Afton Chemical Corporation

American Made: The Coming Renaissance in U.S. Manufacturing

Introduction by Phil Rohrer, Marketing Manager - Industrial, Afton Chemical Corporation, www.aftonchemical.com | TLT CMF Plus November 2018

Article by Scott Miller, Senior Adviser, Abshire-Inamori Leadership Academy at the Center for Strategic and International Studies

Introduction

Manufacturing remains a large and valuable component of U.S. output. Yet, over recent years it has experienced sustained growth in only a few high-technology sectors. Until now.

In this article, Scott Miller, a senior adviser with the Abshire-Inamori Leadership Academy at the Center for Strategic and International Studies in Washington, D.C. discusses current factors influencing the U.S. manufacturing renaissance such as globalization, low energy costs, smart manufacturing, and economic factors supportive of investment.

For more information about how Afton additives can help you take advantage of this revival in manufacturing, contact your Afton representative at www.aftonchemical.com/contact.

American Made: The Coming Renaissance in U.S. Manufacturing

Technological advances have reshaped the global economy. Worldwide, extreme poverty has been reduced dramatically. Yet at the same time, industrial economies face disruption and stagnation, including secular declines in manufacturing value-added. Over the past 25 years, U.S. manufacturing has struggled, with sustained growth in only a few high-technology sectors like electronics, aerospace, and pharmaceuticals. Most other industries have experienced stasis or outright decline in value-added, with concomitant declines in employment (1).

