Polyisobutylene (PIB) is a liquid or semisolid vinyl polymer formed by the cationic polymerization of isobutylene, but the raw materials also can include mixtures of isobutane and isobutylene and fractions of C

4 hydrocarbons along with isobutylene. The C

4 hydrocarbons are derived from naphtha of a crude oil refinery and also can be a derived from plants where natural gas is used as a feedstock.

PIBs are prepared in a wide range of molecular weight, and commercially available PIBs usually range from a few hundreds to a few millions of molecular weights. This article, however, discusses market environment only for PIBs with molecular weight of 8,500 and less. PIBs with molecular weight greater than 8,500 are altogether different chemistries and excluded from this analysis.

PIBs are broadly classified into two categories depending on the placement of double on (C=C)—high reactive (HR) and conventional PIBs. HR PIBs have a higher share of exo-terminal C=C bonds, while conventional PIBs have a very low proportion of exo-terminal C=C in their carbon chain. HR PIBs, as the name suggests, are more reactive than conventional PIBs.

Consolidated supply chain

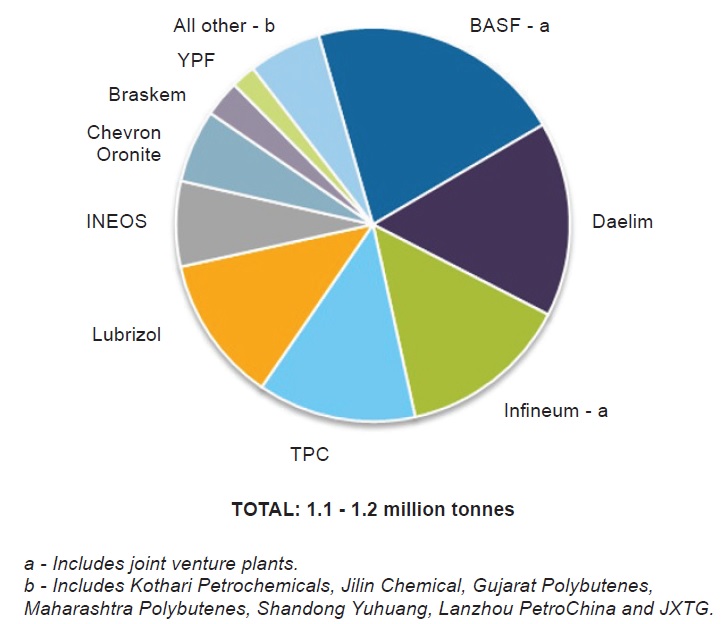

The global PIB market is characterized by a limited number of suppliers across the key regions catering to demand. Kline estimates global PIB capacity, including both HR PIB and conventional PIB, at around 1.1-1.2 million tonnes in 2018 (

see Figure 1).

Figure 1. 2018 global PIB capacity by supplier.

Figure 1. 2018 global PIB capacity by supplier.

The global PIB capacity is fairly split between HR PIB and conventional PIB, with the share of the latter marginally higher. In terms of the regional spread for PIB, Asia-Pacific has the biggest production capacity base, accounting for almost a third of the global PIB capacity. Within Asia-Pacific, the major capacities are in South Korea, China, Japan, Malaysia and India. North America and Europe closely follow the Asia-Pacific region, with around 31% share each in the global PIB capacity. Within North America, the entire capacity base is concentrated in the U.S.; in Europe the capacity base is spread in Germany, France and Belgium. Besides this, a couple of PIB plants are in South America, accounting for almost 5% of global capacity.

While Asia-Pacific may have the biggest production capacity base, its actual production of PIB is lower in 2018 than North America and Europe. This is because of the newer plants in the region that are ramping up production, mainly in China and Malaysia.

An interesting feature of the global PIB capacity is that around a third of the capacity is held by lubricant additive companies. Since lubricant additives are a key application area for PIBs, the major additive companies have in-house capacities that partially fulfill their demand for PIBs. These additive companies also source PIBs from other PIB suppliers in the merchant market whenever needed.

