Lubricant growth in Latin America and the Caribbean

Sharbel Luzuriaga | TLT Market Trends August 2017

New economic models are driving demand with Brazil, Mexico, Argentina and Chile leading the way.

© Can Stock Photo / monstersparrow

KEY CONCEPTS

•

Latin America and the Caribbean are among the world’s fastest-growing lubricant-consuming regions.

•

The market is expected to maintain a shift toward technological development, as more advanced engine oil performance grades enter in the near future.

•

The region is characterized by high price sensitiveness, counterfeit products, parallel imports and low end-user awareness of the benefits of lubricants.

ALTHOUGH LATIN AMERICA AND THE CARIBBEAN contribute about slightly less than 10% of the global finished lubricant demand, the region remains one of the world’s fastest-growing lubricant-consuming regions, exhibiting a compound annual growth rate (CAGR) of about 2% over the next five years.

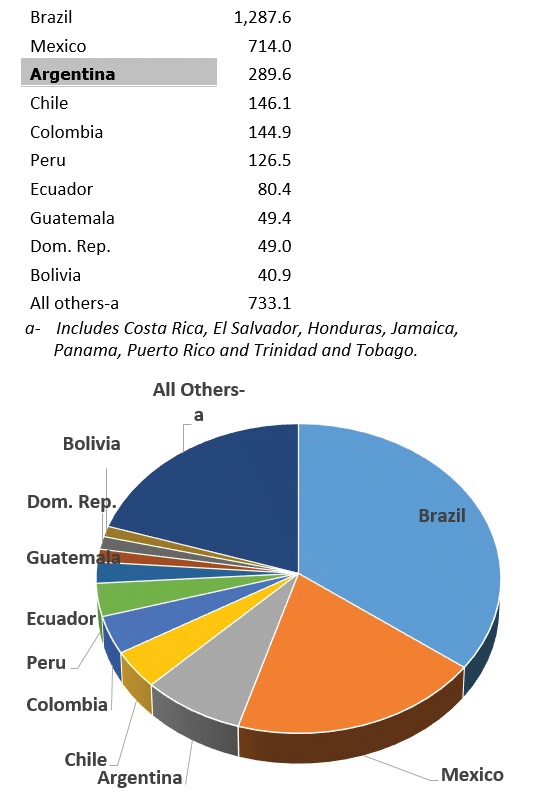

However, this general picture is primarily shaped by two major regional dominant players, namely Brazil and Mexico (

see Figure 1). These two countries display more conservative growth, hiding several smaller but dynamic markets such as Chile, the Dominican Republic, Panama and Costa Rica, where lubricant demand is posting above-average industry growth, as reported by Kline in its recently published study titled Opportunities in Lubricants: Latin America and Caribbean Market Analysis. In this report, 17 countries from the Latin American and Caribbean region are covered.

Figure 1. Finished lubricant demand in Latin America and the Caribbean by country for 2015.

REGIONAL DISPARITIES

Figure 1. Finished lubricant demand in Latin America and the Caribbean by country for 2015.

REGIONAL DISPARITIES

The region exhibits remarkable disparities in growth between commodity-exporting South American countries, compared to more highly U.S.-reliant economies in Mexico and Central America.

Following a bonanza fueled by soaring commodity prices and exports to cater to China’s insatiable appetite for raw materials, the regional economies started to feel the adverse effects of external and internal turbulences, ending a period of economic expansion in the period spanning 2003-2013, also known as the Golden Decade for the region. Due to heterogeneity in Latin America, the extent of the negative impact varies across the region, with the most negative impact being observed in major energy and commodity-exporting countries in South America, and less pronounced in net oil importers in Central America.

In an attempt to remain less vulnerable to external turbulences, local governments across the region have (or are in the process of) implemented policy reforms, albeit at a varying degree of success, in each country. The goal is to transform heavily export-reliant markets into more competitive economies with a robust middle class and strong domestic market. Therefore, it is paramount for lubricant suppliers operating in Latin America and the Caribbean to be agile, offering a lubricant product portfolio matching the emerging consumption patterns in a region transitioning from high raw material price/low financing cost economies to low raw material prices/high financing cost economies.

NEW GROWTH AREAS

Beyond the Golden Decade there is a new era of growth emerging in the Latin American and Caribbean finished lubricants market; savvy lubricant suppliers must be open to addressing new market needs.

