Globally, China’s passenger car motor oil (PCMO) market ranks second in terms of volume, accounting for approximately 17% of demand. The COVID-19 pandemic has slowed growth, with new vehicle sales declining by nearly 20% in the first half of 2020. This drop, along with reduced annual mileage due to lockdowns, has brought PCMO demand to under 1,000 kilotonnes in 2020, a slip of more than 15% from 2019. Contributing to this slowdown is the growing penetration of battery electric vehicles, which are expected to expand to nearly 20% of annual sales by 2025.

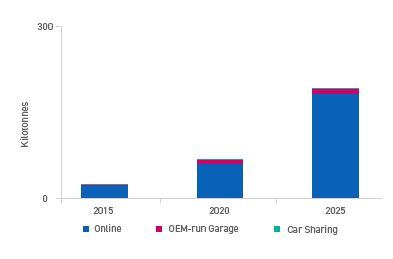

Despite this setback, the Chinese PCMO market is projected to recover and grow over the next five years. While traditional lubricants marketing channels will continue to be the mainstay, new alternative channels are providing opportunities for greater growth as people adapt to a post-COVID-19 world. Currently, alternative channels account for less than 10% of the PCMO market. However, they are projected to double by 2025 as consumers embrace these new means of vehicle services and lubricants procurement. These new channels include OEM garages, online to offline (O2O) and other Internet platforms and car-sharing platforms (

see Figure 1).

Figure 1. PCMO sales growth in alternative channels in China, 2015-2025.

Figure 1. PCMO sales growth in alternative channels in China, 2015-2025.

The OEM garage channel has been growing in China, with nearly a dozen OEMs establishing their own chain of service and repair garages that are distinctly separate from their franchise workshop (FWS) dealers. These smaller facilities typically only provide quick services such as engine oil changes and basic repairs, leaving more entailed work to the OEM dealership service center. They also service more than their own brand of vehicle, but they bring the brand reputation of the OEM into the market, helping them establish brand equity faster. This helps OEMs grow their share of after-sales vehicle service and build customer retention. This is why OEMs have invested in thousands of garages and are continuing to expand their foothold in the market.

Internet platforms such as JD.com and Tuhu have long established a strong foothold in China, and lubricants sales have started to grow. Many major lubricants marketers have formed official stores on these sites, helping customers avoid purchasing a counterfeit product. In addition, prices are typically lower there than at a retail or garage site. Government regulations on counterfeiting will help this channel grow as consumers accustomed to ordering online due to COVID-19 turn to these platforms even more to order everything they need, including service for their vehicles. The O2O channel helps consumers shop prices and brings cost-conscious consumers to local independent garages, as the platform negotiates fees and then sells the engine oil change service (complete with lubricant) to the consumer. The consumer can then choose a local participating garage at which to get their oil changed, prepaying for the service and selecting the lubricant online. This service was already growing pre-COVID-19. Post-pandemic, it is expected to continue rising, especially with stricter anti-counterfeiting regulations coming into effect.

Ride-sharing is quite popular in the country with heavy use in urban areas, though some of its expected growth has been hampered in the short term due to greater vehicle ownership as people concerned about any shared or public transport migrate toward personal vehicles. These ride-sharing companies impact lubricants—for example, when Didi, a ride-hailing company, and other well-established service providers offer their drivers discounted vehicle service, which includes oil changes. These major platforms have reached a large enough size to be able to procure their lubricants directly from lubricants marketers, as their volumes allow for greater discounts, which they can then help provide to their drivers as a bonus while also additional profit for themselves.

The growth in these alternative channels has helped them migrate from lubricant procurement from smaller second- and third-tier lubricant distributors to first-tier distributor or direct sales from lubricant marketers. Third-tier distributors are most likely to lose the greatest volume from this shift, and these distributors will be forced to adapt their business model to more of a logistic-only service, as they will lose some of the lubricant’s sales aspect of their current business.

China has almost 300 million passenger vehicles in its car parc, with sales of around 20 million new vehicles each year. The country also has around 100 vehicle OEMs, which supply both the domestic and regional export market. As a result, the Chinese PCMO market remains a major dynamic market, with recent advances being driven by the pandemic-induced shutdowns. Kline’s study on “The Changing Face of Passenger Car Servicing and Emerging PCMO Sales Channels in China” dives deeper into these changes and identifies opportunities for businesses involved in the lubricants value chain.

1

Recovery in HDMO market by changes in the sales channel landscape

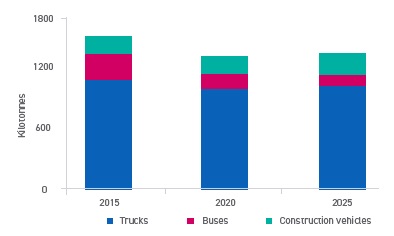

Prior to the COVID-19 outbreak, heavy-duty motor oil (HDMO) demand in the truck and construction vehicles categories was growing due to the booming logistics industry and significant investments in the construction industry. However, the COVID-19-induced lockdown in China in 2020 has severely affected demand for HDMO in the trucks category due to restrictions in the movement of goods as well as reduced demand. The construction industry experienced a relatively less severe impact of the COVID-19 lockdowns, as construction sites in the country regained activity after a brief shutdown period of two months. Therefore, demand for HDMO in the construction vehicle category in China continues to grow. The bus segment in China, which was already declining since 2016, experienced an even steeper decline in 2020 due to reduced travel amidst the COVID-19 outbreak. Highway passenger traffic in the country dropped by over 50% in the first half of 2020 over the same period in 2019, thus resulting in lower operating rates and a drop in HDMO demand by the bus segment in China (

see Figure 2).

