The lubricants market has traditionally been slow to embrace major changes in chemistry and tends to be cautious when it comes to switching to new additive technologies. Traditional additive chemistries have served the industry well for many decades, and OEMs tend to be more comfortable with tried-and-true components such as ZDDP for wear protection.

However, with the ever-increasing push toward greater fuel economy requirements, OEMs are introducing new engine and driveline technology at a faster pace than ever. The new engines are more complex with more components and new alloys that allow for higher compression and greater thermal efficiency. New transmissions are more compact and lightweight with more forward speeds while being required to handle even greater torque and horsepower.

All the while, OEMs are continuing to lower the engine oil viscosity requirements and extending drain intervals. These trends are all driving the performance requirements for lubricants and creating opportunities for lubricant formulators.

Fuel economy has been a major driving force in lubricant additive technology, and now, with ever-extending drain intervals, fuel economy retention will be driving additive selection and lubricant formulations. The used engine oil environment is drastically different than fresh engine oil as components have oxidized or been spent and become degraded. The engine oil also is full of suspended contaminants such as fuel, water, acids, soot and sludge, which affect the fluid characteristics. This provides a greater challenge for additive companies to optimize used oil fuel economy, especially in an engine oil environment where combustion takes place. There could be an opportunity for long life friction modifiers that perform well in a used-oil environment.

Low-viscosity engine oils have been a longstanding lever OEMs have used to extract fuel economy gains. Going from 10W-30s to 5W-20s and now 0W-16 has made its way into the mainstream engine oil market and was approved for ILSAC GF-5 Plus and GF-6B. As automakers continue to drive the use of ultra-low-viscosity engine oils such as 0W-12 and 0W-8, the engines will start to encounter more boundary layer type friction where surface asperities are more likely to come in contact.

This was witnessed in the development of the new fuel economy test for GF-6 where the Sequence VIE engine was having difficulty showing fuel economy improvements from a 0W-16 candidate oil over the reference oil at 115 C oil temperature. Only by lowering the temperature 15 C and pushing the lubricant back up the viscosity curve were they able to show differentiation. Engines designed to run more boundary layer-type lubrication regimes could drive friction modifier and antiwear additive selection that is better designed for this type of lubrication. These thinner viscosities also tend to go against the trend of increasing dispersant content in engine oil to help provide longer lubricant life as dispersants tend to be very large molecules that increase the viscosity of the finished fluid. This could drive the use of lower molecular weight dispersants or multifunctional dispersant viscosity modifiers to provide long fluid life without as much of a viscosity penalty.

OEMs are continuing to squeeze every last percentage of fuel economy out of their drivetrain, which is resulting in a lot of new innovation. FCA has a new aluminum alloy that can withstand temperatures almost 200 F higher to help increase the thermal efficiency in its engines. Nissan has hydrogen-free, diamond-like carbon coatings, which pair with specialized lubricant additives that allow for a thin, low-friction film. Mazda has commercialized its spark-controlled compression ignition engine, designed to mimic diesel fuel economy with gasoline. Each OEM has seemingly gone its own route in pursuit of fuel economy, making for a ripe environment for lubricant additive companies to create specialized chemistry that works with the new engines and transmission designs to maximize their efficiency.

Traditional lubricant additive chemistries may be reaching their performance limits where adding more simply isn’t good enough, and treat rates may be chemically limited to protect exhaust after-treatment devices. This could drive a shift toward new additive technology such as ashless antiwear and EP components, friction modifiers designed for used oil or low-viscosity dispersants to meet the needs of the vehicles of tomorrow. On top of this, the government push toward electric vehicles (EVs) also changes the lubricant additives market as EVs bring along their own unique requirements for lubricants.

Though OEMs are continuing to innovate on the internal combustion engine (ICE) side, they also are investing in battery electric vehicles (BEVs) and hybrid and plug-in hybrid electric vehicles (HEVs and PHEVs). While BEVs might not take an engine oil, they still require other lubricants such as greases, transmission or gear oil, and coolants to function.

However, the removal of the ICE from the vehicle has brought about a unique new problem. Without the typical noise of the combustion engine and exhaust, EVs are much quieter, leading the occupants to hear more of the vehicle sounds from sources such as wind, tire hum, gearbox or bearing whine and axle clicking. Lubricants in BEVs can be surrounded by inductive currents and high amperage wires where the lubricant may need to either insulate or conduct that current depending on the application. BEVs have seen field issues such as bearing failures from electrically induced wear. Those bearings have not worn down severely enough to compromise function but still require a warrantied repair for the OEM, as the noise becomes audibly concerning to the vehicle owners. These types of failures have typically required the OEM to replace the entire electrical drive unit (inverter, motor and gearbox), as diagnosing and isolating the source of noise can be very time consuming.

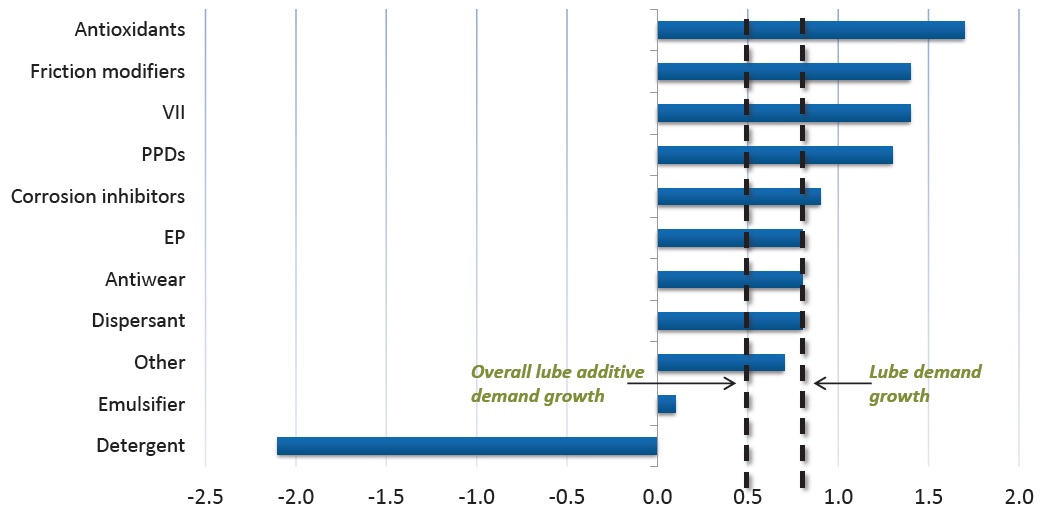

The traditionally cautious lubricant additives market may be in for some faster-paced shifts as the industry grapples with emissions requirements, new ICE technology and the shift toward EVs. This is likely to help bring forward novel chemistries in the lubricant additives market. Our report is projecting global lubricant additives to grow at a 0.5% compounded annual growth rate over the 2019-2023 period, though the modest overall growth masks the faster-paced changes happening in each market segment (

see Figure 1).

Figure 1. Global lubricant additive demand growth, 2018 to 2023 (CAGR, %).

Figure 1. Global lubricant additive demand growth, 2018 to 2023 (CAGR, %).

Kline’s recently published report, Global Lubricant Additives: Market Analysis and Opportunities 2018, dives deeper into the trends driving the additives industry such as the slowdown in marine lubricants demand and the growth in automotive additives. The study breaks down demand by region and product category, along with a FutureCast projection of additive demand by chemistry type, and provides insights into the lubricant additives industry.

David Tsui is a Project Manager at Kline & Co. in the Energy practice. You can reach him at david.tsui@klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries that include lubricants and chemicals. Learn more at www.klinegroup.com.