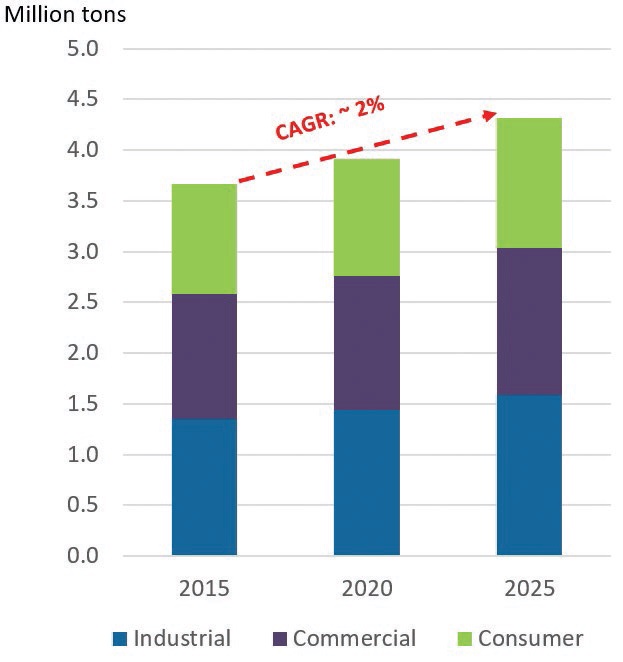

Kline estimates the Latin American and Caribbean finished lubricants market at around 3.7 million metric tons in 2015, with the largest countries, including Brazil, Mexico and Argentina, accounting for more than 60% of the finished lubricant demand in the region. By market segment, the industrial segment accounts for 37% of demand, while the commercial and consumer automotive segments represent 33% and 30% shares of the total demand, respectively (

see Figure 2).

Figure 2. Finished lubricant demand growth by segment for the 2015-2025 period.

Figure 2. Finished lubricant demand growth by segment for the 2015-2025 period.

The regional finished lubricant market can be characterized by quality shifts promoted by the renovation of the local car parc (i.e., total number of cars in a country or region) and the modernization of the industrial sector reconfiguring to more added-value manufacturing activities. The industrial lubricant segment is dominated by extractive and related industries, such as quarrying, mining, gas and oil extraction and refining, but also activities related to the processing of commodity products for exports, including agricultural and food-processing products, as well as textile and light manufacturing. The automotive and its associated component supply industries constitute another important market outlet for lubricant consumption, notably in Brazil and Mexico. The textile industry is a key GDP contributor in Central America and Mexico, with a dense network of “maquiladoras” operating in counties like Honduras, Guatemala and El Salvador. Sugar cane cultivation, and its processing industries, including bioethanol and biomass for power generation, is creating demand for industrial finished lubricants in Brazil and Central America.

Process oils, hydraulic fluids and industrial engine oils accounts for about 70% of the total industrial finished lubricant consumption in Latin America and the Caribbean. Process oils are in relatively high demand and find application mostly in the food processing, chemical, pharmaceutical manufacturing, textile and rubber industries. Hydraulic fluids are mainly used in mining, steel manufacturing and machinery. In terms of demand by grade, the most demanded hydraulic fluid grade in Latin America is AW 68. By industry, the mining industry represents the largest end-use application for industrial lubricants in Chile, Peru and Bolivia.

Within industrial engine oils, marine oils are the largest subcategory in Latin America. In some countries like Panama and Ecuador, it is reported that some portion of the engine oils classified as marine are used in power generation. In general, there are two types of maritime engine oils: 2T and 4T. The most common viscosity is monograde SAE 40, followed by SAE 50 and SAE 30. All maritime oil requirements can be met with these grades. Some of the largest cruise and marine transport companies prefer to carry lubricant stock and keep maintenance on board. This preference among large companies for in-house maintenance continues to curb demand for lubricants and services at the shipyard.

The commercial automotive segment is the second most important outlet for finished lubricants in Latin America. Mining, construction, cargo fleet and public transportation, as well as tourism, are among the most important market outlets for commercial lubricants in the region. Given the underdeveloped railroad infrastructure in the region, the vast majority of all cargo moved in the region is done via cargo trucks and vehicles on the country’s terrestrial highway system.

Latin America is one of the most urbanized regions in the world, with more than half of the population living in major urban agglomerations. Latin American commercial lubricant demand also is composed of public transportation fleets, such as city buses, as it is the preferred method of transportation.

Conventional multigrade HDMO, 15Ws, continue to be the dominant grade for heavy-duty engine oils in Latin America, accounting for more than 50% of the total heavy-duty motor oil demand in the region, with sizeable consumption of SAE 30/40/50 monogrades representing 40% share and high-viscosity multigrades accounting for the balance. Low awareness of the benefits of lubricants and adequate maintenance practices is a recurrent issue observed in Latin America. The persisting myth among Latin American end-users that “the thicker, the better” the lubricant has yet to be completely defeated.