Outlook

In line with growing demand, a few PIB producers are implementing plans to set up new capacities of PIB. For instance, Lubrizol is setting up a plant in Deer Park, Texas, to produce HR PIB by 2019/20. The company has licensed Daelim technology to produce HR PIB but hasn’t publicly announced the size of its plant.

Similarly, JXTG in Japan has taken an initiative to increase its production capacity by 5 kilotonnes per year by year-end 2019. However, the company focuses on production of very high molecular weight PIBs in the range of 30,000 and above in addition to PIBs in the range of 8,500 and less. It is believed that only 30% of the planned new capacity will be earmarked to produce PIBs in the molecular weight range of 8,500 and less.

A new PIB plant in Saudi Arabia is planned jointly by Aramco, Total and Daelim and is scheduled to come onstream by 2024. This plant will have a total production capacity of around 80 KT per annum split between conventional and HR PIBs.

Therefore, while the supply of HR PIBs most likely will grow on the back of new capacity and improved operating rates of existing plants, conventional PIBs will grow primarily due to improved operating rates of existing plants.

Lubricant additives

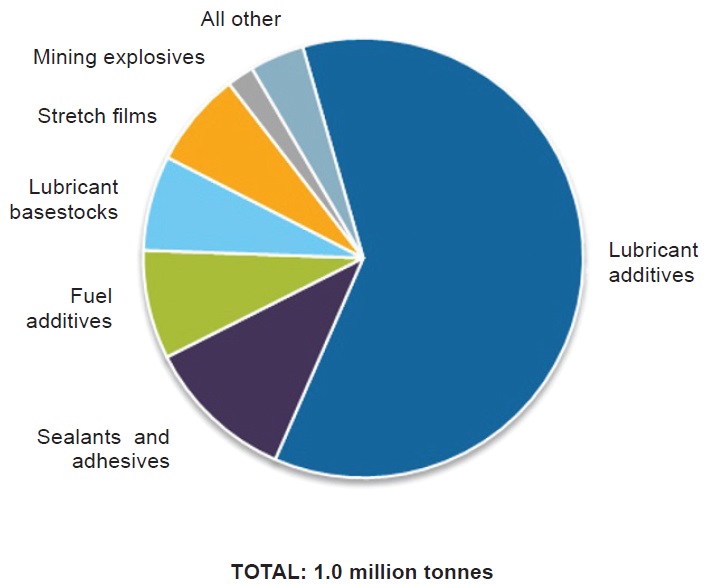

While lubricant additive manufacturing is the largest application for PIBs, other applications include fuel additives, lubricant basestocks, stretch films, sealants and adhesives, mining explosives and cosmetics, among others. The total PIB demand (including HR and conventional PIBs) in 2018 was approximately 1 million tonnes. The total PIB demand is almost equally divided between HR PIBs and conventional PIBs, with the former having a slight lead over the latter.

Lubricant additive is the major application, accounting for almost three-fifths of the global PIB demand. Within lubricant additives, PIBs are primarily used for producing dispersants—chemicals used to suspend (or dissolve) particulate contamination and prevent contaminants from agglomerating and depositing on metal surfaces. Dispersants are used in a wide range of lubricants, including passenger-car motor oil, heavy-duty motor oil, railroad, natural-gas engine oil, marine cylinder oil and aviation-piston engine oils. Dispersants also are consumed in automatic-transmission fluids, gear oils and motorcycle oils.

While PIBs with molecular weights in the range of 500-4,000 and even higher can be used, most commonly used molecular weights for dispersant manufacturing are 1,000, 1,300 and 2,300. Besides dispersants, PIBs are used as VI improvers and antimist agents in metalworking fluids.

PIBs also are used to make dispersants for fuel additives. However, the global demand for additives used in fuel is limited, thereby limiting the demand for PIBs in such an application. In terms of function, dispersants used in fuels aim to achieve the same function for which they are used in lubricant dispersants—cleanliness of engine (

see Figure 2).

Figure 2. 2018 global PIB demand by application.

Figure 2. 2018 global PIB demand by application.

