Few casual observers, whose knowledge of electric vehicles might encompass the Tesla 3 and a few other similarly well-known models, would connect electric vehicles with heavy-duty fleets. However, beneath the surface, alternative powertrain technologies in the commercial automotive segment are rapidly catching up with their more celebrated passenger counterparts.

Subject to increasing pressure deriving sustainability concerns and the opportunities that lie along with the expansion of digital platforms, the automotive industry has responded by betting on new technologies that can comply with ever-tightening emission standards. OEMs from Daimler to Volvo to Tesla itself rush to bring new electric truck models to the market every year. Startups and local authorities team to produce ambitious public transport projects running on electric energy.

More widely, in recent years the commercial vehicle industry has witnessed the emergence of disruptive technologies that have the potential to redefine the concept of transport. Electrification is only a part of this puzzle—alternative fuel systems from natural gas to biofuels, along with autonomous vehicles and digital platforms, are the other corner pieces having the potential to shape the entire automotive value chain, including the future role of heavy-duty motor oil (HDMO).

But how does this flurry of ideas translate from the research lab to the highway stop? And how will the rollout of future commercial vehicle technologies impact future lubricant demand?

To answer that question, Kline looked at the future of HDMO demand across various leading country markets, taking into account the plethora of different factors that could shape the market of tomorrow, from electrification and the growth of vehicles with alternative drive systems to evolutions in vehicle design and the spread of advanced telematics, digitalization and the omnipresent Internet of Things (IoT) in the transport sector.

EV’s marginal effect on HDMO

In the end, electrification is expected to play only a relatively small part. Total HDMO demand in selected countries is projected to shrink through the forecast period at an estimated negative compound annual growth rate (CAGR) of 1.0%, to 3,100 kilotonnes by 2040. When EV penetration is factored in, the total HDMO demand in selected countries is projected to shrink within the forecast period of time at an estimated negative CAGR of 1.2%. In other words, a total 0.2% declining CAGR of HDMO demand is purely due to the increase in EV penetration in the on-highway commercial vehicle population in select countries.

The extent of EV penetration will vary by country and commercial vehicle segment and also fluctuates in function of socio-economic factors, existing infrastructure, pace of technology advancement and government intervention.

Ambitious government policies have been implemented in Germany, Canada and China targeting substantial emission reduction targets. There also are variations by country with regards to the preferred technology to champion. Battery electric technologies are anticipated to become prominent in Germany and China. Japan, the U.S. and Brazil are set for a higher penetration of hybrid commercial vehicles. Beyond the public sector, large companies with high-visibility brands with consumer appeal and interest in improving their corporate social reputation among the public are expected to invest heavily in low- and zero-emission vehicles to upgrade their fleets across both developed and emerging countries.

It is assumed that EV penetration across the off-highway segment will not be sizeable in the forecast period of time due to distinct operational and maintenance requirements typical for key end-use applications. However, some OEMs are already active in this area and introduced fully electric models, for instance, John Deere’s SESAM electric tractor and Komatsu’s e-dumper truck.

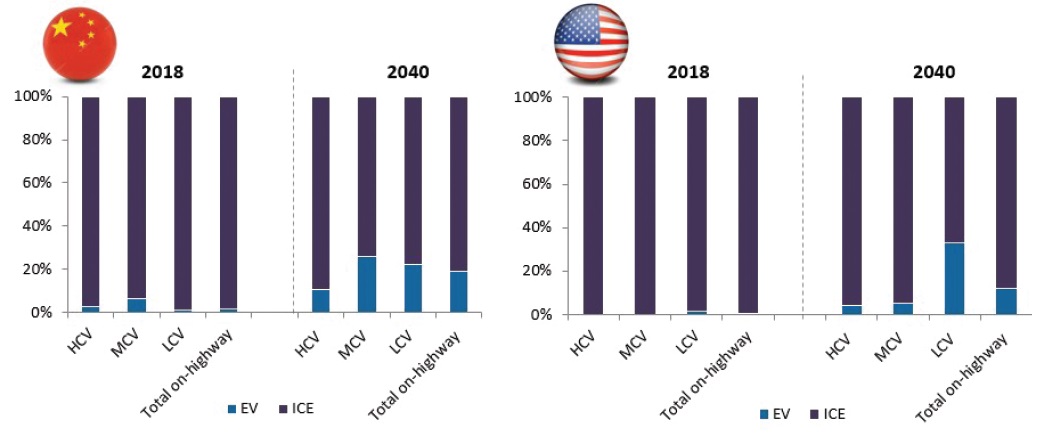

EV penetration also is very application specific (

see Figure 1). Light commercial vehicles (LCV), used, for example, in last-mile urban deliveries, are more easily electrified than the heavier classes. Over the course of the next two decades, however, a third of LCV in the U.S. are expected to be electrified, while in the medium (MCV) and heavy-commercial (HCV) sectors, expansion of electrification is expected to remain in single figures during the whole forecast period. As the medium and heavy-duty commercial vehicles segments look for cleaner technologies, what we are far more likely to see is the use of natural gas and hydrogen as an alternative to diesel fuel. However, currently the main barriers to their broad uptake are similar to electrification—the lack of infrastructure, high initial vehicle purchase cost and poor return on investment.