The Latin American consumer lubricant segment is characterized by high demand for high-viscosity motor multigrades such as 15Ws but also 20Ws and 25Ws; together, these grades account for about 60% of the passenger car motor oil demand in the region. Demand for monogrades remains significant (about 20%) in a region where imports of aged vehicles from the U.S. are still very popular, despite the various initiatives to regulate this activity. Brazil and Chile have the most modern car population, with car parcs having an average age of eight and nine years, respectively. Contrary to this, Colombia and Ecuador have some of the oldest car parcs with an average age around 12 years in both countries. It is worth mentioning that the Caribbean region exhibits a strong consumer automotive lubricant segment driven by the proliferation of private passenger cars services offering alternatives to means of public transportation. In the Dominican Republic, private cars offering public transportation services, known in the local jargon as

conchos, are a popular form of transportation.

Primarily low-quality performance lubricants are used. There is low penetration of synthetic products and high growth potential in the premium lubricant product segment. Semi-synthetic PCMOs have gained ground in some markets, such as Chile and Costa Rica, as a result of modernization of the car parc based on imports of new cars requiring higher quality engine oils.

On the other hand, penetration of synthetic and semi-synthetic PCMO is still low in some high-volume markets, such as Mexico and Colombia, primarily due to the limited knowledge of vehicle owners regarding the benefits of synthetic lubricants.

Lower viscosity grade PCMOs, SAE 0W-XX and SAE 5W-XX, currently account for a small share of 7% of the total PCMO demand. These are expected to expand in 2020 to a share of 14% and in 2025 to a share of 25% of the total demand. The large motorcycle population in Brazil and Colombia are the largest markets for 2T/4T motorcycle oils.

KEY PLAYERS

Major lubricant multinationals remain the leading market players in Latin America, although their position is being challenged by local players successfully operating in the mid-tier and low-tier segments.

Global majors Shell and ExxonMobil, the top two suppliers of finished lubricants in Latin America and the Caribbean, service the region through macro distributors and are increasingly facing fierce competition from local/regional players, such as Petrobras, Ipiranga (Brazil), Akron (Ex-MexLub), Roshfrans (Mexico) and YPF (Argentina), among others. Some of these contenders aspire to achieve more gains from global majors, which are operating indirectly through distributors. Local suppliers have successfully applied manufacturing-driven strategies, having made inroads in low-tier lubricant segments, with lock-in blend plant capacities with private label, service fill and factory fill contracts.

LOOKING AHEAD

The outlook for the Latin American finished lubricant market remains bright despite various challenges.

As the region starts to pick up, it is entering a new post-recession cycle in 2017. The regional differences emerging show that growth will not be uniform and will largely depend on internal political stability, as well as the stance the new U.S. administration will take in relation to its southern neighbors.

Uncertainty around Brazil’s economy, the largest market in South America, which is immersed in a deep recession, combined with high volatility of crude oil prices, are some of the factors deterring a more robust growth in the region. Since China became a major importer of South American commodities during the last decade, from crops like soya to meat, metals and crude oil, the slowdown of the Chinese economy also has affected the region’s growth.

With overall volumes continuing to decline in Brazil during the 2016-2017 biennial, the main challenge in the lubricants industry is keeping profitability levels and avoiding “value destruction” in search of higher volume share.

However, Brazil is forecast to start recovering by 2018 in the best-case scenario. This will be driving demand for PCMOs, which are estimated to grow at a CAGR of 2.5% through 2025. Mexico, Central America and the Caribbean will post robust growth due to a closer connection with the U.S., as well as benefits arising from the low crude oil prices, given the fact that this regional cluster is a net importer of crude oils, except for Mexico.

Furthermore, the vehicle parc is based on secondhand imports where primarily low-quality performance lubricants are used. There is minor penetration of synthetic products, as well as a significant presence of counterfeit products.

The market is expected to maintain a shift toward technological development, as more advanced engine oil performance grades enter in the near future. However, this development evolves faster in larger markets, such as Brazil, Chile and Mexico. Conventional multigrade PCMOs, 15Ws, 20Ws, 25Ws and SAE 40/50 will progressively lose ground, favoring premium 5Ws and 0Ws fuel economy grades. These are expected to expand in 2020 to a share of 15% from 7% in 2015.

