Group I base oils: Going, going, but nowhere close to gone

Jane Marie Andrew, Contributing Editor | TLT Cover Story April 2020

Lubricant manufacturers are developing Group I alternatives for today’s ever-changing global base oils market.

KEY CONCEPTS

- The new IMO 2020 regulation mandates lower sulphur emissions for the shipping industry, which likely will shift both supply and demand for Group I base stocks.

- Group I base oil plants are less efficient than modern hydroprocessing plants and face overall operational and economic disadvantages.

- In recent decades, the Group I base oil market has been redefined as a workhorse commodity to specialty product.

For years, the majority of base oils used in lubricants were of Group I quality.1 Group I oils are considered the baseline quality stock made from paraffinic crude oil, and they are produced in a complex and increasingly expensive solvent process. However, they have attractive properties, especially for viscosity and additive solubility. Until recently, Group I base oils were the workhorse in the lubricants market, especially for automotive engine oils. However, three forces have dramatically changed the landscape for Group I oils, for both producers and customers, and the disruption is still playing out.

First, in the early 1990s, Chevron introduced a simpler, cleaner and cheaper catalytic method for producing Group II base stock, considered by many as the next higher quality level. Other technology providers followed with similar catalytic methods. With easier production and competitive prices, Group II base oils became a viable alternative to Group I base oils in many applications. In North America and most of Asia, Group II is now priced at par with Group I on a mass basis and actually somewhat lower on a volume basis because it has lower density for the same kinematic viscosity.

Second, and in parallel to the introduction of new processing technologies, specifications for engine oil began to change. Modern specifications now require higher thermal/oxidative stability and soot-handling capability, combined with improved fuel economy and lower volatility. These requirements can be met only by using higher quality base oils.

Finally, in addition to these two decades-long trends, a new regulation took effect last January that promises to further disrupt the economics of Group I base stocks. Under a regulation known as IMO 2020, adopted by the International Marine Organization, marine fuels used in certain zones may contain no more than 0.5% sulfur, down from a previous cap of 3.5%. This regulation affects fuels for the large two-stroke engines used on tankers and cargo ships. The change is likely to shift both supply and demand for Group I base stocks.

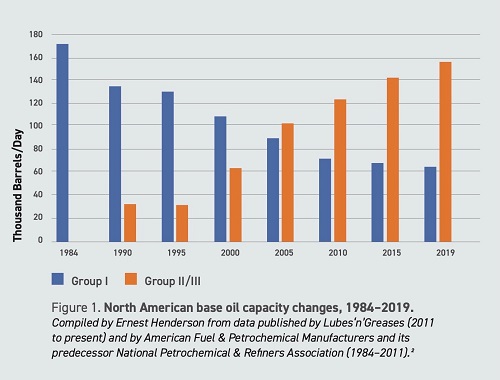

Market trends show a decline in the importance of Group I oil relative to Group II (see Figures 1 and 2), as both production and demand have continued to decline. In 2011, Group I represented 57.2% of nameplate base oil production capacity (545 kbd); in 2019 the figure was 37.5% (453 kbd), according to STLE-member Ernest Henderson, president of K&E Petroleum Consultants, citing figures from Lubes‘n’Greases magazine. Henderson expects the global lubricants market will continue to shift its demand towards Group II (driven primarily by heavy-duty engine oils) and Group III (driven primarily by passenger car engine oils).

Figure 1. North American base oil capacity changes, 1984–2019. Compiled by Ernest Henderson from data published by Lubes ‘n’ Greases (2011 to present) and by American Fuel & Petrochemical Manufacturers and its predecessor National Petrochemical & Refiners Association (1984–2011).1

Figure 1. North American base oil capacity changes, 1984–2019. Compiled by Ernest Henderson from data published by Lubes ‘n’ Greases (2011 to present) and by American Fuel & Petrochemical Manufacturers and its predecessor National Petrochemical & Refiners Association (1984–2011).1

