KEY CONCEPTS

•

Many analysts see 2025 as the turning point for the mass-scale adoption of electric vehicles.

•

Fully electric battery-electric vehicles are projected to become the leading technology by 2040.

•

There is little data on the effects these disruptive technologies might have on the finished-lubricants industry.

After several decades of stability and continuity, the world is entering a new period in personal mobility characterized by fundamental changes.

The emergence of such disruptive forces as ride-sharing, autonomous (AV) and electric vehicles (EV), all technologies with the potential to reinforce each other, pose a challenge that might eventually transform the automotive industry—along with its numerous associated markets, including finished lubricants.

These changes are prompting several questions for our industry to ponder:

•

What are the direct and indirect implications for stakeholders operating in the finished-lubricant business?

•

How, when and to what extent will the impact be felt?

There is an overflow of reports assessing the various dimensions of evolving mobility, but there is little information linking the implications that these disruptive technologies might have on the finished-lubricants industry.

In this article, we will review some of the considerations related to the implications for the consumer automotive lubricants market, specifically passenger car motor oil (PCMO) in 15 of the largest PCMO markets.

Transformation drivers

More stringent emission limits, sustainability concerns, energy security, competitiveness, consumer preferences and even geopolitics all are factors playing a decisive role in the changing personal mobility landscape. Precisely, strong governmental support is a prerequisite if EVs are intended to become the mainstream alternative to internal combustion engine (ICE) vehicles. This is a key aspect considering the significant techno-commercial obstacles that EVs must overcome before gaining market-driven traction. At present, some of the major barriers preventing the wider spread adoption of EVs include higher sticker prices compared to ICE vehicles, range anxiety concerns and limited charging infrastructure, among others.

Also worth mentioning is the motivation to adopt EVs and the subsequent pace of diffusion that will rely on the overlapping combination of all above drivers, as governments in different countries pursue different priorities.

At the December 2015 Paris climate conference, 195 countries adopted legally binding global climate deals, resulting in a global consensus toward the need for cleaner energy and transport. The growth of battery electric vehicles (BEVs), plug-in hybrid electric vehicles and hybrid electric vehicles (PHEVs, HEVs) have been primarily driven by strong governmental support in nations with stringent emission standards, such as the U.S. and European countries. Moreover, the rapid deterioration of air quality levels in large cities has been the main driver in countries like China and other emerging economies.

In this regard, ambitious EV sales targets were announced during recent years; for instance, the Chinese New Energy Vehicle program. Meanwhile, in Europe some governments have committed to ban new ICE vehicle sales gradually, at a city level (Ultra-Low Emission Zones in London) or nationwide (i.e., the ban sale of new ICEs by 2040 in France and the UK).

As a reaction to these mobility mega-trends, major OEMs are investing in EV technology. Many traditional OEMs—BMW, Volvo, VW, Ford and Renault—have unveiled plans to introduce new EV models and set future EV sales targets in line with the government’s aspirations for the EV market. The orchestrated effort between governments and OEMs in countries like China and certain European countries have proved effective in exerting the leverage accelerating the diffusion of EVs.

With the above forces at play, sales of EVs, including BEVs, but also PHEVs and HEVs, albeit from a modest start, have been growing for the last five years. Despite this exponential growth, EVs still remain a fraction of the global vehicle population. Hence, any impact assessment is influenced by the length of time assumed for the analysis. Some also are beginning to question the green credentials of EVs, considering their footprint if different energy sources are used to generate electricity to power electric vehicles.

Market participants share a consensus view that 2025 may become the turning point for the mass-scale adoption of EVs. By then the cost of EVs could have already reached parity to ICE vehicles, enabling EVs to become the mainstream alternative.