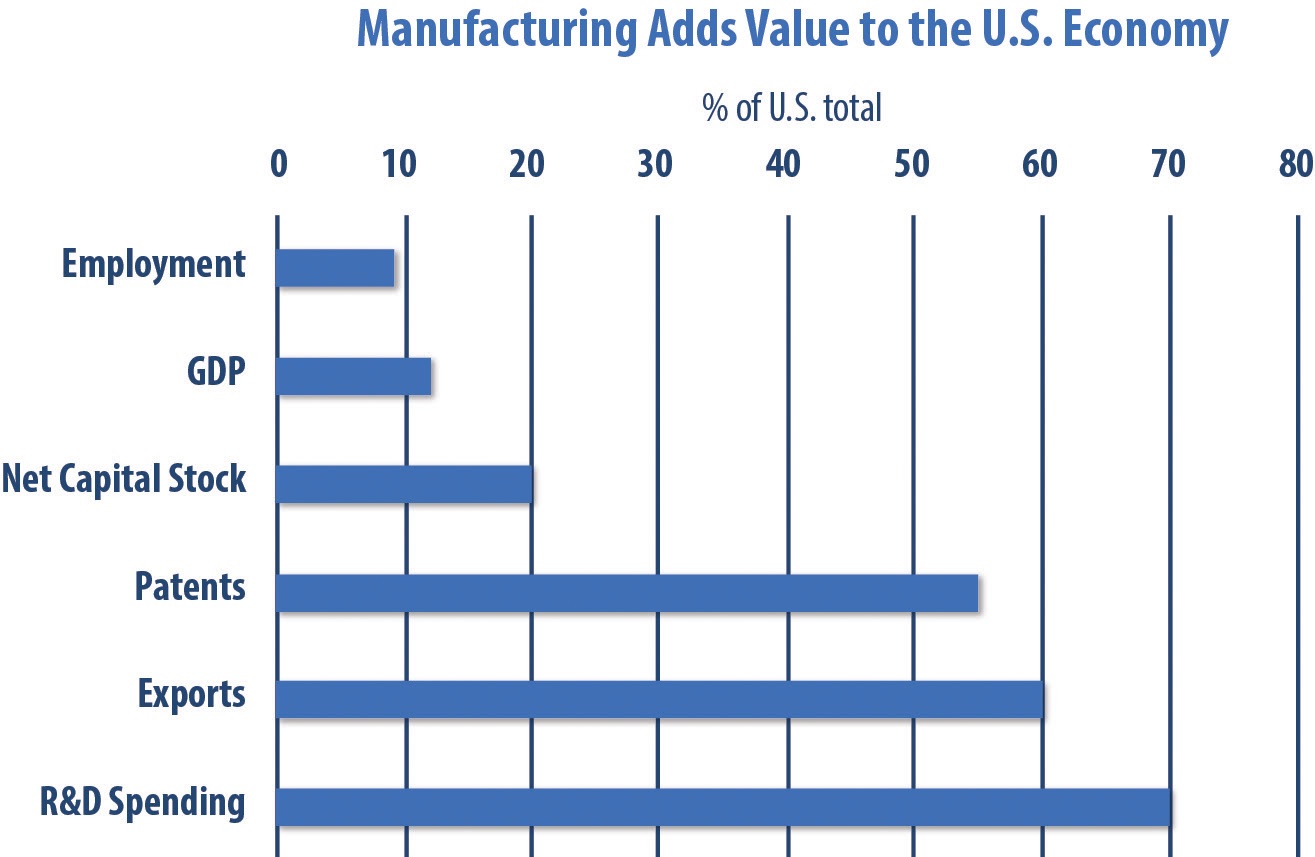

Many observers have described the U.S. economy as “post-industrial.” While it’s true that services predominate, manufacturing remains a large and valuable component of U.S. output. While providing around 10 percent of employment, the U.S. industrial base output is larger than the entire GDP of South Korea. Using 20 percent of net capital stock, manufacturers account for over half of U.S. patents, 70 percent of R&D investment, and 60 percent of exports—key factors which are essential to prosperity. (Figure 1) Alternatively, a declining industrial base exposes firms to supply chain risk and limits their agility and innovation. Furthermore, manufacturing decline leads to diminished prospects for the U.S. middle class, particularly in the 500 counties where manufacturing represents the top economic activity.

Figure 1.

Globalization: A Second Industrial Revolution

Beginning in the late 1980s, advances in information and communication technology (I/CT) led to radical changes in the way goods were produced. Just as the development of steam power in the nineteenth century was the key to overcoming transport costs, whereby firms could separate production from consumption and achieve economies of scale, the advent of low-cost, instantaneous transmission of data allowed producers to precisely coordinate tasks at a great distance (2). What once was an inter-plant transfer from a nearby supplier became international trade, part of a complex global supply arrangement. Products once made in a relatively compact geography (like Silicon Valley or the Motor City) could now be characterized as “made in the world,” with components and sub-assemblies sourced around the globe.

Concurrently, governments embraced market economics, which accelerated global development: formerly closed economies like China and the Soviet Union were opened to trade and investment, and barriers to the movement of goods, people, ideas, and culture fell dramatically. Developing economies grew rapidly, in large part because the I/CT revolution gave local firms access to production “know-how” once available only in the co-located supply networks of advanced economies. As the revolution progressed, large, globally engaged U.S. firms and high-tech sector manufacturers fared best, but the net result was a permanently reshaped U.S. industrial base.

Figure 1.

Globalization: A Second Industrial Revolution

Beginning in the late 1980s, advances in information and communication technology (I/CT) led to radical changes in the way goods were produced. Just as the development of steam power in the nineteenth century was the key to overcoming transport costs, whereby firms could separate production from consumption and achieve economies of scale, the advent of low-cost, instantaneous transmission of data allowed producers to precisely coordinate tasks at a great distance (2). What once was an inter-plant transfer from a nearby supplier became international trade, part of a complex global supply arrangement. Products once made in a relatively compact geography (like Silicon Valley or the Motor City) could now be characterized as “made in the world,” with components and sub-assemblies sourced around the globe.

Concurrently, governments embraced market economics, which accelerated global development: formerly closed economies like China and the Soviet Union were opened to trade and investment, and barriers to the movement of goods, people, ideas, and culture fell dramatically. Developing economies grew rapidly, in large part because the I/CT revolution gave local firms access to production “know-how” once available only in the co-located supply networks of advanced economies. As the revolution progressed, large, globally engaged U.S. firms and high-tech sector manufacturers fared best, but the net result was a permanently reshaped U.S. industrial base.

