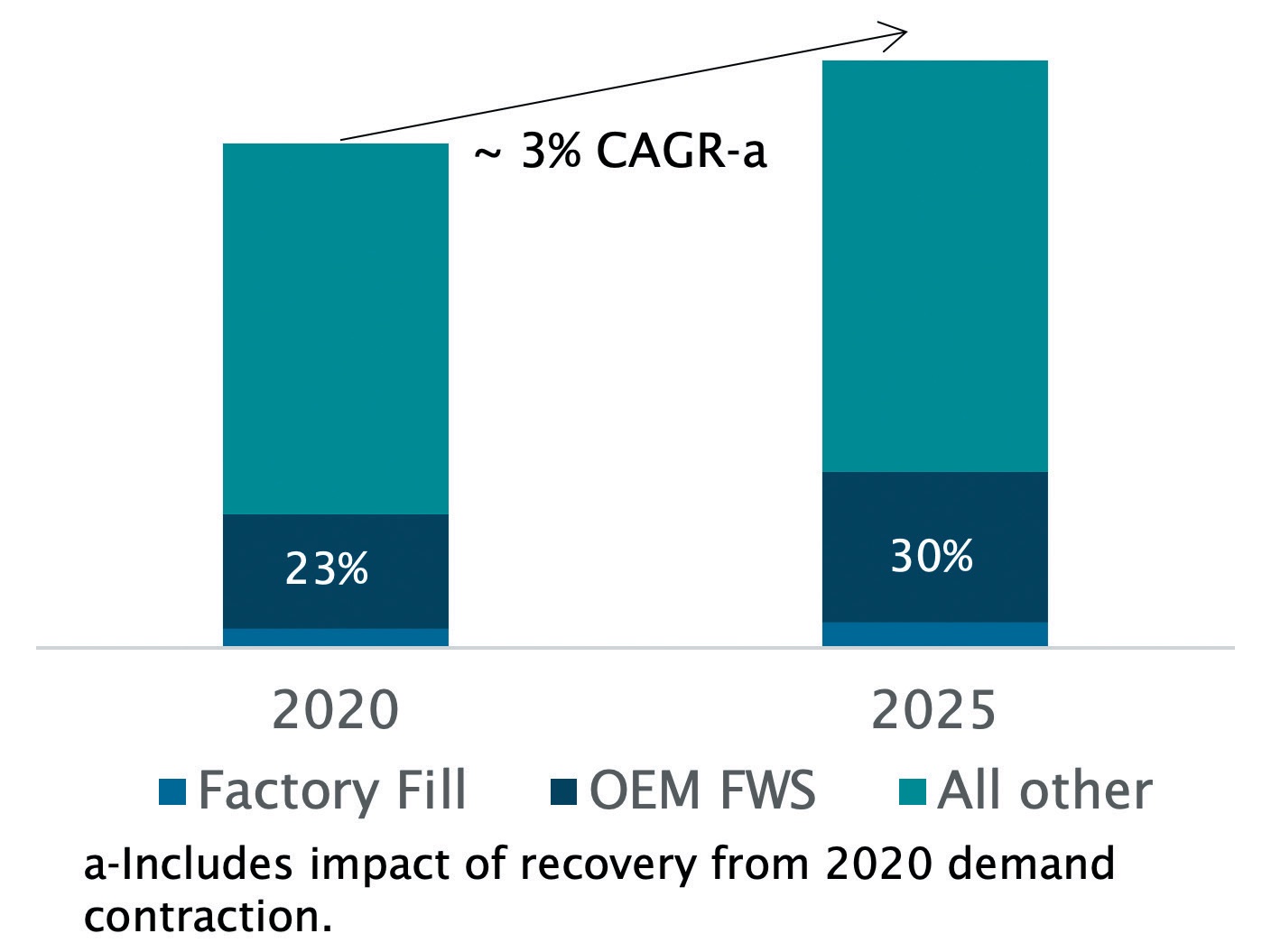

The OEM FWS channel accounts for nearly a quarter of global passenger car motor oil (PCMO) demand in 2020 and is projected to increase at a faster pace than global PCMO growth over the 2020 to 2025 forecast period (

see Figure 1).

Global PCMO Demand, 2020–2025

Figure 1. The global PCMO demand is projected to increase at a faster pace than global PCMO growth over the 2020 to 2025 forecast period.

Figure 1. The global PCMO demand is projected to increase at a faster pace than global PCMO growth over the 2020 to 2025 forecast period.