The impact on lubricants

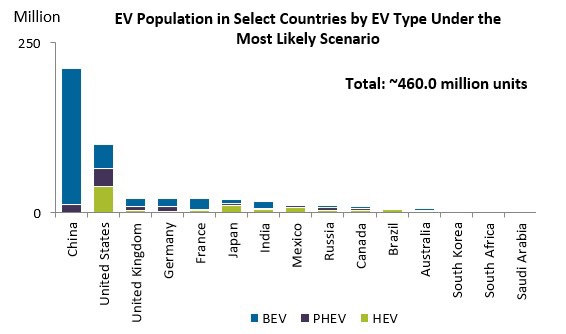

The 2040 EV landscape is foreseen to be substantially different from the EV market in 2017. According to Kline’s analysis, the EV industry will undergo a significant technological and geographical transition. Currently HEVs are the leading EV technology. HEVs were introduced much earlier than the first BEV cars, building a market presence in countries like Japan over time. Moreover, about 90% of the global EV population was concentrated in Japan, the U.S., the UK and Germany in 2017.

Fully electric BEVs are projected to become the leading technology by 2040, while hybrids (HEVs and PHEVs) are regarded as a bridge technology. In 2040, the share of BEVs is estimated to account for 16% of the total EV population, and about half of the world’s EV population is expected to be on Chinese roads (

see Figure 1).

Figure 1. About half of the world’s population is expected to be on Chinese roads.

Figure 1. About half of the world’s population is expected to be on Chinese roads.

In the near term, HEVs and PHEVs remain popular alternatives. HEVs are used often as commercial fleet vehicles, bringing about the benefits of fuel costs savings. PHEVs also can use their internal combustion engines when needed. Both technologies still require engine oils, and drain intervals are not expected to be very different from conventional ICE vehicles.

The deeper penetration of EVs has the potential to reduce the lubricant consumption, especially engine-less BEVs, as they eliminate the need for the largest product category—PCMO. The silver lining is that BEVs also will create several opportunities in areas like coolants, specialized greases, gear and transmission fluids. To maintain optimal operating temperatures, some EV manufacturers may use liquid coolants for batteries, as well as for moving parts, resulting in increasing coolant consumption. Lubricant suppliers may use this opportunity to introduce EV-specific specialty products, with some offering dielectric properties. The introduction of EV- and hybrid-specific specialty lubricants creates an opportunity for lubricant suppliers to compensate for volume losses with an increase in value.

Market forecast

In the near term, shared mobility services can incur in higher vehicle utilization; hence, boosting PCMO consumption due to more frequent oil change intervals. BEVs are not yet widely used in shared mobility services due to concerns over their driving range and charging infrastructure. However, once these hurdles are overcome, shared mobility providers may adopt BEVs over private drivers.

Autonomous vehicles (AVs), considered as a special, driverless case of ride-sharing, could become another large disruptor of the broader transportation industry by transitioning to on-demand transportation models. However, many challenges will need to be overcome before self-driving cars are ready for the mainstream. Safety is an aspect of great public attention in the aftermath of the most recent Uber AV lethal accident.

