Economic impacts are already severe, and evolving national policies will impact the shape and duration of economic recovery.

Adverse lubricants market signals could extend beyond 2020 if COVID-19 persists or social distancing becomes embedded in corporate behaviors.

The COVID-19 pandemic, which started in China in November 2019, now afflicts much of the world. What will be its immediate and lasting impacts on the global economy and, specifically, on the lubricants industry?

What we know now is that the virus is highly transmissible and has a higher mortality rate than seasonal influenza. There are currently no medicines or vaccines to fight the disease. The only effective weapon at present is social distancing, imposed by various means, to slow transmission of the disease.

At best, it would seem that radical measures adopted worldwide could contain the impact of COVID-19 to mid-year (a lifecycle of a little over six months). Just as likely, based on the history of previous pandemics such as the Spanish flu and Swine flu, its extent could persist for up to 18 months, lasting well into 2021.

The economic consequences

COVID-19, and the restrictions put in place to inhibit its spread, will have massive and potentially long-lasting consequences. Governments are responding with measures to stimulate economies, assure liquidity and soften impacts on the public.

China is considered the OPEC of industrial goods. The country has a leading role in several industries, including automotive, electronics and pharmaceuticals. China, with other afflicted countries such as South Korea, Japan, Germany and the U.S., are all vital to global supply chains. Virus containment efforts have caused factory closures due to worker shortages, non-availability of parts and shutdown of logistics networks. Even as China lifts these restrictions, the supply-side shock will continue for some time, as restrictions in other countries impact Chinese exports. Early insights into the damage caused by COVID-19 in China show industrial production down by 13.5% in January and February 2020 versus December 2019. Even larger declines are reported in Chinese retail sales and exports. The impacts on Chinese GDP in 2020 are still being assessed, but early estimates suggest a decline of 3%-5% over pre-crisis growth forecasts of +5.5%. No real growth is a possibility.

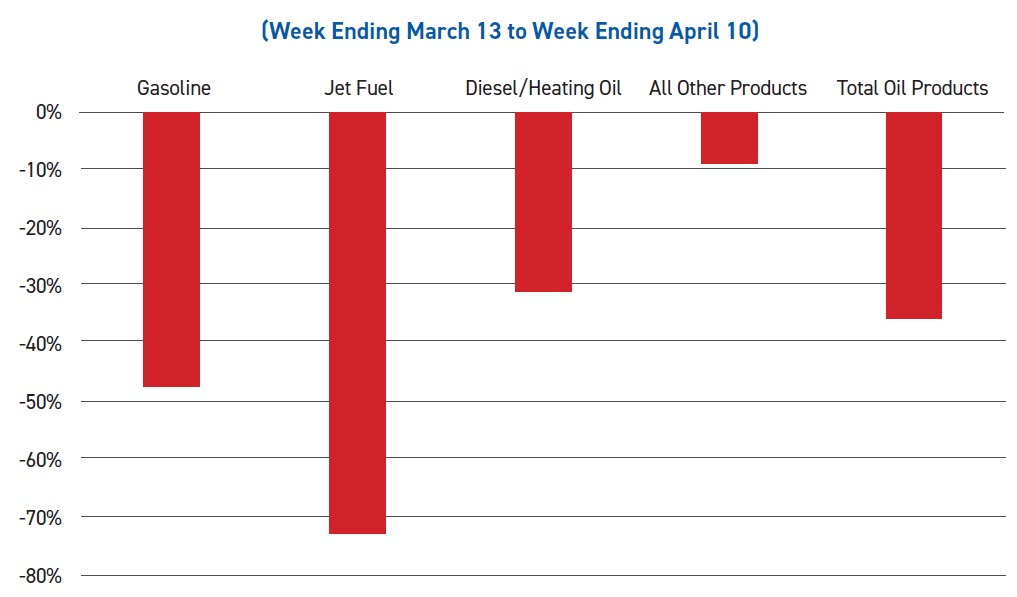

The damage caused by COVID-19 to oil markets has been much more severe. On March 26, the International Energy Agency announced that world oil demand could drop by up to 20%, from 100 to 80 million B/D, while the crisis persists. Though hard data lags behind, current U.S. statistics show the early impact on domestic petroleum products supplied (a leading indicator of consumption) with massive declines in demand between March 13 and April 10 (

see Figure 1).

Figure 1. Change in U.S. petroleum products consumption. Source: U.S. DOE/EIA

Figure 1. Change in U.S. petroleum products consumption. Source: U.S. DOE/EIA

Hardest hit have been transportation fuels (jet fuel, gasoline and diesel), registering demand declines of 71%, 48% and 31%, respectively, between March 13 and April 10.

