KEY CONCEPTS

•

In 2017 the Middle East accounted for 4%-5% of global lubricant consumption.

•

The region’s industrial lube market is smaller than its automotive segment.

•

Lubricant demand in the Middle East is expected to reach approximately 1,900 kilotonnes by 2027.

The Middle East, a region in western Asia adjoining Africa, Europe and the rest of Asia, has some of the most rapidly developing economies with very high gross domestic product (GDP) per capital in the world. This region, along with Africa, accounts for about 10% of the global finished lubricants market, estimated at 40 million tonnes in 2017.

The main macroeconomic theme for the region is that most of the countries are crude-oil-driven economies trying to diversify into other industrial sectors. Despite socio-political unrest, the petroleum sector makes the Middle East an important part of the global economy. The economic growth of the countries, heavily dependent on the petroleum sector, has slowed since 2015 due to a fall in crude oil prices. As a result, these economies began to seriously consider diversifying into other industrial sectors to reduce their dependence on crude oil. Against the backdrop of these developments, Kline’s report, titled Opportunities in Lubricants: Middle East, covers the lubricants market of seven major countries in the region, Iran and six Gulf Cooperation Council (GCC) countries: Saudi Arabia, the United Arab Emirates, Kuwait, Bahrain, Oman and Qatar.

Market overview

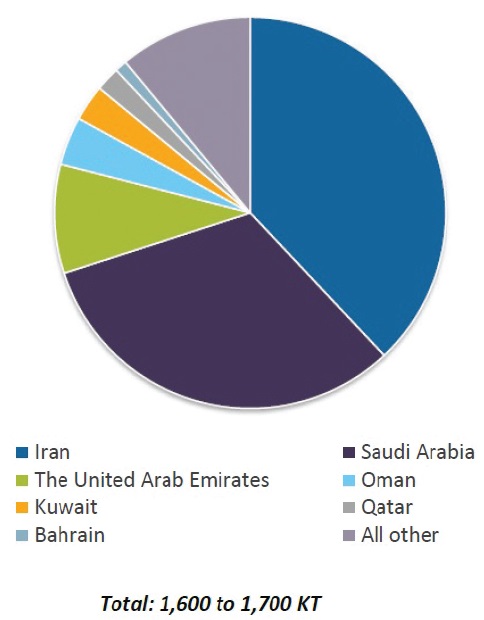

With an estimated lubricant demand of 1,600-1,700 kilotonnes (KT), the Middle East accounts for 4%-5% of global lubricant consumption in 2017. Iran, the region’s second largest economy after Saudi Arabia in terms of GDP, is the largest consumer of lubricants. It is followed by Saudi Arabia and the United Arab Emirates (

see Figure 1).

Figure 1. 2017 finished lubricant demand in the Middle East by country. (Figure courtesy of Kline & Co.)

Figure 1. 2017 finished lubricant demand in the Middle East by country. (Figure courtesy of Kline & Co.)

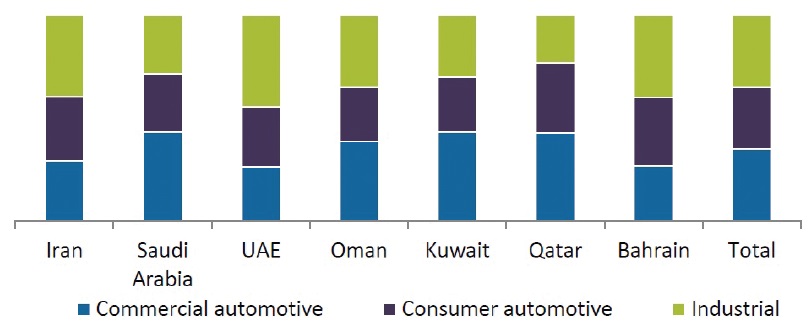

The region has a low level of industrialization; hence, the industrial segment’s share in the region’s lube market is smaller than the automotive segment. High income of the people in GCC explains why automobiles are heavily used in the region despite a small human population in comparison to other regions. Vehicle population is skewed toward passenger cars, as people prefer using cars over mass transport due to convenience and social status considerations. The industrial sector in Iran is more diversified than the GCC countries. In GCC countries major industries are oil and gas, power, petrochemicals and marine; meanwhile in Iran agriculture, cement, tile and ceramic production and steel also are consuming lubricants (

see Figure 2).