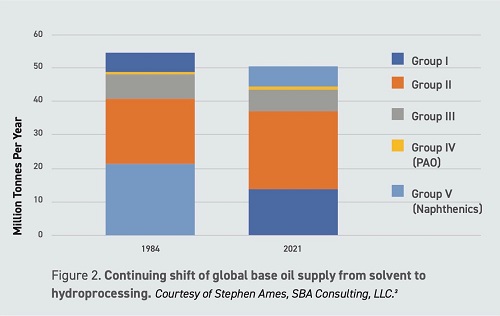

Figure 2. Continuing shift of global base oil supply from solvent to hydroprocessing. Courtesy of Stephen Ames, SBA Consulting, LLC.1

Figure 2. Continuing shift of global base oil supply from solvent to hydroprocessing. Courtesy of Stephen Ames, SBA Consulting, LLC.1

Outlook for Group I supply

Has Group I reached a tipping point, such that supplies will continue to contract, possibly into nonexistence? It’s hard to say. The economics are challenging. On the production side, these oils are at a major disadvantage relative to Group II alternatives in cost of production. In addition, the “mothership” refineries are economically vulnerable. Typically, these motherships operate in the third or fourth quartile of profitability based on Solomon studies, with exceptionally poor margins and limited options for upgrading or conversion. On the demand side, Group I stock can no longer be used for blending the latest automotive engine oil specifications, severely limiting demand. For a sense of the scale of this change, note that automotive oils are about 55% of the global lubricants pie.

The effects of IMO 2020 are just beginning to play out. “A number of Group I motherships will be changing to a sweet crude in order to produce an IMO 2020-compliant marine fuel. Sweet crudes typically have a higher cost and lower base oil yield than their sour crude counterparts, thereby further pressuring the ongoing economics of Group I production,” says Stephen Ames, managing director of SBA Consulting, LLC. “In contrast, Group II and Group III base oils are not impacted by IMO 2020, for the most part, and will likely benefit from the increased demand for their diesel byproducts.”

A ripple effect on the demand side may be driven by changes in the composition of marine lubricants, which are injected during operation and burned with the fuel. With high-sulfur fuel, the solvent power of Group I oils was important to keeping marine engines clean. But because the IMO 2020-compliant fuels will have fewer alkaline compounds, lubricant solvency will be less important, and the door may be open to using premium Group II base oils instead of Group I in marine lubricants.

Overall availability

As to the prospects for continuing availability of Group I base stocks, opinions differ. Ames says, “The market is heavily oversupplied, and global production capacity for Group I is significantly underutilized. Some capacity is operating as low as 60% of nameplate. Group I capacity is highly vulnerable to closure, either on its own or with the shuttering of the mothership.”

Henderson is more optimistic: “Despite the continuing growth in the demand for hydroprocessed Group II and Group III base stocks, there remains a continued and strong demand for Group I, especially for industrial oils, large engine oils (e.g., marine, railroad) and select process oils where solvency is an important criterion.” Henderson agrees that Group I refineries will continue to experience economic scrutiny but believes supply (and demand) will continue to exist in the long term.

There remains a continued and strong demand for Group I, especially for industrial oils, large engine

oils (e.g., marine, railroad) and select process oils where solvency is important.

Another view comes from John Rosenbaum, who retired from Chevron as senior product research engineer and manager for business development for base oils for the Americas. “Group I supply will continue to diminish to a point where it will be no longer practical for most blenders to continue using it. This outcome will continue to be driven by economic as well as environmental factors,” says Rosenbaum. “The shift to extended oil drain intervals will continue to move many lubricant and process oil applications toward use of the more stable hydroprocessed and synthetic base stocks. The longer life of these finished products will justify paying more for premium base stocks.”

As a consequence, work to develop additives will focus on those stocks. Left behind by these trends, manufacturers of Group I-based products will be forced to make do with older additive technology that may not be adequate for tougher lubricant requirements.

Rosenbaum does see some exceptions. The strongest remaining case for Group I base stocks is as lubricant for two-stroke marine engines, Rosenbaum says, “For these engines, you want a cheap lubricant that works. It needs to be relatively cheap because each stroke of these massive engines burns not only the fuel but also a significant amount of lubricant as well. Certain high-volume marine engine oils are easier and cheaper to formulate with Group I base stocks because they contain more aromatic compounds. The aromatics have enough solvent power to keep these engines clean while they’re burning fairly nasty fuels. However, the sulfur restrictions of IMO 2020 will move marine fuels to cleaner, more hydrogenated refinery products. These cleaner fuels will likely reduce the incentive to use Group I base stocks in most marine lubricants.” He adds, “I expect that the few Group I plants that can make low-sulfur Group I base stock and that have good logistics to marine lubricant blending plants and other forms of economic help will continue to be viable for some decades.”