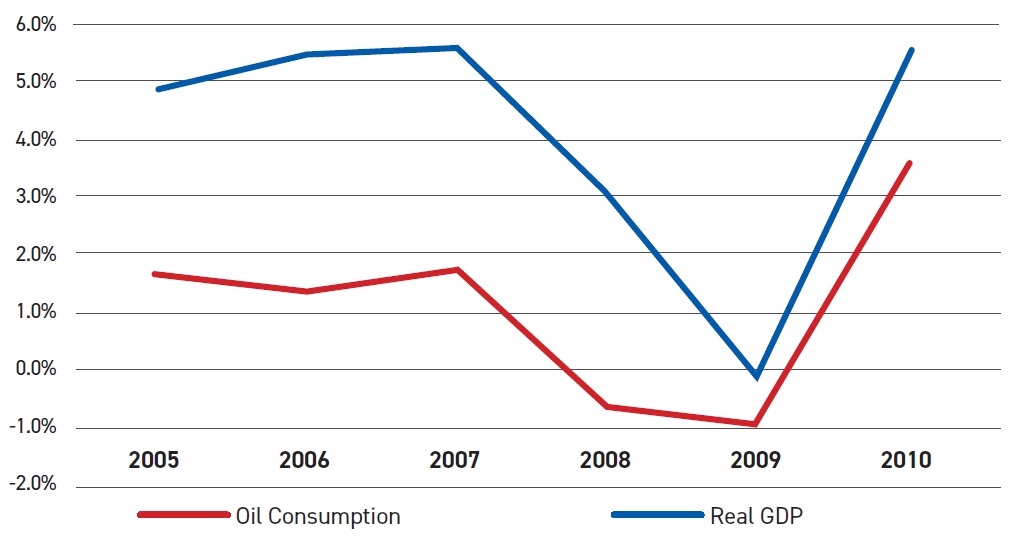

Previous non-medically driven recessions, such as the global financial crisis of 2007-2009, have had far lesser impacts on oil consumption in aggregate. While financial markets and consumer spending were affected, oil consumption fell in lockstep with global GDP (

see Figure 2).

Figure 2. World real GDP versus oil consumption growth. Sources: IMF, BP

Figure 2. World real GDP versus oil consumption growth. Sources: IMF, BP

What we can presuppose is that oil markets will behave quite differently with COVID-19, which impacts physical behaviors in addition to financial ones. Oil markets are already reflecting that difference.

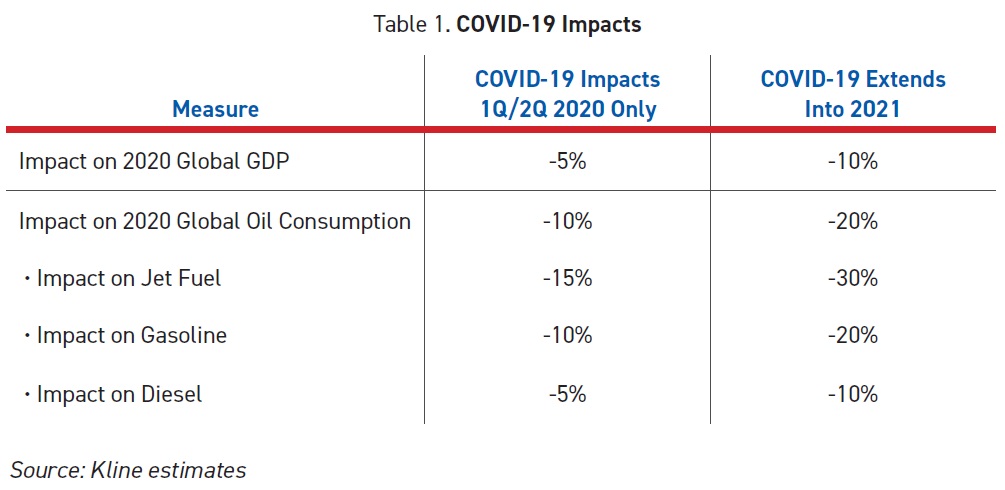

Taking what we know, at present, about the potential impacts of COVID-19 on global economic activity under the most optimistic and pessimistic of assumptions, what approximate early assessment can we postulate for the possible range of impacts on global GDP and oil demand in 2020 (

see Table 1)?

Impact on the global lubricants market

Impact on the global lubricants market

First, we have empirical evidence that global lubricant consumption in aggregate is driven by changes in real GDP, with a historical negative demand elasticity of between 3% and 4%. In other words, lubricants consumption is expected to change at a rate of some 3%-4% per year below the projected change in annualized global real GDP over the same period. Based on the above range of real GDP growth estimates, global lubricants demand in 2020 could be expected to decline by between 8% and 15% from 2019 levels. But, in reality, because of the unique characteristics of the COVID-19 pandemic, we may expect the decline in lubricants consumption to be even greater. Let’s look at two examples from the 2007-2009 financial crisis.