Figure 2. 2017 finished lubricant demand in the Middle East by country and segment. (Figure courtesy of Kline & Co.)

Automotive lubricants market

Figure 2. 2017 finished lubricant demand in the Middle East by country and segment. (Figure courtesy of Kline & Co.)

Automotive lubricants market

The automotive lubricants market can be further segmented into commercial automotive and consumer automotive. The first segment includes lubricants consumed by heavy-duty and other commercial vehicles, while the second segment includes lubricants used in personal use vehicles such as cars and two-wheelers.

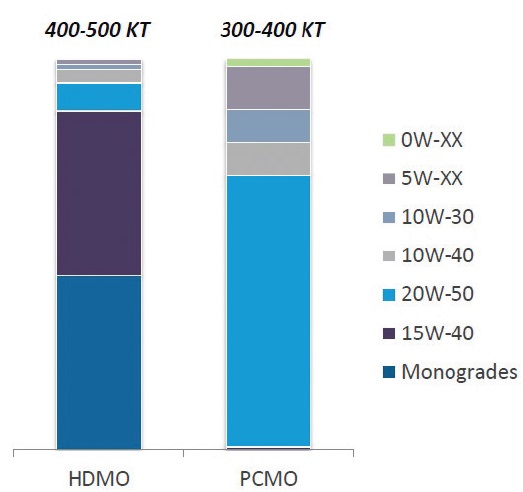

While all GCC nations are rapidly moving away from using monogrades, these products still account for more than half of the demand for total heavy-duty motor oil (HDMO)—engine oils used in commercial vehicles—in 2017. HDMO demand by viscosity grade is expected to change significantly in the region, driven by the Gulf Standardization Organization’s (GSO) standard that requires API CH-4 as the minimum service category. Iran, which does not follow GSO standards, also is moving toward multigrades, albeit slowly. Penetration of low-viscosity grades in the HDMO market is higher in GCC nations compared to other countries in the Middle East.

The market for passenger car motor oil (PCMO)—engine oils used in personal use cars—in the Middle East is mainly a multigrade market with negligible demand for monogrades in Iran and Saudi Arabia. Viscosity grade SAE 20W-50 is a popular choice, and people believe that it is the optimal grade based on environmental and weather conditions. Though the market is moving toward low viscosity oils, 20W-50 will continue to lead in the region due to general market perception and people’s habits. 5W-XX is expected to enjoy a higher growth rate compared to 10Ws, due to OEM recommendations (

see Figure 3).

Figure 3. 2017 HDMO and PCMO demand in the major Middle Eastern countries by viscosity grade. (Figure courtesy of Kline & Co.)

Figure 3. 2017 HDMO and PCMO demand in the major Middle Eastern countries by viscosity grade. (Figure courtesy of Kline & Co.)

