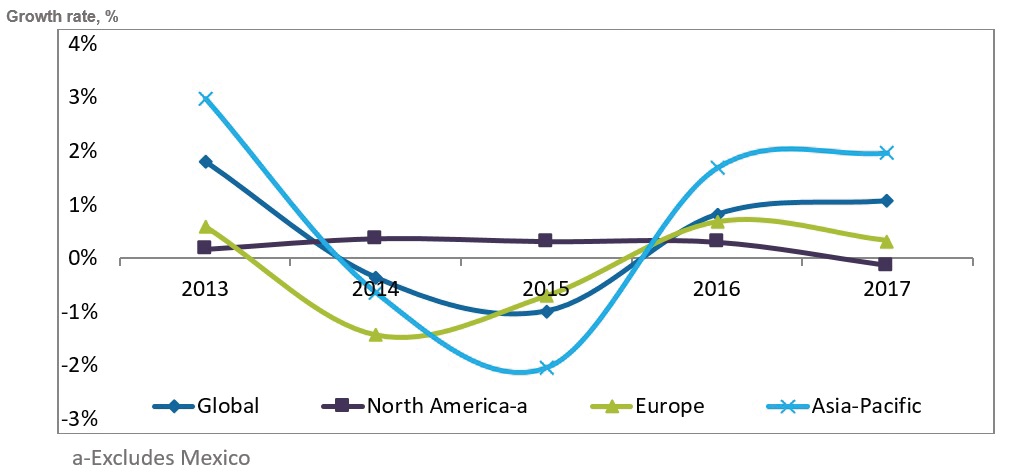

The post-crisis finished lubricant market can be characterized by a sluggish growth not exceeding a compounded annual growth rate (CAGR) of 1%during the next few years, all in a context of unprecedented challenges such as ongoing decarbonization of the global economy coupled with emerging technological disruptors such as electric vehicles, automation and shared economies. The finished lubricant demand in 2017 witnessed small growth over 2016, with varying performance in different regions. The Asia-Pacific region, which traditionally exhibits the most vigorous growth, is already showing signs of deceleration, mainly driven by China’s economic slowdown. Europe and North America have remained flat or negative (

see Figure 1).

Figure 1. Global lubricant demand annual growth for major regions, 2013-2017.

Figure 1. Global lubricant demand annual growth for major regions, 2013-2017.

Despite the slow growth in the overall finished lubricant market, synthetic lubricants have remained a fast-growing segment. Increasingly stringent emission regulations around the world, with the subsequent upgrade of automotive OEM specifications, make the synthetic lubricant market the fastest-growing segment of the lubricants industry. This, in turn, is driving demand for synthetic lubricants base stock.

The types of synthetic lubricant base stocks covered in Kline’s recently published Global Synthetic Lubricant Basestocks include American Petroleum Institute (API) Group III, gas-to-liquids (GTL) base stocks, polyalphaolefins (PAO), polyalkylene glycols (PAG), synthetic esters, phosphate esters, polyisobutene (PIB) and alkylated aromatics. Group III+ refers to all the Group III base stocks that have a VI greater than or equal to 130. This includes base stocks produced from GTLs, waxy raffinates and other virgin and bio-based Group III base stocks with a minimum VI of 130.

GTL base stocks are clearly synthetic products. Group III base stocks have been included in this article because their performance comes close to the performance offered by GTL and PAO base stocks on many important parameters. Furthermore, Group III-based products can be marketed as synthetic products in most countries. Due to their better availability and lower prices, Group III base stocks have captured a large share of the synthetic lubricant market. This makes them an important part of the synthetic lubricant base stock industry despite the way they may be viewed in technical terms.

