Why synthetics are leading the lubricants market

David Tsui | TLT Market Trends June 2017

Once viewed as strictly premium products, these lubes are rapidly gaining a broader appeal.

© Can Stock Photo / nanDphanuwat2526

KEY CONCEPTS

•

At 3.5 million tons annually, synthetics represent 10.5% of the total lubricants market, excluding process oils.

•

OEMs, government regulation, ample base stock supply and consumer preferences are powering the demand for synthetics.

•

While interest in synthetics is broadening worldwide, so too is the competition to bring them to market.

THE GLOBAL FINISHED LUBRICANTS MARKET has been relatively flat for more than a decade with a compound annual growth rate of 0.2% during the 2005-2016 period, holding steady at just under 39 million tons (including process oils) last year. Yet lubricant marketers and suppliers are tasked to grow year on year. How can a company meet growth expectations when volumes in major markets are flat? The solution may come from the synthetic lubricants segment.

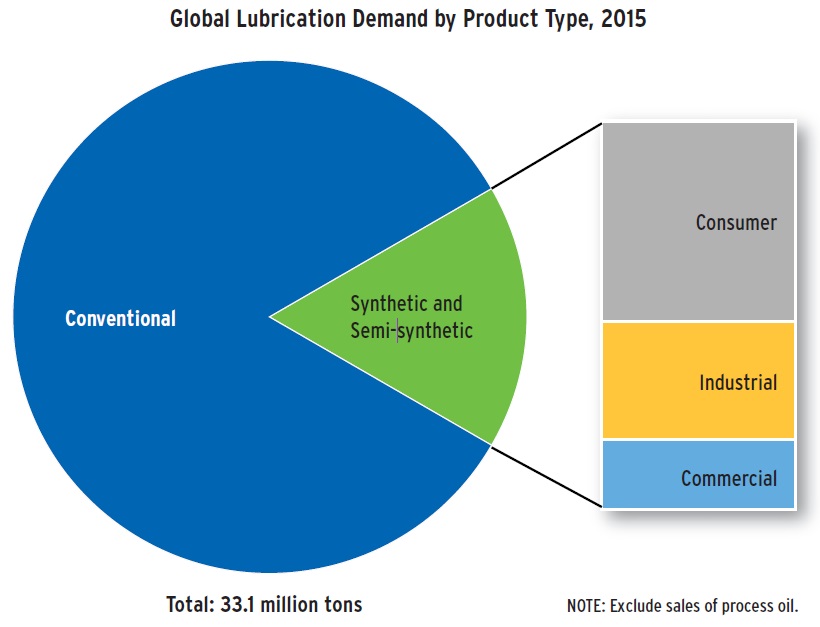

Kline estimates that the global synthetic lubricants market is 3.5 million tons annually, representing 10.5% of the total market excluding process oils. Semi-synthetic lubricants account for a further 2.1 million tons, representing 6.3% of the total market in 2015 (

see Figure 1).

Figure 1. Kline estimates that the global synthetic lubricants market is 3.5 million tons annually.

Figure 1. Kline estimates that the global synthetic lubricants market is 3.5 million tons annually.

The use of the terms synthetic and semi-synthetic in this article are not based on the base stock, chemistry or molecules but, rather, how the products are marketed, positioned, priced and accepted by end-users. Synthetic products include API Group III-based products.