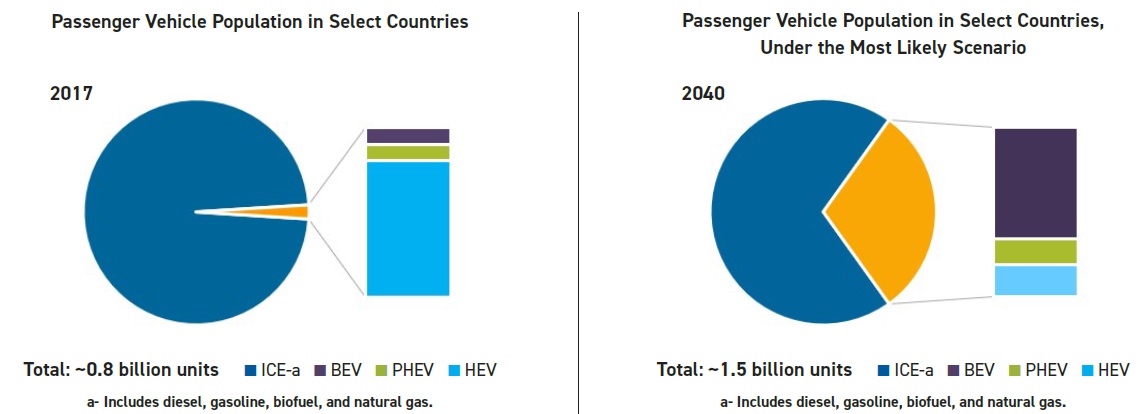

Even assuming a fast-paced adoption of EVs, ICE vehicles will continue to prevail, accounting for more than two-thirds of the global passenger vehicle population by 2040 (

see Figure 2).

Figure 2. ICE vehicles will continue to prevail, accounting for more than two-thirds of the global passenger vehicle population by 2040.

Figure 2. ICE vehicles will continue to prevail, accounting for more than two-thirds of the global passenger vehicle population by 2040.

In the near term (2018-2025), electric mobility is expected to remain a niche market with a limited influence on the demand of engine oils. During this period, quality shifts from mineral-based toward synthetic engine oils, and the resulting effect on oil drain interval, will remain the main factor driving PCMO demand.

In the long-term (beyond 2025), growth of EVs is expected to exert a greater influence on finished lubricants, mainly as a byproduct of technological improvements, new production process and the inevitable convergence with other technological platforms, namely shared and autonomous mobility.

Our analysis shows that PCMO demand in selected countries under this study is depressed at an estimated compound annual growth rate (CAGR) of about 1.0%; this decline is directly proportional to the progressive EV penetration and has translated into an aggregated PCMO demand loss of about 1.2 million tonnes by 2040.

The degree of EV penetration will vary at a regional and country level, reflecting socio-economic factors, existing infrastructure and government interventions. In quickly growing economies in Asia-Pacific, PCMO demand most likely will continue to grow, driven by robust car sales, even under a high EV penetration scenario. Conversely, PCMO demand in the U.S. and Europe will be more susceptible to downward pressure, even under a low EV penetration scenario. It can be expected that the effect of EV will be marginal on PCMO demand in emerging economies in the Middle East, Africa and Latin America. These countries will post healthy growth driven by robust new car sales based on internal combustion engines.

Beyond the negative impact on market demand in terms of volume, the transition to new mobility systems is triggering fundamental shifts in the PCMO market dynamics.

The automotive aftermarket business will witness increased competition, tightening the cooperation among established and new stakeholders in the finished lubricant value chain. New market opportunities also can be identified in emerging alternative channels. For instance, blenders (Shell) and car manufacturers (Hyundai, Volvo) are partnering with car-hailing companies (Uber, among others) or technology firms (Waymo) to work with car rental companies (Avis). Car manufacturers also have made inroads in the shared mobility sector, with several companies launching their own ride-sharing platforms, including Ford’s Chariot and Kia Motors WiBLE service in South Korea, which has recently started operations in Spain in partnership with Repsol.

Electric vehicles and other mega-trends are reformulating marketing strategies, adapted to the new market ecosystem, where PCMO/finished lubricants will be increasingly regarded as an integral component of mobility solutions.

In conclusion, the evolution of mobility patterns will adversely impact the PCMO market, from volume-demand perspective, however this impact will be limited, at least in the near term. Most important, the transition to an electric-, driverless- and shared personal mobility environment will create business opportunities. First movers have the unprecedented chance to reinforce their position in this evolving market, under the assumption that they are able to capitalize on the advantage of being the first engaging in alternative trade channels, adopting and redefining marketing approaches and product differentiation strategies.

Sharbel Luzuriaga is a project manager at Kline & Co. in the Energy practice. He is based in Kline’s Prague office in the Czech Republic. You can reach him at Sharbel.Luzuriaga@klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries including lubricants and chemicals. Learn more at www.klinegroup.com.