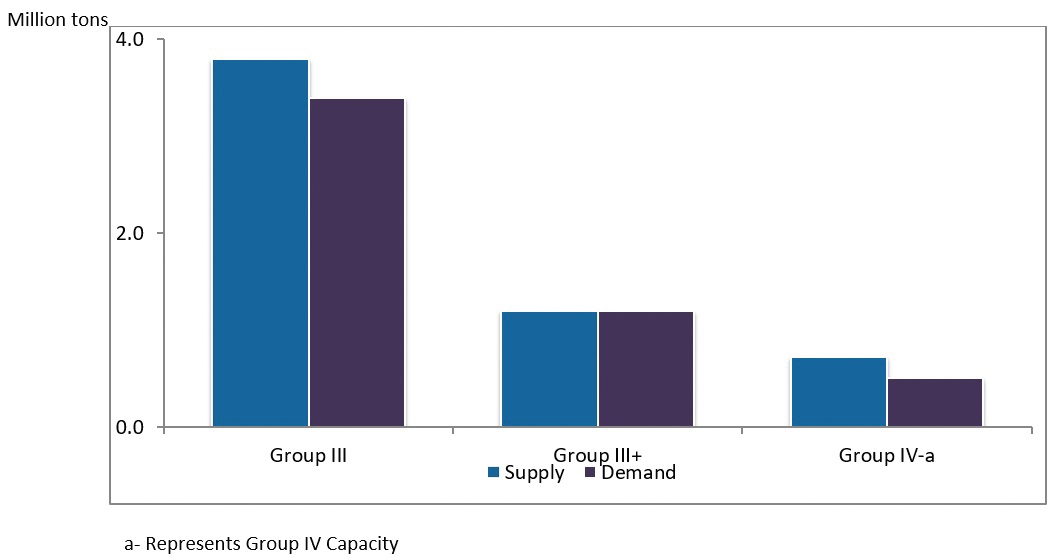

The global base stocks supply and demand has been trending toward high-performance base stocks.

The share of synthetic lubricant base stocks demand has grown consistently. While in 2011 they represented an estimated 8% of the global base stock consumption, synthetic lubricant base stocks accounted for nearly 12% in 2017 (

see Figure 2). In line with that result, the market has undergone a major transformation from a supplier’s market with supply of high-performance base stocks tight with respect to demand, and most of it tied to in-house demand, to a buyer’s market with supply of synthetic lubricants base stock, notably Group III, far in excess of technical demand. (This article analyzes the synthetic lubricant base stock exclusively from a technical demand market perspective.)

Figure 2. Global supply demand balance for Group III, Group III+ and Group IV base stocks, 2017.

Figure 2. Global supply demand balance for Group III, Group III+ and Group IV base stocks, 2017.

Demand for Group III/III+ and Group IV will be driven by availability, approvals and expansion of synthetic lubricants usage. Group III/III+ are primarily used in top tier in consumer automotive lubricant formulations such as 0Ws, 5Ws passenger car motor oils but also in top-tier heavy-duty motor oils, like 5Ws, as well as in factory fill ATFs.

In the automotive segment, PAOs are used in fuel economy engine oil grades, long-life fill-for-life automotive gear oils and transmission fluids. In industrial lubricants, heavy-grade PAOs are used in gear oil and stationary gas turbines.

In terms of new nameplate Group III/III+ capacity, a number of additions can be expected since some base stock suppliers have embarked on a mission to upgrade their product quality to Group III+. New sources of competing material also are emerging in China, as a number of coal-to-liquid suppliers have started operations and reportedly will be placing base stock of Group III+ quality.

Conversely, substantial Group IV capacity expansion is expected to be completed in 2019, largely in the U.S.

Group III is sufficient for meeting performance in most instances. Supply of approved versus unapproved Group III will be a key factor, having a significant impact on demand trends. On the other hand, Group III+/IV use is driven by desire for OEM approvals. For these reasons, PAO and Group III+ capacity expansion is difficult to project, as OEM risk aversion leaves these premium base stock products on uncertain footing.

The Group V base stock supplier landscape is fragmented, with global and regional suppliers targeting specific industries and market segments.

Under Group V are a diversity of oleochemicals and petrochemical materials, including synthetic esters, PIBs, PAG, alkylated aromatics and phosphate esters, among others.