The Next Wave: Smart Manufacturing

Technological progress that radically reduced coordination costs over the past 30 years continues to evolve and influence the fundamentals of making things. In our view, it’s likely that the next phase of the I/CT revolution will uniquely benefit high-skill, high-tech economies, first and foremost the United States. Digitization, sometimes called “Industry 4.0” or “smart manufacturing,” is being driven by the advent and maturation of many technologies, including: high-performance computer-aided design (CAD) and engineering (CAE) software; cloud computing; the Internet of Things (IoT); advanced sensor technologies; additive manufacturing, also known as 3D printing; industrial robotics; and data analytics, machine learning, and wireless connectivity that better enables machine-to-machine (M2M) communications (3). While for many decades manufacturing has gained efficiency from advances in data processing, what’s different today is not just the improved ease and lower cost of using information. It is now possible for producers to identify, track, communicate, analyze, and use information in manufacturing at a granular level and to make changes in real time.

As connectivity and smart machines advance, technology is creating avenues for U.S. manufacturers to boost their productivity, agility, and competitiveness. New business models, which reflect increasing value from R&D, design, and services, will play to U.S. strengths but will challenge manufacturers to accelerate cycle times and broaden product variety.

U.S. Manufacturers Are Poised to Win—If They Rebuild

There is a compelling case to be made that U.S. manufacturing is poised for not just recovery, but accelerated growth in value-added. Achieving this renaissance will require action by firms and the government, some of which we will outline below. But firms here begin with a key asset—having the United States as “home market.” The U.S. consumer market is large, rich, diverse, and dynamic. The United States has no peer for attracting capital from home and abroad; moreover, its goods producers are “battle-tested,” with lean, competitive operations required for success in the world of global supply networks. Furthermore, the United States boasts the most innovative, competitive services market on the planet and is home to 45 of Reuters’ Top 100 global technology leaders (Japan, in second place, has 13) (4).

Capturing the new opportunities will not be easy. The manufacturing sector needs new capabilities. More firms need to participate in the global economy, since technology and demand growth have enhanced opportunities abroad. Many plants need to be upgraded for digital readiness; firms, focused on survival the last 20 years, now must step up to keep pace with capital requirements. For example, large investments are needed to close the gap in robotics, where the United States has a relatively low implementation intensity when compared to Japan, Germany, and South Korea. Moreover, shorter product cycles and faster discovery will require firms to “compete against time.” Considering human resources, the entire goods-producing sector will need people with higher skills, which will stretch the existing education and training infrastructure. Therefore, firms will need to redouble efforts to attract and retain skilled workers.

As connectivity and smart machines advance, technology is creating avenues for U.S. manufacturers to boost their productivity, agility, and competitiveness. New business models, which reflect increasing value from R&D, design, and services, will play to U.S. strengths but will challenge manufacturers to accelerate cycle times and broaden product variety.

U.S. Manufacturers Are Poised to Win—If They Rebuild

There is a compelling case to be made that U.S. manufacturing is poised for not just recovery, but accelerated growth in value-added. Achieving this renaissance will require action by firms and the government, some of which we will outline below. But firms here begin with a key asset—having the United States as “home market.” The U.S. consumer market is large, rich, diverse, and dynamic. The United States has no peer for attracting capital from home and abroad; moreover, its goods producers are “battle-tested,” with lean, competitive operations required for success in the world of global supply networks. Furthermore, the United States boasts the most innovative, competitive services market on the planet and is home to 45 of Reuters’ Top 100 global technology leaders (Japan, in second place, has 13) (4).