PIBs have high viscosity, which makes them a suitable candidate for use as a thickener. Traditionally, brightstock has been used as a thickening agent, but with declining supplies of it PIB is being evaluated as a possible substitution. PIBs are used as a basestock in several applications like two-stroke engine oils, gear oils, greases, metalworking fluids, compressor fluids and marine oils, among others.

Within the sealants and adhesives industry, PIBs are used as a tackifier, plasticizer or even as a polymeric base for adhesives or sealants. Due to the inherent tackiness of PIB, it is considered a superior tackifier for the adhesive and sealant industry. In the packaging industry, PIBs are used only in production of stretch films. PIBs are used as a cling agent, which means it helps the stretch film to hold on tightly to the load. PIBs in stretch films offer the property of tackiness (or stickiness). In the explosives application, polyisobutylenes (PIBs) are used in making emulsion explosives. PIB is not directly used in explosives but its derivative—PIBSA (polyisobutylene succinic anhydride)—is used in the explosion mixture.

There are a host of other applications, including cosmetics, paints and coatings, tires, electrical insulation and insulating oil, modifiers for asphalt, rubber and polymers and oil impregnated leather that account for the balance PIB demand globally. These applications together account for around 3%-4% of the global PIB demand.

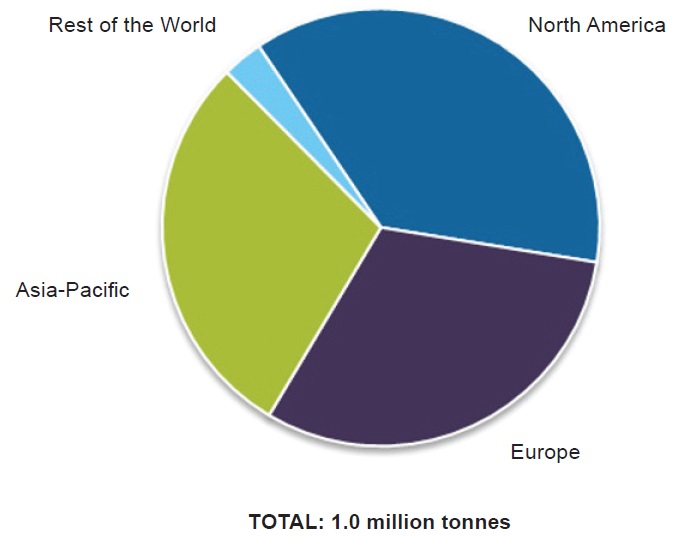

Due to the skewed demand for PIBs from lubricant additives, its demand is primarily centered around the additive manufacturing hubs—the U.S. Gulf Coast in North America, France and Italy in Europe and China and Singapore in Asia-Pacific (

see Figure 3).

Figure 3. 2018 global PIB demand by regions.

Figure 3. 2018 global PIB demand by regions.

Specs drive demand

Due to the overwhelming share of lubricant additives manufacturing in the global demand for PIBs, its demand is strongly tied to growth in finished lubricant demand. The global demand for PIB (including both HR and conventional PIBs) is projected to grow at a compound annual growth rate of 1%-1.5%.

The rapid demand growth for HR PIBs will be driven by growing need for these PIBs in producing dispersants for ILSAC GF-5 type of oils. Demand for HR PIBs will further get a boost when GF-6 specification kicks in, possibly requiring increased dispersant usage. In contrast, demand for conventional PIBs will decline within the additive application as the demand shifts toward HR PIBs.

The growth in industrial applications such as sealants and adhesives, stretch films and other smaller segments will drive the demand for PIBs. The demand for conventional PIBs from 2T oil applications will decline as the markets shifts from two-stroke engines to four-stroke engines for two-wheelers. This loss in demand, however, will be compensated by growth offered by other basestock applications for PIB such as gear oil, greases and marine, among others.

Anuj Kumar is a Project Manager in the Energy practice with Kline & Co. He works with lubricants and lubricant additives and has 12 years of market research and consulting experience in downstream specialty segments. Kline is an international provider of world-class consulting services and high-quality market intelligence for industries including lubricants and chemicals. Learn more at www.klinegroup.com.