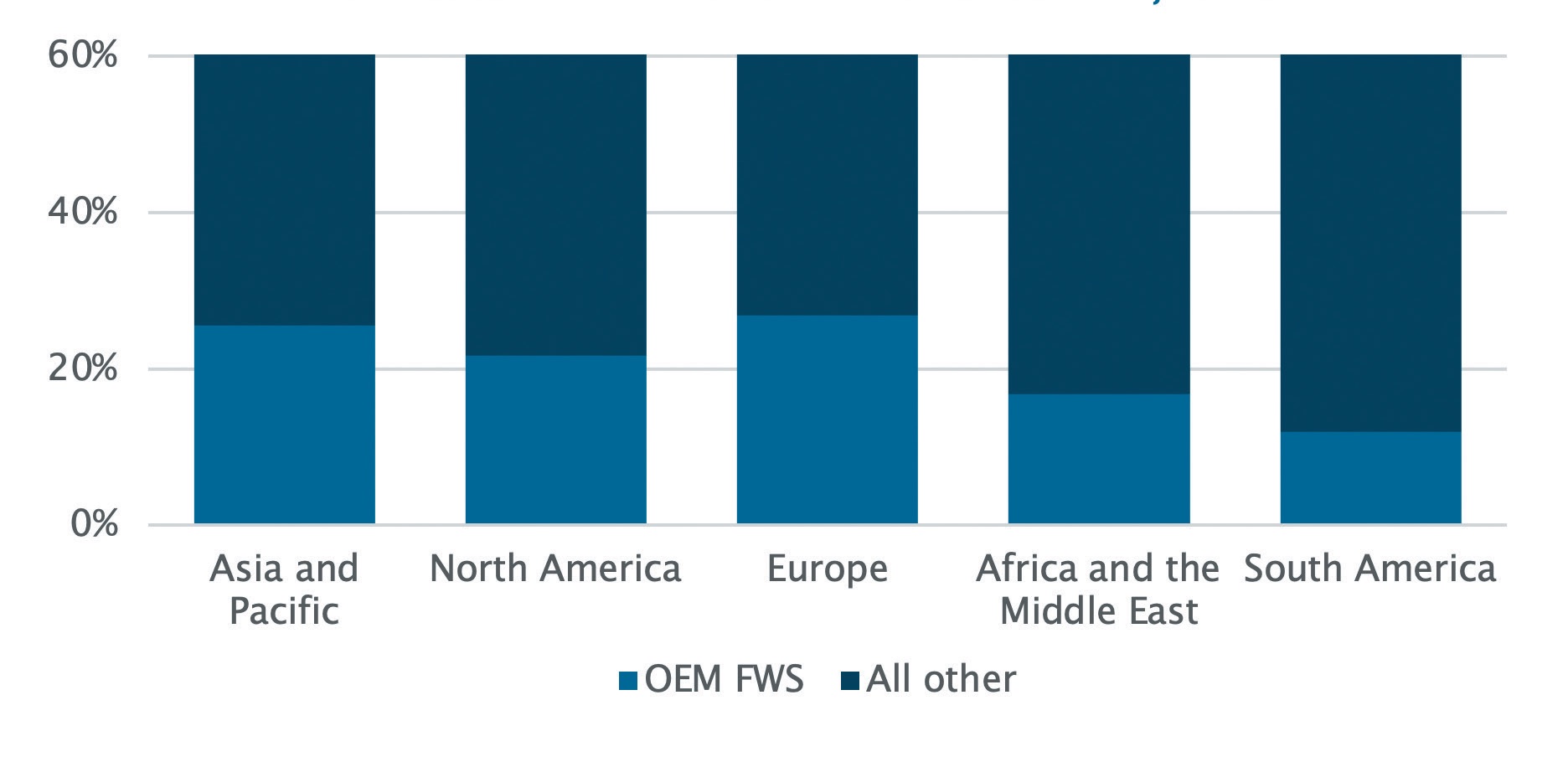

Across the five major regions, Asia-Pacific leads in terms of volume, while Europe leads in channel market share. Asia-Pacific, North America and Europe account for nearly 90% of the PCMO sold through the OEM FWS channel. Consumers in Western Europe have long been migrating back to the OEM FWS channel, and this has continued as OEMs continue to offer the latest specification lubricants, professional service and OEM genuine fluids and parts. This trend is just starting in North America, as consumers who had originally moved to DIY and the vast IWS network begin to return to dealerships that offer more professional service at competitive pricing. Asia-Pacific is rather varied, with consumers leaving the dealership network or returning depending on the country, as cultural differences tend to influence the OEM FWS channel share. Japan, for instance, has a culture of strong consumer loyalty and sees extremely high customer retention rates in its OEM FWS channel, whereas developing nations are seeing the IWS channel grow with customers becoming more confident and migrating away for convenience and cost savings (

see Figure 2).

Regional PCMO Demand By Channel, 2020

Figure 2. Across the five major regions, Asia-Pacific leads in terms of volume, while Europe leads in channel market share. Asia-Pacific, North America and Europe account for nearly 90% of the PCMO sold through the OEM FWS channel.

Figure 2. Across the five major regions, Asia-Pacific leads in terms of volume, while Europe leads in channel market share. Asia-Pacific, North America and Europe account for nearly 90% of the PCMO sold through the OEM FWS channel.

The COVID-19 pandemic also has caused a significant decline in the OEM FWS channel, as PCMO demand is estimated to have declined 18% since 2019 due to the global shutdown. COVID-19 also has created a shift in this service channel. For example, consumers are looking for contactless service and sales and increasingly using phone apps and online service scheduling tools, and dealerships are offering pick-up and drop-off services. The outlook for PCMO sales through the OEM FWS channel is strong for the foreseeable future.

This article draws on Kline’s second edition of the Franchised Workshop Channel in the Consumer Automotive Segment report, which analyzes trends and drivers for PCMO demand in the OEM FWS channel while looking into some of the effects of the global shutdown on the FWS channel and its growth potential post-pandemic.

1

REFERENCE

1.

Click

here.

David Tsui is a project manager at Kline & Co. in the Energy practice. You can reach him at david.tsui@klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries that include lubricants and chemicals. Learn more at www.klinegroup.com.