Capturing the new opportunities will not be easy. The manufacturing sector needs new capabilities. More firms need to participate in the global economy, since technology and demand growth have enhanced opportunities abroad. Many plants need to be upgraded for digital readiness; firms, focused on survival the last 20 years, now must step up to keep pace with capital requirements. For example, large investments are needed to close the gap in robotics, where the United States has a relatively low implementation intensity when compared to Japan, Germany, and South Korea. Moreover, shorter product cycles and faster discovery will require firms to “compete against time.” Considering human resources, the entire goods-producing sector will need people with higher skills, which will stretch the existing education and training infrastructure. Therefore, firms will need to redouble efforts to attract and retain skilled workers.

Tax and Regulatory Policy—So Far, So Good

The Trump administration and Congress have made substantial progress in both boosting economic growth and improving competitiveness, especially in manufacturing. The Tax Cuts and Jobs Act (Public Law 115-97), enacted in December 2017, lowered corporate marginal tax rates from 35 percent to 21 percent, near the average of industrial economies. The new law also moved the U.S. system to territorial taxation and provided for immediate expensing of capital investment—changes which are accelerating capital flows into the United States and, by extension, manufacturing productivity. Less visible but just as important has been regulatory reform, which reversed the direction of the previous administration. President Trump set a goal of repealing two regulations for each one implemented, and thus far the new administration is exceeding this pace (5). In partnership with Congress, reducing the burden of regulation has translated directly into higher business confidence as well as an improved operating environment supportive of new investment.

These improvements come at a moment when global demand is rising, and technology is driving value chain evolution in the direction of U.S. advantage. Favorable changes to energy costs and labor productivity (relative to global competition) can be expected to add a tailwind to the growth scenario. Pro-growth policies appear to be working well, with the economy registering 4.1 percent GDP growth in the most recent quarter and unemployment reaching multi-year lows.

Trade and Infrastructure—To Be Determined

Candidate Trump made a confrontational trade policy focused on reciprocity as a core campaign message. Thus far, the president has shown resolve, with a willingness to use the blunt instrument of tariff escalation to reset what he perceives as arrangements unfair to the United States. As of now, the macroeconomic effects of higher tariffs are small in comparison to the stimulus associated with tax reform, but U.S. actions and retaliation by trading partners are causing headaches for those who manage manufacturing supply networks. A reset of U.S.-China commercial relations is overdue, and the president has public support for this fight. However, with over half of U.S. imports composed of intermediate goods (i.e., things used to make other things), most producers hold out hope for a speedy resolution of disputes with key partners like Canada, Japan, Mexico, and the European Union, where the administration’s claims of “unfairness” are more difficult to square with the facts.

Improving U.S. infrastructure was another frequent campaign theme. In February 2018, the president proposed a creative approach to infrastructure development, utilizing grants to incentivize public-private partnerships along with reforms in permitting, credit guarantees, and asset management. Congress has not yet acted on this initiative and is now likely delayed until after the midterm elections.

Makers: Remaking for Success

Looking ahead, it is reasonable to be confident in the future of U.S. manufacturing. Key factor endowments remain highly favorable: plentiful domestic energy supplies, a dynamic home consumer market, a skilled workforce, and economic circumstances supportive of investment.

Tax and Regulatory Policy—So Far, So Good

The Trump administration and Congress have made substantial progress in both boosting economic growth and improving competitiveness, especially in manufacturing. The Tax Cuts and Jobs Act (Public Law 115-97), enacted in December 2017, lowered corporate marginal tax rates from 35 percent to 21 percent, near the average of industrial economies. The new law also moved the U.S. system to territorial taxation and provided for immediate expensing of capital investment—changes which are accelerating capital flows into the United States and, by extension, manufacturing productivity. Less visible but just as important has been regulatory reform, which reversed the direction of the previous administration. President Trump set a goal of repealing two regulations for each one implemented, and thus far the new administration is exceeding this pace (5). In partnership with Congress, reducing the burden of regulation has translated directly into higher business confidence as well as an improved operating environment supportive of new investment.

These improvements come at a moment when global demand is rising, and technology is driving value chain evolution in the direction of U.S. advantage. Favorable changes to energy costs and labor productivity (relative to global competition) can be expected to add a tailwind to the growth scenario. Pro-growth policies appear to be working well, with the economy registering 4.1 percent GDP growth in the most recent quarter and unemployment reaching multi-year lows.