Conventional multigrade HDMO, 15W-40/50, continues to be the dominant grade for heavy-duty engine oils in Latin America. This viscosity grade will see a maximum volumetric growth within the next five years. Whereas in the industrial segment, process oils (PO), hydraulic fluids (HF) and industrial engine oils (IEO) lead the demand.

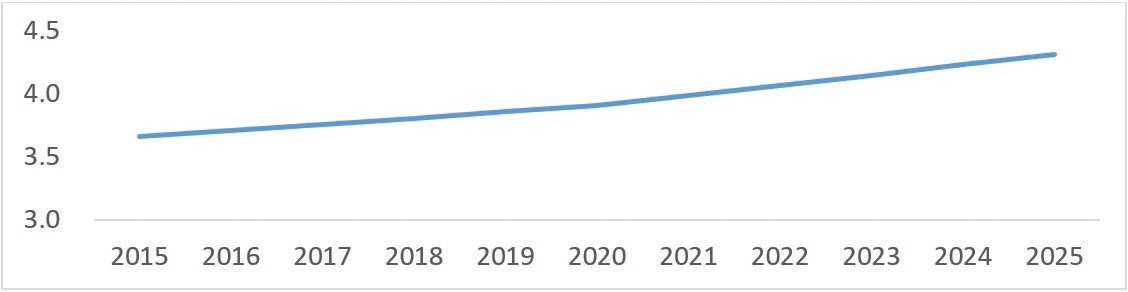

Finished lubricant demand in Latin America and the Caribbean is forecast to reach 3.9 million metric tons in 2020 and 4.3 million metric tons in 2025, with Brazil, Mexico, Argentina and Chile leading the way (

see Figure 3). Future growth in the region will be driven by an increase in exports and trade deals with North America and other regions, namely the EU, as well as countries from the Pacific Rim.

Figure 3. Forecast lubricant demand in Latin America and the Caribbean for 2015-2025.

Figure 3. Forecast lubricant demand in Latin America and the Caribbean for 2015-2025.

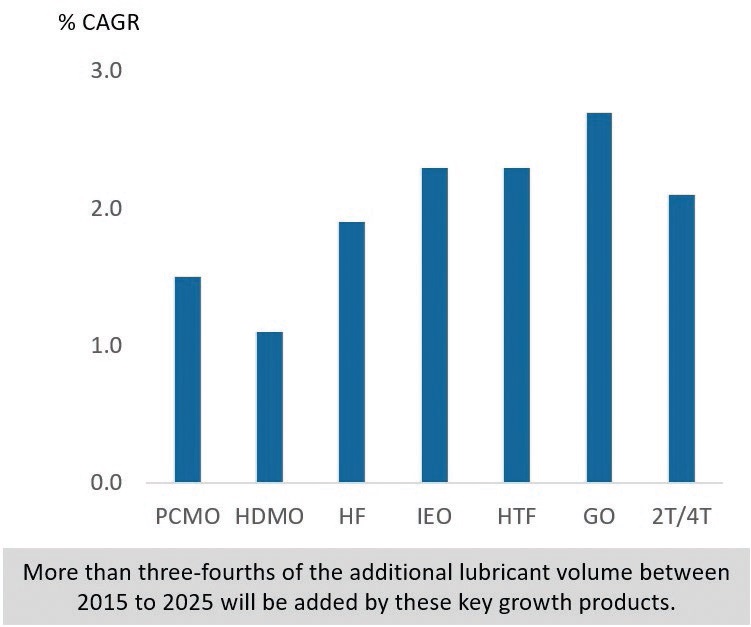

Penetration of synthetic and semi-synthetic PCMOs, and HDMO is growing in Latin America and the Caribbean, along with the modernization of the car parc. The region poses a high growth potential for volumetric organic growth. Savvy lubricant suppliers will have to be open to putting in place differentiated lubricant marketing strategies, each requiring a different set of competences to be successful in a region characterized by high price sensitiveness, counterfeiting issues, parallel imports and low end-user awareness of the benefits of lubricants (

see Figure 4).

Figure 4. Key growth products in Latin America and the Caribbean for 2015-2025.

Figure 4. Key growth products in Latin America and the Caribbean for 2015-2025.

Sharbel Luzuriaga is a Project Manager at Kline & Co. in the Energy practice. You can reach him at Sharbel.Luzuriaga@klinegroup.com

Sharbel Luzuriaga is a Project Manager at Kline & Co. in the Energy practice. You can reach him at Sharbel.Luzuriaga@klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries including lubricants and chemicals. Learn more at www.klinegroup.com.