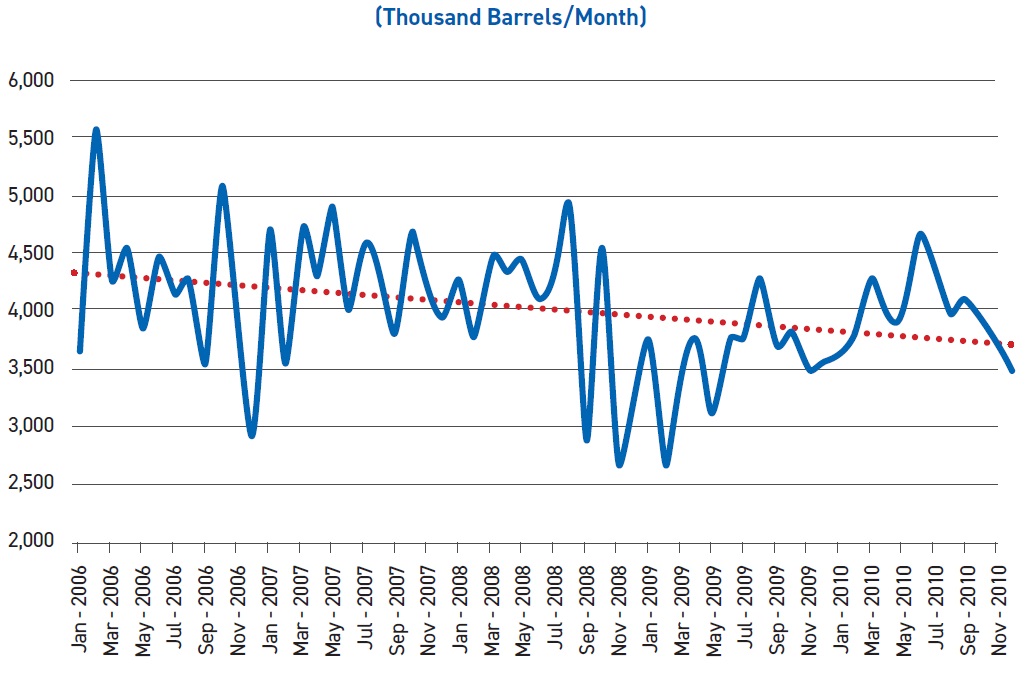

The global financial crisis of 2007-2009 truly started in 2007 but entered the wider public consciousness in September 2008 when Lehman Brothers filed for bankruptcy. The impact on the U.S. lubricants market was swift. Between September 2008 and the end of the recession (and recovery in U.S. lubricants demand) in March 2010, the cumulative reduction in U.S. lubricants consumption relative to expected (normalized) aggregate demand over that period amounted to 9.4 million barrels (or 1.3 million tons), equivalent to a loss of nearly 13% in expected demand over that time (

see Figure 3). By contrast, aggregate U.S. consumption of all refined products over that same period declined by only 4% relative to expected demand. A parallel assessment of the same crisis on global lubricants demand shows an aggregate loss of 7.3 million tons, or nearly 10% of expected consumption from mid-2008 to the end of 2009. This compares with a loss of only 3% in expected global refined products consumption over the same 18-month period.

Figure 3. U.S. “lubricants” consumption versus normalized trend, 2007-2010. Source: U.S. DOE/EIA

Figure 3. U.S. “lubricants” consumption versus normalized trend, 2007-2010. Source: U.S. DOE/EIA

May we expect the same, but disproportionately large, impact on lubricants consumption as the consequences of COVID-19 extend and mature? Early market signals suggest that social distancing, travel bans and the closure of non-essential businesses have depressed gasoline and jet fuel demand most significantly; diesel use for on-highway transportation is largely fulfilling an essential service to the economy and has been less compromised, at least initially. But a month into the U.S. experience of the pandemic, even diesel is now feeling its bite. So, by extension, do these same early signals extend to lubricants?

Presuming that we can take these initial signs as indicators, the early impact of COVID-19 may be felt most particularly in the passenger automotive lubricants segment. Less driving, social distancing and the partial closure of dealerships and quick lubes is taking a significant bite out of PCMO demand for oil changes, particularly in North America, which is far more dependent on the private automobile than most other countries. New vehicle purchases have plummeted, as unemployment spikes and consumer confidence erodes, impacting OEM initial fill volumes.

Commercial and industrial lubricant consumption are reacting more slowly, in large part because a functioning economy depends on those segments to provide essential products and services (for example, food, healthcare, commercial transportation, communications and government). But as unemployment rises, and GDP declines, the linkage to lubricants consumption, as demonstrated previously, is inevitable.

A very early assessment of the impact on global lubricants demand suggests that if COVID-19 has the same leverage on lubricants demand relative to fuels that we saw in 2008 and 2009, 2020 global lubricants consumption could drop by 15%-30% from 2019 levels. Prolongation of the pandemic into 2021 could adversely impact lubricants demand in that year, but by lesser amounts.

The inference is that the lubricants industry will have a long, hard road ahead. Preparing for adverse outcomes of the significance implied by our preliminary prognostications should be top of mind for all leaders of lubricants businesses.

This article is adapted, by permission, from Kline & Company, Inc. To read the original article, visit www.klinegroup.com.

Ian Moncrieff and Milind Phadke are vice presidents of Kline’s Management Consulting and Market Research divisions, respectively. You can reach Ian at Ian.Moncrieff@klinegroup.com.

You can reach Milind at Milind.Phadke@klinegroup.com.

Kline is an international provider of worldclass consulting services and high-quality market intelligence for industries that include lubricants and chemicals. Learn more at www.klinegroup.com.