Trade and Infrastructure—To Be Determined

Candidate Trump made a confrontational trade policy focused on reciprocity as a core campaign message. Thus far, the president has shown resolve, with a willingness to use the blunt instrument of tariff escalation to reset what he perceives as arrangements unfair to the United States. As of now, the macroeconomic effects of higher tariffs are small in comparison to the stimulus associated with tax reform, but U.S. actions and retaliation by trading partners are causing headaches for those who manage manufacturing supply networks. A reset of U.S.-China commercial relations is overdue, and the president has public support for this fight. However, with over half of U.S. imports composed of intermediate goods (i.e., things used to make other things), most producers hold out hope for a speedy resolution of disputes with key partners like Canada, Japan, Mexico, and the European Union, where the administration’s claims of “unfairness” are more difficult to square with the facts.

Improving U.S. infrastructure was another frequent campaign theme. In February 2018, the president proposed a creative approach to infrastructure development, utilizing grants to incentivize public-private partnerships along with reforms in permitting, credit guarantees, and asset management. Congress has not yet acted on this initiative and is now likely delayed until after the midterm elections.

Makers: Remaking for Success

Looking ahead, it is reasonable to be confident in the future of U.S. manufacturing. Key factor endowments remain highly favorable: plentiful domestic energy supplies, a dynamic home consumer market, a skilled workforce, and economic circumstances supportive of investment.

With the right policy decisions, the United States can expect manufacturing GDP growth well above the current trend, spurring income growth, employment, and positive-sum secondary effects. The critical element for both business and political leaders is to focus on the future instead of trying to recreate the past.

REFERENCES

1. Sree Ramaswamy et al., “Making it in America: Revitalizing U.S. Manufacturing,” (McKinsey Global Institute, November 2017), click here.

2. Richard Baldwin, “The Great Convergence: Information Technology and the New Globalization,” (Belknap Press of Harvard University Press, 2016), click here.

3. Stephen J. Ezell, “A Policymaker’s Guide to Smart Manufacturing,” (Information Technology and Innovation Foundation, November 2016), click here.

4. Click here.

5. For up-to-date information about regulatory reform, click here.

Scott Miller is a senior adviser with the Abshire-Inamori Leadership Academy at the Center for Strategic and International Studies in Washington, D.C.

The Center for Strategic and International Studies (CSIS), a private, tax-exempt institution focusing on international public policy issues. Its research is nonpartisan and nonproprietary. CSIS does not take specific policy positions. Accordingly, all views, positions, and conclusions expressed in this publication should be understood to be solely those of the author(s).

With the right policy decisions, the United States can expect manufacturing GDP growth well above the current trend, spurring income growth, employment, and positive-sum secondary effects. The critical element for both business and political leaders is to focus on the future instead of trying to recreate the past.

REFERENCES

1. Sree Ramaswamy et al., “Making it in America: Revitalizing U.S. Manufacturing,” (McKinsey Global Institute, November 2017), click here.

2. Richard Baldwin, “The Great Convergence: Information Technology and the New Globalization,” (Belknap Press of Harvard University Press, 2016), click here.

3. Stephen J. Ezell, “A Policymaker’s Guide to Smart Manufacturing,” (Information Technology and Innovation Foundation, November 2016), click here.

4. Click here.

5. For up-to-date information about regulatory reform, click here.

Scott Miller is a senior adviser with the Abshire-Inamori Leadership Academy at the Center for Strategic and International Studies in Washington, D.C.

The Center for Strategic and International Studies (CSIS), a private, tax-exempt institution focusing on international public policy issues. Its research is nonpartisan and nonproprietary. CSIS does not take specific policy positions. Accordingly, all views, positions, and conclusions expressed in this publication should be understood to be solely those of the author(s).

© 2018 by the Center for Strategic and International Studies. Used with permission.