There remains a continued and strong demand for Group I, especially for industrial oils, large engine

oils (e.g., marine, railroad) and select process oils where solvency is important.

Another view comes from John Rosenbaum, who retired from Chevron as senior product research engineer and manager for business development for base oils for the Americas. “Group I supply will continue to diminish to a point where it will be no longer practical for most blenders to continue using it. This outcome will continue to be driven by economic as well as environmental factors,” says Rosenbaum. “The shift to extended oil drain intervals will continue to move many lubricant and process oil applications toward use of the more stable hydroprocessed and synthetic base stocks. The longer life of these finished products will justify paying more for premium base stocks.”

As a consequence, work to develop additives will focus on those stocks. Left behind by these trends, manufacturers of Group I-based products will be forced to make do with older additive technology that may not be adequate for tougher lubricant requirements.

Rosenbaum does see some exceptions. The strongest remaining case for Group I base stocks is as lubricant for two-stroke marine engines, Rosenbaum says, “For these engines, you want a cheap lubricant that works. It needs to be relatively cheap because each stroke of these massive engines burns not only the fuel but also a significant amount of lubricant as well. Certain high-volume marine engine oils are easier and cheaper to formulate with Group I base stocks because they contain more aromatic compounds. The aromatics have enough solvent power to keep these engines clean while they’re burning fairly nasty fuels. However, the sulfur restrictions of IMO 2020 will move marine fuels to cleaner, more hydrogenated refinery products. These cleaner fuels will likely reduce the incentive to use Group I base stocks in most marine lubricants.” He adds, “I expect that the few Group I plants that can make low-sulfur Group I base stock and that have good logistics to marine lubricant blending plants and other forms of economic help will continue to be viable for some decades.”

Tankage is always a factor in blending

plant economics.

Another specialty niche is production of petroleum waxes, an important byproduct from Group I plants that most modern hydroprocessing plants cannot make. This byproduct can be quite valuable, but compared to lubricant base oils, the market is small. Moreover, synthetic and vegetable-based alternatives exist for many petroleum-based wax products.

Tankage is always a factor in blending

plant economics.

Another specialty niche is production of petroleum waxes, an important byproduct from Group I plants that most modern hydroprocessing plants cannot make. This byproduct can be quite valuable, but compared to lubricant base oils, the market is small. Moreover, synthetic and vegetable-based alternatives exist for many petroleum-based wax products.

Regional issues can be a factor, according to STLE-member Luc Girard, president of Sanjuro Consulting Inc. “The large-volume products (engine oils, hydraulic fluids as notable examples) have largely evolved into Group II (or III, or higher) applications, at least in North America. However, in some niche viscosity grades, especially for regions that don’t promptly adopt the most recent automotive performance categories, Group I options remain appealing. As a result, some Group I producers have chosen to become niche players with a regional, technical, or specialty chemistry (large molecules, high viscosity) focus,” says Girard.

As to production, Girard points out that economics may in fact support continuing production even well below nameplate capacity. “In some cases, the cost of remediation following the closure of a refinery would be so high that the only sound decision is to keep producing,” says Girard. “Some aspects of Group I production, like the directionally better solvency versus Groups II, III, or IV, or the ability to product high-viscosity base oils like bright stock, can ensure the viability of Group I refiners in niche markets.”

Economics of refining

Group I base oil plants, which operate solvent extraction processes, are generally less efficient than modern hydroprocessing plants, and they face overall operational and economic disadvantages. Group I plants are much more limited in the types of crude feed stocks they can run; their base oil yields are significantly lower; their byproducts are less valuable; they are harder to operate; and their base oil products are generally more difficult and expensive to blend to performance levels equivalent to Group II and Group III base stocks. To put it bluntly, Group I plants are a pain. Rosenbaum recounts, “At Chevron, our operators were dancing when we shut down the Group I plant. They were especially happy to get rid of the solvent dewaxer. There are a lot of moving parts. There are fugitive emissions. The filter fabrics develop pinhole leaks. The whole plant is a maintenance headache, especially filtering out the waxes.”