EV Market Penetration: 2018-2040

Figure 1. EV penetration in the on-highway commercial vehicle population by segment in China and the U.S., 2018 and 2040.

Figure 1. EV penetration in the on-highway commercial vehicle population by segment in China and the U.S., 2018 and 2040.

Even if the impact of electrification on HDMO consumption is expected to be minor, this does not automatically mean it will be business as usual in the HDMO market with the status quo persisting undisturbed by technical innovation. In concert with mandated emissions reduction, disruptive technologies developed for the commercial vehicle market, from light-weighting in vehicle design to innovations in digital freight management that optimize fuel economy, are accelerating the penetration of more advanced HDMO formulations. These enable longer oil drain intervals, which remains the main HDMO market driver.

U.S. and Chinese HDMO markets

In the U.S., across the classes from the lightest to heavy duty and off highway, there are estimated to be more than 21 million commercial vehicles in operation.

Commercial vehicle sales between 2013 and 2018 have grown at a CAGR of 8%. This is a trend that is expected to continue as we preview the next five years. However, HDMO demand will be influenced by the gradual shift to fuel economy grades.

To give two examples, in the U.S. SAE 15W-40 is still the most-consumed HDMO viscosity grade, and the uptake of lower viscosity API FA-4 SAE 10W-30 oils has been slow. With the implementation of the next round of greenhouse gas emissions cuts, and as large fleet owners appreciate the benefits these can deliver, penetration of lower viscosity grades SAE 5W-30 and SAE 10W-30 is expected to gradually increase.

The Chinese government will continue to put great efforts in the implementation of emission standards, the National VI for on-highway trucks and National IV for off-highway mobile vehicles by 2020. This will have significant impact on the lubricant product mix, resulting in an increased demand of SAE 15W-30 and double-digit growth of SAE 5W40 and 10W-40, in detriment of SAE 20W-50 (

see Figure 2).

Figure 2. Most likely EV penetration in on-highway CV for selected countries, by EV technology, 2040.

Figure 2. Most likely EV penetration in on-highway CV for selected countries, by EV technology, 2040.

It is expected that the penetration of electric vehicles in commercial fleets will accelerate the transition to lower-viscosity, fuel-economy grades. A commercial vehicle fleet consisting of a diversity of powertrain technologies will pose a challenge but also offer untapped opportunities for lubricant formulators.

Electric trucks, particular in the heavier segments, might not become a common sight on most highways anytime soon, but change is coming to the world of commercial vehicles that will have far-reaching impact across many spheres, including the future of the products used to lubricate them.

Besides alternative powertrains, emerging technologies such as the rapid diffusion of smart and connected fleets making use of technologies such as IoT, also will have an impact on the way commercial vehicles are maintained. The rapid deployment of digital technologies, including telematics, will help improve monitoring and adherence to maintenance schedules, ultimately having an impact on oil drain intervals.

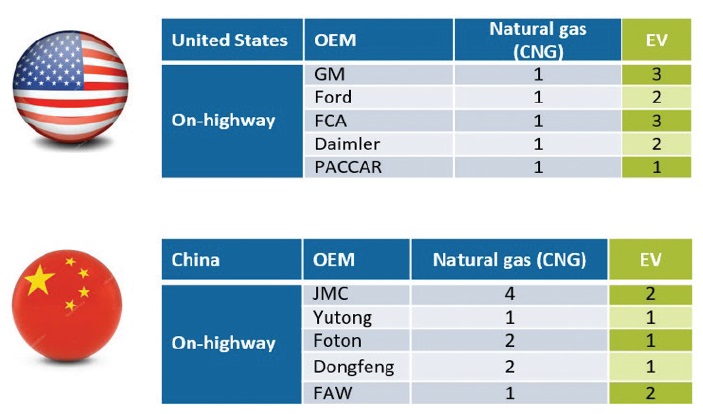

In order to cope with increasingly stringent sustainability standards, OEMs are adopting a multi-dimensional approach, opting for a mix of improving internal combustion engine (ICE) efficiency while developing alternative fuels and powertrain technologies (

see Figure 3). The decision to pursue a given strategy will consider region-specific considerations. For instance, the access to abundant feedstock supply, CNG/LNG is the preferred option for OEM in the U.S., whereas China inclines to EV in compliance with NEV policies.

OEM Strategies

1: Commercially available in a full or broad range of models.

1: Commercially available in a full or broad range of models.

2: Already developed new models that are currently subjected to testing procedures.

3: Announced plans to develop new models based on this technology.

4: No announced plans to develop this technology.

Figure 3. Strategies adopted by leading OEMs in the development of alternative powertrain systems in the U.S. and China, 2018.

OEMs also are actively pursuing opportunities in fields beyond their core businesses, competing with telematic providers, as OEMs are including their own telematic devices to collect data during production of the vehicle.

In the gradual but steady transition to new fuels and technologies, fleet operators will look for lubricants to help them simplify inventory, minimize misapplication and reduce operational and maintenance costs.

Lubricant suppliers who can ensure sufficient protection across mixed fuel commercial vehicle fleets will have an advantage in this market.

Sharbel Luzuriaga is a project manager at Kline & Co. in the Energy practice. He is based in Kline’s Prague office in the Czech Republic. You can reach him at Sharbel.Luzuriaga@klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries including lubricants and chemicals. Learn more at www.klinegroup.com.