Figure 2. HDMO sales trend in China for trucks, buses and construction vehicles, 2015-2025.

Figure 2. HDMO sales trend in China for trucks, buses and construction vehicles, 2015-2025.

Despite a significant drop in demand for service-fill HDMO by the truck category in China in 2020, the demand for engine oils is expected to recover, albeit partially driven by growth in truck sales and population. Implementation of stricter emission standards, such as National VI Standard, is expected to be launched in 2021 and drive sales of new trucks in the country. Medium and heavy trucks are likely to experience annual growth in sales between 1% and 2%, while light and mini trucks are likely to experience slightly slower growth over the next five years. This is expected to result in growth of truck parc size in the country, translating into growth in HDMO sales. However, this growth will be dampened by the penetration of premium (API CK-4/CJ-4 category) long-drain interval engine oils.

The sales channel landscape, however, is changing among the truck and fleet owners in China. A growing number of truck fleets are shifting toward in-house garages for maintenance, which is expected to result in a considerable loss in customer footfall in the independent workshop (IWS) channel, which currently accounts for nearly half of the total engine oils sales in the truck category. The FWS channel, which is the second-place holder for HDMO sales, is likely to continue gaining share in the aftersales market. As new trucks adhering to National VI Standard become popular, an increasing number of truck owners might seek professional maintenance services offered by FWS instead of visiting IWS, which typically are less competent in servicing new technology engines.

Buses in China have faced fierce competition in recent years from high-speed railroad and subways. The railroad passenger traffic in the country increased by 8.4% in 2019 over 2018, while highway passenger traffic dropped by 4.8% during the same period. Low travel activity in 2020 due to the pandemic is estimated to further cut back the operating rates for buses in the country. Additionally, China is seeing a noticeable growth in battery-electric buses, particularly in the city bus category, which does not require engine oils. On this background, the already declining HDMO consumption in this segment is anticipated to experience an even steeper decline over the next five years.

Following this trend, the two largest channels for aftermarket HDMO sales in the bus category, IWS and fleets, are anticipated to experience declining sales in the future. Scaling this down further will be Chinese people continuing to drift away from buses and instead using railroads. The development of high-speed railroads in the country poses a threat to the buses plying between cities, which are the key customers for the IWS channel. The fleets channel, which performs in-house oil change and purchases lubricants via a central purchasing system, is faced with a constraint of choosing from a limited pool of oil brands. This is driving a small share of sales via this channel toward retail shops.

The construction vehicle category in China has experienced growth from 2015-2020, on the back of an initiative taken by the Chinese government to encourage the development of the country’s construction industry to boost the economy. Investments in real estate and infrastructure development helped bring the construction industry back on a growth trajectory in 2020, after a brief slowdown for only a couple of months. Other initiatives, such as the launch of National IV Standards for construction vehicles in China in December 2020, are expected to stimulate the sales of new construction vehicles. These trends are expected to augment the demand for HDMO in the construction vehicle category in China in the short-term future.

Construction vehicle fleets in China are typically owned by construction and real estate companies and other companies in related industries. Due to the significantly large size of the construction vehicle fleets, these corporations tend to purchase lubricants from oil blenders or first-tier distributors at relatively lower prices compared to owner-operators who usually own less than five vehicles. Owner-operators end up purchasing lubricants from retail shops, OEM/blender’s tier-two distributors or wholesalers at substantially higher prices. This is encouraging smaller owner-operator fleets to get themselves affiliated to large construction fleets, through which they can purchase lubricants more economically and also get the oil change service done via the fleet garage. Consequently, the Chinese construction vehicle category is seeing growing engine oil sales via the fleet channel, which is forecast to overtake the owner-operator channel in terms of aftermarket HDMO sales in the next five years.

Online sales channel for commercial automotive lubricants in China is still not as popular as the consumer automotive segment in China. However, the industry is seeing signs of possible future growth in this channel. Internet and e-commerce are highly encouraged by the Chinese government, and industry experts are of the view that a better regulation of online sales could keep the counterfeiting activity in check and might be able to drive healthy growth in this market in the future.

The HDMO market in China is continuously changing with an altering vehicle landscape, the introduction of new National Standards for commercial vehicles, growing logistics demand and significant investments in infrastructure and real estate projects stimulating growth in commercial fleets. Kline’s deep dive into this market in 2020 has revealed some interesting trends in the HDMO sales channel landscape, particularly for trucks, buses and construction vehicles, in the country. These trends and opportunities have been comprehensively presented by Kline in a detailed “what-if” analysis report, “Heavy-duty Motor Oil: China Channel Dynamics and Opportunities for Trucks, Buses, and Construction Vehicles.”

2

David Tsui is a Project Manager at Kline & Co. in the Energy practice. You can reach him at david.tsui@klinegroup.com.

Pooja Sharma is a Project Manager at Kline & Co. in the Energy practice. You can reach her at pooja.sharma@klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries that include lubricants and chemicals. Learn more at www.klinegroup.com.

REFERENCES

1.

https://klinegroup.com/reports/passenger_car_servicing_pcmo_sales/.

2.

https://klinegroup.com/reports/heavy_duty_motor_oil_china/.