Installed global capacity of Group V base stocks is highly variable and flexible. Moreover, the lubricants market constitutes a small application for materials classified within the API Group V base stock category, since companies actually produce esters, PAG and PIB primarily for other industries such as plastics and personal care, surfactants, adhesives and sealants and tires.

Group V base stock products each have core end-uses in certain market spaces, mostly in industrial lubricant applications. Synthetic esters, meanwhile, are the most versatile product category, finding application across the entire automotive and industrial lubricant spectrum.

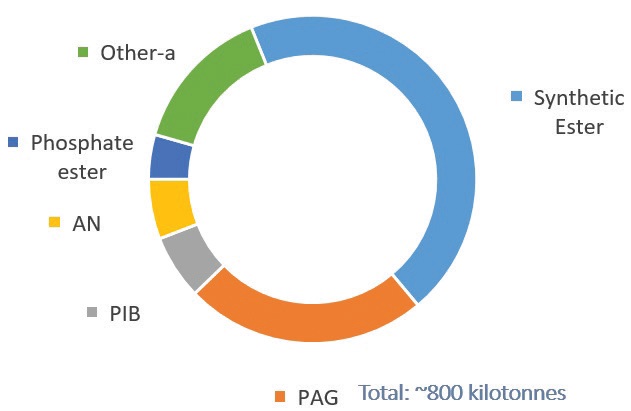

In fact, synthetic esters and PAG represent more than two-thirds of global demand for Group V base stocks, as shown in Figure 3:

•

Synthetic esters are used as correction fluids, enhancing solubility in Group III-based formulation (engine oils) and metalworking fluids, but they also are used in hydraulic fluids (HF), aviation lubricants and bio-lubricants.

•

PAG is used in HF, compressors, refrigeration fluids and gear oils.

Figure 3. Global Group V base stock demand by base stock type, 2017.

Figure 3. Global Group V base stock demand by base stock type, 2017.

Other minor synthetic base stocks are used mainly in their core application areas.

•

AN: Heat transfer fluids, refrigeration fluids, metalworking fluids

•

PIB: 2T MCO (motorcycle oils), gear oils, aluminum rolling oils

•

Phosphate esters: Fire-resistant hydraulic fluids.

Already existing uncertainty surrounding PAO supply was exacerbated by the increasing occurrence of natural disasters, with Hurricane Harvey being one of the most devastating for the industry since most of the petrochemical sites situated in the Texas Gulf area were affected. Some of them declared

force majeure situations; others, including a major PAO manufacturer, managed to keep operations uninterrupted—although there were still serious logistic disruptions. There are a handful of players dominating the global PAO market, and nearly half of them are located in the Texas Gulf region.

The main end-use applications that consume Group V base stocks are metalworking fluids, hydraulic fluids and refrigeration oils, among other automotive and industrial applications.

A fairly steady growth is anticipated for synthetic lubricants base stock, with remarkable differences among various materials.

Synthetic base stock demand will be driven by two significant factors.

Robust growth in synthetic and semi-synthetic lubricants well above lubricant industry average will be driven by demand for synthetic lubricant base stock; however, since the rate of demand being created is slower than the rate of new capacity addition, there will be increasing substitution pressure. Therefore, inter-material competition is another key factor driving demand. Two major market spaces where the inter-material competition is evident:

1.

Group III/GTL versus PAO, especially in top tier automotive applications.

2.

Synthetic esters versus AN competing on the solubility performance in automotive formulations, whereas conventional PAGs have been used as alternatives to esters in a variety of applications such as metalworking fluids, industrial gear oils and compressor and hydraulic oils.

Sharbel Luzuriaga is a project manager at Kline & Co. in the Energy practice. He is based in Kline’s Prague office in the Czech Republic. You can reach him at Sharbel.Luzuriaga@klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries including lubricants and chemicals. Learn more at www.klinegroup.com.