Bio-lubricants: Global opportunities and challenges

Sharbel Luzuriaga | TLT Market Trends December 2017

The five-year forecast is 5% growth with the U.S. and Europe providing the greatest demand.

To protect their aquatic inhabitants, ponds need pumps that use bio-lubricants.

www.canstockphoto.com

KEY CONCEPTS

•

Bio-lubricants comprised roughly 1% of total finished lubricants in 2016.

•

For years bio-lubricant demand was driven largely by legislative mandates.

•

Today end-users also expect bio-lubricants to deliver superior energy efficiency and prolonged machine lifetime.

THE GLOBAL FINISHED LUBRICANT MARKET GROWTH IS SLOW AT BEST, but increasing environmental- and climate-protection directives are ensuring robust demand in a handful of high-growth, specialty-product categories. Bio-lubricants is one of those fast-evolving markets, and according to Kline’s most recent findings will soon become a high-value niche market.

Bio-lubricants are used not only in applications with high probability of total or accidental exposure of lubricants to sensitive environment but also in applications where bio-lubricants contribute to environmental quality indirectly by improving an existing benefit or reducing pollution and emission levels.

Bio-lubricant demand has been driven primarily by legislative mandates, notably in environmentally sensitive and low-severity applications where vegetable oils such as canola oil (but also soybean and sunflower oils) meet the required criteria for biodegradability, low toxicity and bioaccumulation. Regulatory-driven demand, serious performance drawbacks and higher pricing are among the factors limiting bio-lubricants to a few niche applications in forestry and agricultural.

Today the increased supply of new-generation, high-performing and more cost-competitive green synthetic bio-base stock technologies is helping to reconcile sustainability, cost and performance.

A REGULATION-DRIVEN MARKET

On the regulatory front, the U.S. and Europe are the most progressive regions, having implemented mandatory and voluntary schemes promoting the use of products and services with a lower environmental impact during their entire service lifetime. The most impactful regulation in North America is the Vessel General Permit (VGP). Europe has the EU Ecolabel, a platform largely based on existing ecolabels of individual European countries, namely: Germany (Blue Angel), the Netherlands (VAMIL Regulation) and Sweden (Swedish Standard).

The EU Ecolabel and the VGP are due to be reviewed next year. The EU Ecolabel will be reviewed by an ad-hoc working meeting committee consisting of EU authorities but also such industry stakeholders as bio-lubricant blenders, base stock and additives suppliers and OEMs.

This event has created high expectations among industry participants on how potential modifications will impact the uptake of synthetic bio-base stocks and ultimately bio-lubricant products. In regard to VGP, the main change is related to extending the list of VGP-compliant vessels to include vessels smaller than 79 feet or 24 meters in length. However, according to industry experts, the VGP will most likely remain unchanged. Conversely, the EU Ecolabel scheme might be subjected to major adjustments in an attempt to inject momentum to the commercial viability of the EU Ecolabel products in Europe.

End-use industries are keen to adopt high-quality lubricants with superior performance reflected in energy efficiency and prolonged lifetime of lubricants and machines. Although environmental responsibility and public perception are important, these aspects are assigned a secondary priority. More tangible efforts, such as balancing price, performance and sustainability, are needed if the EU Ecolabel is set to reach a broader range of end-users.

A common belief is that authorities are interested in stricter criteria such as minimizing the use of substances (including lubricant additives such as extreme pressure, corrosion inhibitors and biocides) that contain toxic characteristics needed to achieve performance requirements. True, but regulators also are imposing stricter renewability criteria. There are indications that the 25%-50% renewable content will be increased to 60% or even 80%. This will eliminate petrochemical synthetic base stock from the bio-lubricants market while benefiting bio-synthetic base stock and oleochemical synthetic esters.

Today a holistic approach is being taken as the entire lifecycle of a bio-lubricant is being assessed, including the environmental impact of bio-lubricants during manufacturing, use and disposal. Special emphasis is being placed on automotive engine oils.

NORTH AMERICA AND EUROPE

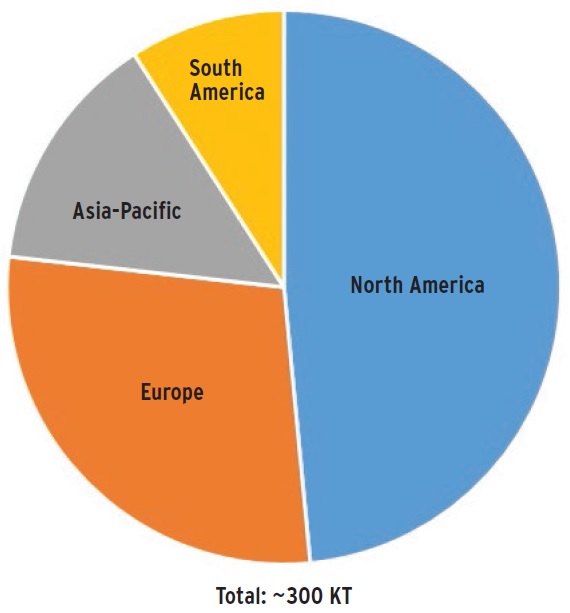

North America and Europe are the prime consumers of bio-lubricants by virtue of stringent environmental protection policies, including the EU Ecolabel and VGP, but also due to heightened environmental awareness among end-users. Together the two regions account for approximately 80% of the global market. Asia-Pacific, a region lagging in terms of bio-lubricants uptake, is rapidly becoming a key market for bio-lubricant products (

see Figure 1).