Group II refining gains its advantage in two areas. First, the base oil yield of about 60% on a vacuum gasoil (VGO) feed is nominally twice that of Group I. Second, the principal byproduct is a high-value one: ultra-low-sulfur diesel. In contrast, most byproducts from Group I refining—aromatic extracts, asphaltenes (if producing bright stock) and heavy fuel oil components, with about a 50% yield in total—sell for markedly less than the VGO feedstock. One byproduct, slack wax, does sell for premium prices, but its yield is only about 6%, compared to 50% for the low-value products. “While the cost-of-production advantage of Group II varies widely with the ‘crack values’ of the byproducts, typical cash cost differentials range from $125 to $165 per ton, an unassailable advantage for base oils currently selling for about $600 per ton,” according to Ames.

Sometimes, however, the viability of a Group I refinery is not entirely a matter of economics. Some regions maintain Group I production for intangible factors, including maintaining local economies. Politics also can play a significant role in the viability of a Group I base stock plant.

Viability of small blenders

Although big players shift the global marketplace, it’s also important to consider the consequences of the changing economics for smaller, independent lubricant manufacturers. “I think we will reach a point when most blenders will make the decision to stop blending with Group I base stocks,” Rosenbaum says. He adds, “Tankage is always a factor in blend plant economics. Blenders rarely have as many tanks as they want. Many blend plants are relatively small, regional operations, and as Group II and Group III continue to become more widely available, such blenders will opt to use their tanks for base stocks, additives and finished products that do not use Group I.”

A further challenge, Rosenbaum says, is that many Group I plants are old. Maintenance becomes a major operating cost, especially for the many Group I plants making less than 10,000 barrels per day. Moreover, these plants use solvent processing technology, and fugitive emissions are an inherent operating problem. In contrast, modern hydroprocessing plants are tightly sealed catalytic operations with no solvents, and fugitive emissions are few and relatively easy to monitor and control.

As to Group I viability overall, Rosenbaum is pessimistic, going so far as to say that many small base oil plants—perhaps already operating on slim margins—are likely to go out of business. This could translate to difficulties for their customers, the lubricant blenders. “A lot of lubricant blenders could be staring a crisis in the face unless they start to be proactive about it. They could get a going-out-of-business letter from their base oil supplier, and it will be scramble time,” he says.

Girard agrees that independent lubricant manufacturers face risks if they do not find a means to optimize their blended product mix to the base oils available to them, or to adapt to a market where Groups II and III are in much better supply than Group I. However, Ames sees less of an issue: “Over the past 20 years, blenders have been adapting to the continual loss of Group I supply. Most have already migrated some of their formulations to Group II and/or naphthenic oils. For many, the transition has been a nonevent.”

In general, the shift in supply away from Group I is likely to continue to be gradual, and the growing economic attractiveness and greater availability of Group II oils will ease the transition of small blenders to new markets and formulations.

Adapting to diminished Group I supply

Given the economic pressures on Group I supply, how is the lubricant industry adapting? The feasibility of reformulating depends on the application or market in which a given blender chooses to operate. For over 90% of all lubricant applications, Group I can be directly replaced by Group II, often with a silver lining in the form of lower additive costs, according to Ames. He says that in most cases, especially in North America and most of Asia, where Group II pricing is attractive, it is more economical to reformulate with Group II than to continue using Group I.

Other alternatives

A range of alternatives to Group I have been developed or are being explored (see Figure 3). Over the past 30 years, additive manufacturers have successfully learned how to make new additives—detergents, antioxidants, antiwear agents and so on—that are soluble in more highly saturated base oils. Most of the big additive suppliers have moved to Group II for their large-volume diluent oils, perhaps only keeping only a few small tanks available for Group I diluent oils for low-volume products.

New formulations usually center on compensating for the loss of viscosity and additive solvency. Somewhat more expensive thickeners, such as polybutene, may be needed to boost viscosity. Also, because higher grade oils have lower concentrations of aromatics (1% versus about 30% in Group I), the solvency of the additive package is reduced. To avoid haze, precipitate, or separation, the advice of additive suppliers is critical to ensuring the additive is compatible with the Group II or higher base stocks. Also, because the nature of the wax content changes from group to group, reformulation also may need to take into account the performance of pour point depressants (additives that keep oil pourable at low temperature by interfering with the formation of wax crystals). For the (relatively) low solvency of Group IV, the use of co-solvents (such as diesters) have afforded very successful finished product formulations, notably engine oils. In Girard’s view, if the focus is on high-volume products that offer solid performance, blenders can migrate away from Group I stocks by seeking Group II options that use readily accessible additive technology.