Industrial lubricants market

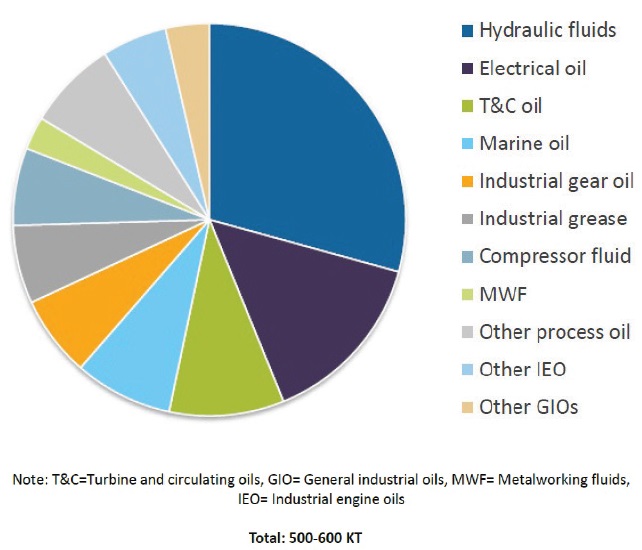

Hydraulic fluid, electrical oils and turbine oil and circulating oils together account for more than half of industrial lubricants demand in the region. Hydraulic fluids find high usage in the construction industry and a variety of other industries. Expansion of electrical transmission and distribution facilities due to urbanization is the reason for a high demand share of electrical oils. Power generation plants, oils and gas extraction operations, chemical plants and refineries account for a significant part of turbine oil demand. However, in the United Arab Emirates, industrial engine oils lead due to the high consumption of marine engine oils, attributable to huge bunkering operations in the country (

see Figure 4).

Figure 4. 2017 industrial lubricant demand in the major Middle Eastern countries by product type. (Figure courtesy of Kline & Co.)

Demand outlook

Figure 4. 2017 industrial lubricant demand in the major Middle Eastern countries by product type. (Figure courtesy of Kline & Co.)

Demand outlook

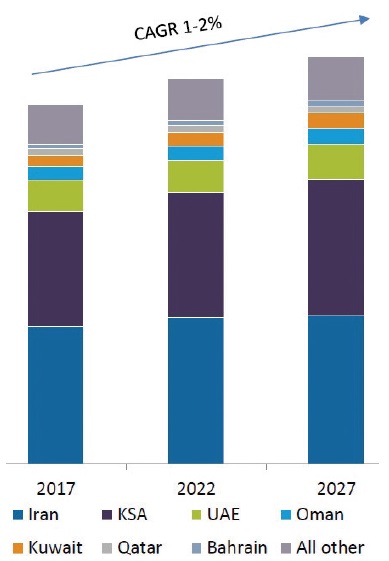

The Middle East region will witness slow to moderate growth in lubricant demand over the next 10 years to reach a demand volume of approximately 1,900 KT. Almost all the major economies except Iran will experience growth in lubricants demand, while Iran will experience a slight decline during the forecast period. GCC will continue to transition into a more industrialized region by increasing the share of manufacturing industries. This trend is driving growth in the industrial sector, which will witness much higher growth in lubricants demand than the automotive segment. The automotive lubricants market is currently transitioning from low quality to high quality lubricants, which will drive demand for longer drain interval lubricants such as synthetic and semisynthetic lubricants (

see Figure 5).

Figure 5. Lubricant demand forecast in the Middle East by country, 2017-2027. (Figure courtesy of Kline & Co.)

Figure 5. Lubricant demand forecast in the Middle East by country, 2017-2027. (Figure courtesy of Kline & Co.)

Overall the region’s lubricant market remains attractive in the future, as GCC emerges from the aftermath of a crude oil crisis with its prices revived. The governments’ reforms to manage macroeconomic imbalances such as reconsideration of subsidy plans, the introduction of value-added taxes in GCC, geopolitical issues between Qatar and other GCC countries and fresh sanctions against Iran by the U.S. will have a bearing on the region’s economy.

Nevertheless, the lubricants market will continue to expand. In the commercial automotive segment, the trend toward multigrades HDMO will be supported by availability of Group II base oil from Luberef’s Yanbu plant. Considering high concentration of luxury cars in the region and low consumption of synthetics, it can be concluded that the region can offer greater penetration levels of synthetics in the years to come. In addition, people’s attitude toward vehicle maintenance is likely to change progressively, with a gradual removal of fuel subsidies, changes in vehicle designs and maybe an introduction of fuel economy standards.

Sushmita Dutta is project manager-Energy for Kline. You can reach her at sushmita.dutta@klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries including lubricants and chemicals. Learn more at www.klinegroup.com.