Figure 1. Global bio-lubricant consumption by region, 2016.

Figure 1. Global bio-lubricant consumption by region, 2016.

The U.S. is the largest consumer of bio-lubricants in the world, followed by Germany. Other important country markets include South Korea, Brazil, Canada and the Nordic countries (including Sweden, Denmark, Norway and Finland).

CONSUMPTION BY PRODUCT AND APPLICATION

Hydraulic fluids is the leading product category, followed by metalworking fluids and chainsaw oils, transformers oils, gear oils, automotive engine oils and greases. Minor bio-lubricant product categories include mold releasers, notably concrete releasers used in construction, but also spindle oils used in the textile industry, and wire rope lubricants used in cranes, shovels, elevators and suspension bridges, among others.

Bio-hydraulic fluids include mobile applications in the construction and mining sectors but also in agriculture and forestry. In stationary applications, hydraulic fluids are used mainly in machine tools and general manufacturing.

Metalworking fluids are used in the primary metals, automotive manufacturing (OEMs) and general manufacturing sectors. Although some neat and water-miscible metalworking fluids fulfill biodegradability and renewability criteria, as they are based on vegetable oils and synthetic esters, they have not yet been integrated under the EU Ecolabel umbrella. This is largely because of the content of hazardous chemical substance used in the formulation of metalworking fluids. During the past 10 years, the content level of these molecules were significantly reduced due to the effect of a series of regulations, notably REACH and EPA. Nowadays, metalworking fluids are eligible to fulfill the health and safety criteria to be considered as a new EU Ecolabel category.

COMPETITIVE LANDSCAPE

The bio-lubricants market is highly competitive with major oil companies competing with small and medium-sized specialized independent players.

Panolin and Fuchs are the leading suppliers of finished bio-lubricants in Europe and worldwide, driven by their bio-lubricant range and focus, global reach and OEM partnerships. Both companies are directly competing with such global oil majors as BP, Shell, ExxonMobil and Total. The combined Houghton and Quaker Chemical Co. will be the leading metalworking fluids supplier. Quaker Chemical also is active in other bio-lubricant product segments through acquisition activities. Similarly, Fuchs expanded its market presence through acquisitions. In 2015 Fuchs acquired Statoil’s Fuel and Retail Lubricants business, while Binol, a leading player in the Nordic bio-lubricants market, was acquired by Quaker Chemical.

HIGH GROWTH, REGIONAL DISPARITIES

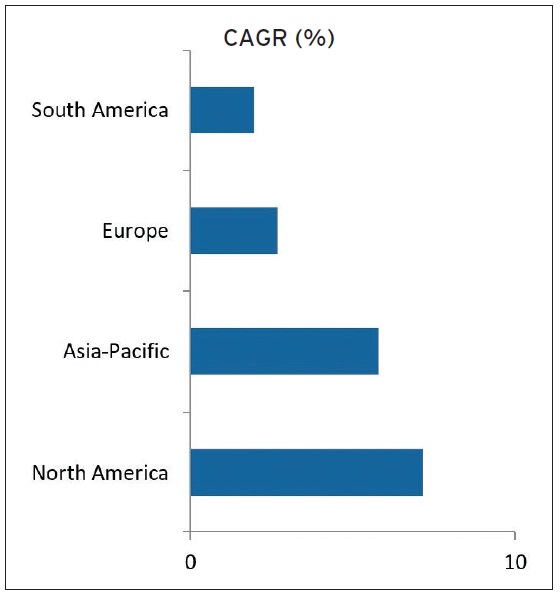

Bio-lubricants constitute a small fraction of the global finished lubricants market, roughly estimated at around 1% of total finished lubricants in 2016. However, the growth rate for bio-lubricants is forecast to outpace the growth for finished lubricants (

see Figure 2).

Figure 2. Global outlook demand for bio-lubricants by region, 2016 to 2021.

Figure 2. Global outlook demand for bio-lubricants by region, 2016 to 2021.

Kline estimates the bio-lubricants market will grow at a compound average growth rate of 5% during the next five years.

However, growth rates of bio-lubricants vary by region. North America and the Asia-Pacific region are projected to exhibit growth rates above the global average, while Europe and South America will experience growth below 5%.

Regulation can be a prelude to growth, with an incentive for blenders to develop relevant products and customer interest, especially when mineral lubricants continue to have significant cost advantage over bio-lubricants. However, regulation by itself, without the relevant enforcement, attractive product offerings in terms of price and performance and dedication, will not drive the sector.

The EU Ecolabel platform has been successful in enhancing the environmental performance of organizations, as well as promoting products with a reduced environmental impact. However, this contribution is still significantly limited due to persistent low awareness among market stakeholders, including distributors, end-users and even authorities.

There are serious challenges to overcome to convince OEMs and lubricant formulators on key aspects, such as reliability and consistency of supply, compliance with all specifications and standards. Overcoming these challenges will help drive strong growth in this exciting market.

Sharbel Luzuriaga is a project manager at Kline & Co. in the Energy practice. He is based in Kline’s Prague office in the Czech Republic. You can reach him at Sharbel.Luzuriaga@klinegroup.com

Sharbel Luzuriaga is a project manager at Kline & Co. in the Energy practice. He is based in Kline’s Prague office in the Czech Republic. You can reach him at Sharbel.Luzuriaga@klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries including lubricants and chemicals. Learn more at www.klinegroup.com.