Some formulators will have challenging decisions to make about which additive suppliers to work with and what products to make. It is increasingly a matter of price over chemistry, according to Henderson: “With an oversupply of Group II, economics are favorable for change, and there are several product applications today that can either use Group I or Group II. It then becomes a decision based on economics.”

Formulators also need to challenge the idea that Group I qualities are “irreplaceable”—for example, high viscosity in bright stock (i.e., clear, light-colored oils). Ames thinks these “unique” properties are somewhat overstated: “Bright stock was most important to cheap, ‘fighting grade’ lubricants, such as SAE 50 monograde engine oils. These oils can be reformulated—at a cost savings—to a 20W50 variant that does not contain bright stock.” Even for marine cylinder lubricants, Ames says that many blenders now use alternatives of heavy naphthenic oils, polyisobutylene and deep distillation neutrals in place of bright stock. Another option is use of thickener additives to increase viscosity in a lower viscosity base stock.

Where solvency or kinematic viscosity is key, a naphthenic (Group V) base stock can be a cost-effective alternative. Naphthenic oils are less costly to produce and can substitute for (or exceed) some Group I properties. Where solvency is key, suppliers of naphthenic oils suggest that combining a Group II base stock with a naphthenic base stock can simulate the solvency effects of a Group I base stock. In such cases, Group V naphthenic oils are significantly better than the more paraffinic Group II alternative. However, naphthenic oils have other properties that make them unsuitable for modern automotive engine oils and high-performance industrial oil formulations.

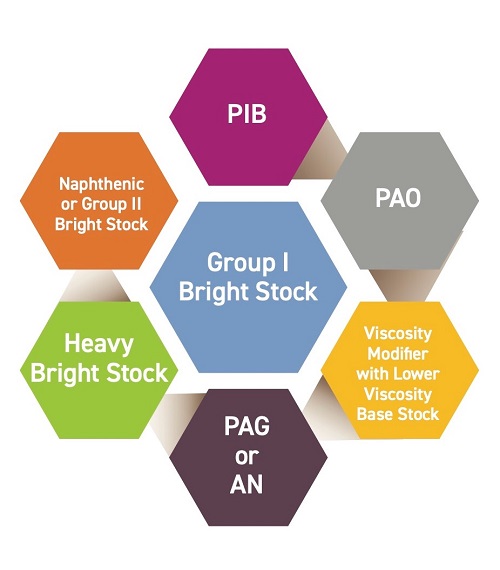

Figure 3. Group I bright stock has several replacement options. PIB = polyisobutylene; PAO = polyalphaolefins; PAG = polyalkylene glycol; AN = alkylated naphthalenes. Courtesy of Ernest Henderson, K&E Petroleum Consultants.

Availability of Group II bright stock

One of the attractive properties of Group I is the ease of producing clear, light-colored oil, called bright stock; customers often associate these aesthetic qualities with purity and stability. A consequence of the production shift to Group II and III is a decline in the availability of bright stock because it is difficult to make in these grades. According to Ames, “Group II bright stock was first produced by Gulf Canada in 1983 but found few followers and was discontinued the following year. A Korean producer has made small volumes in recent years, and ExxonMobil plans production at its new Singapore Group II plant in 2023.” However, Ames does not see it gaining widespread adoption as a substitute for Group I bright stock, primarily because of its much poorer solvency and ability to keep additives in solution (the same reasons Gulf Canada discontinued its production almost 40 years ago).

Another drawback to Group II bright stock is its cost, which is due chiefly to the difficulty of production. The molecules are big and uncooperative, and the plants are harder to operate. According to Rosenbaum, one of the biggest problems when making petroleum-based bright stock is dewaxing. The bulky bright stock molecules of the wax component don’t fit well into the pores of most dewaxing catalysts, so dewaxing is challenging—that is, expensive. An alternative is solvent dewaxing of highly saturated hydroprocessed stocks (Group II and III). This approach is practiced in a few places, but yields are low and the low-temperature properties of the products still suffer. In an effort to maintain yields and catalyst life, some Group II/III bright stock producers sell lower viscosity versions (less than 30 cSt), so some customers have to accept lower thickening power.

Henderson notes that most Group II producers do not have a readily available heavy VGO stream to produce bright stock. In an alternative method for producing bright stock, vacuum tower bottoms from a Group I or Group II refinery are processed through a propane deasphalter and subsequently hydroprocessed. By either method, the product still needs considerable processing to meet the Group II compositional requirements of 300 ppm maximum sulfur (i.e., <0.03 wt%) and greater than 90% saturates. Meeting these targets cost effectively is very difficult, which prevents Group II bright stock from being cost-competitive with the remaining capacity available to produce Group I bright stock.

In addition to cost, there is a performance drawback to Group II bright stock: solvency/solubility. According to Ames, formulations containing a significant proportion of additives are susceptible to additive “dropout” unless the Group II bright stock is back-blended with more soluble enhancers such as naphthenic oils.

Adapting beyond chemistry

Beyond pricing of the base oil, Ames notes that operations and logistics concerns are important in making the decision to switch stock. Using Group II in place of a split Group I/II slate will improve the economics of supply logistics and require fewer tanks, thus freeing working capital.

Regional supply is also an issue, according to Girard: “Niche players that have depended on Group I to meet critical performance metrics of their specialized applications may find themselves geographically isolated once their historic suppliers exit the market. If that happens, they will have very difficult decisions to make.” These decisions may include long-distance shipment of base stock, which is now commonplace. “Locking in alternate Group I suppliers— and assessing the impacts of longer delivery distances/times as one places orders further afield— should be a priority,” Girard adds.

While it may be chemically and operationally feasible to migrate many (perhaps most) Group I applications to different base stocks, there remains the time and cost for manufacturer reapprovals and industry accreditation. In some cases where unusual or unique approvals are required, change will be delayed until considerable testing has been completed to demonstrate the substitution with a different quality of base stock. For large-volume markets, the costs of reapproval should be easily assimilated.

Opportunities and challenges

The trajectory of the Group I base oil market over recent decades has been one of redefinition— from workhorse commodity to specialty product. While some traditional uses have disappeared, Group I base oils are now prized in some niche applications for their solvency effects. “The lubricants industry has been quite adept finding cost-effective alternatives when faced with change,” Henderson notes.

It appears refiners will struggle with the economics of an operationally challenging process, but a combination of continuing specialty demand, regional interests, and environmental costs of closure will continue to prop up supply of Group I base oils. Lubricant producers, on the other hand, will be challenged with many options as they navigate the changing landscape: they may alter formulations, make different products, work with different additive suppliers, look further afield for base stock supply, consider the economics of logistics and tankage—all the while keeping their eye on the yardsticks of customer support and quality assurance.

Acknowledgment

The author thanks the engine oil, driveline and industrial technical teams at Afton Chemical Co. in Richmond, Va. for contributing valuable background information.

Jane Marie Andrew is a free-lance science writer and editor based in the Chicago area. You can contact her at jane@janemarieandrew.com.

REFERENCES

1. The American Petroleum Institute defines criteria for base stock. Stock designated as Group I has less than 90% saturates and/or more than 0.03% sulfur and a viscosity index greater than or equal to 80 and less than 120. Stock designated as Group II has 90% or greater saturates and 0.03% or less sulfur; the viscosity range is the same as for Group I. Stock designated as Group III has the same range for saturates and sulfur as Group II but has a viscosity of 120 or greater. Other categories are Group IV (polyalphaolefins) and Group V (all base stocks not included in the other four groups). Details are at American Petroleum Institute (2015), API 1509 Annex E—API Base Oil Interchangeability Guidelines for Passenger Car Motor Oils and Diesel Engine Oils, March, pp. E-1 – E-2. Available here.

2. Henderson, H.E. (2017), “Global base stock outlook – shifting priorities?” 2nd ICIS North American Industrial Lubricants Congress, Chicago, IL, September 12.

3. Ames, S.B., 21st ICIS World Base Oils and Lubricants Conference in London UK, February.