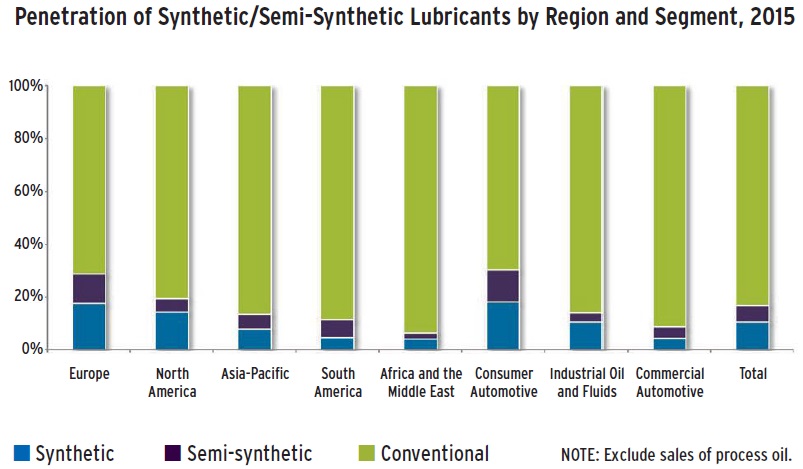

Synthetic lubricant penetration varies significantly by region and product categories. Europe has the highest PCMO synthetic penetration due to OEM technical demand in premium/mass market vehicles, consumer demand for extended oil drain intervals (ODIs), improved fuel economy, lower vehicle emissions and hardware compatibility. North America is second with OEM technical demand, changing preferences for longer ODIs and low price sensitivity. Asia-Pacific is third with higher penetration in South Korea and Japan, though China and India are rapidly advancing with growing consumer awareness of synthetics. South America, Africa and the Middle East trail as OEM technical demand gains traction. By category, consumer automotive has the highest synthetic penetration due to OEM technical demand, consumer awareness and lower price sensitivity. Commercial automotive has the lowest penetration of synthetic lubricants due to the high price sensitivity of commercial fleets and lower OEM technical demand. Industrial falls in the middle, with some specialty applications almost exclusively utilizing synthetic lubricants along with many other general industrial applications exclusively using conventional lubricants.

The growth in the synthetics market segment has been outpacing the overall lubricants market growth in all regions. The synthetic lubricants segment accounted for 17% of the overall lubricants market in 2015 and for 30% of the consumer automotive segment in the same year (

see Figure 2); both are up 4% from 13% and 26%, respectively, in 2013. This is due to growth in synthetic lubricant consumption during this period and a decline in the overall lubricants volume, which declined 1.7% since 2013.

Figure 2. The growth in the synthetics market segment has been outpacing the overall lubricants market growth in all regions.

Figure 2. The growth in the synthetics market segment has been outpacing the overall lubricants market growth in all regions.

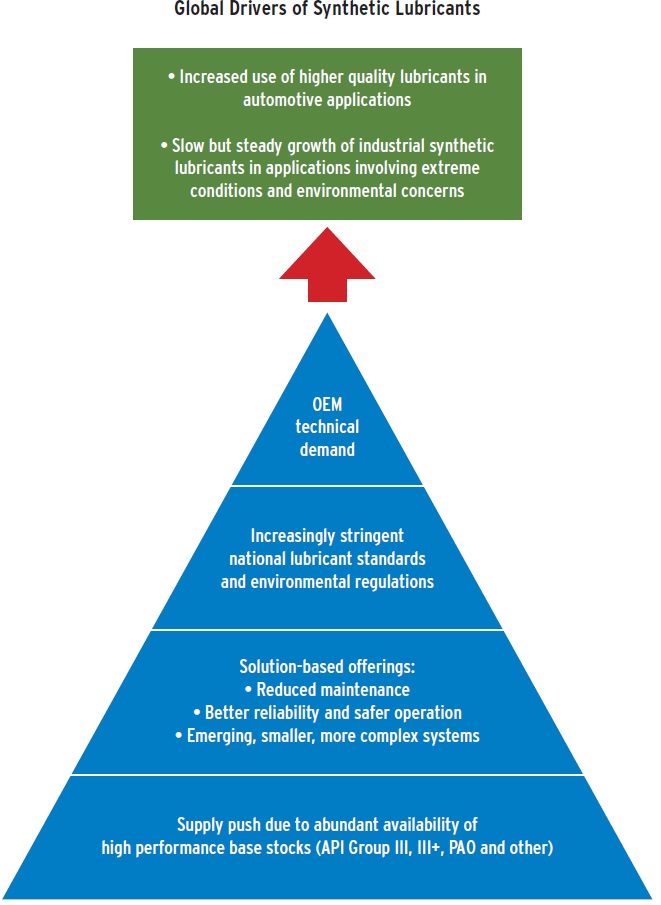

What is behind this growth in synthetics? In Kline’s view, OEM requirements, government regulations, increasing synthetic base stock supply and consumer preference all have played a part (

see Figure 3).

Figure 3. Factors behind the growth in synthetics.

OEMS DRIVING LUBRICANT UPGRADE

Figure 3. Factors behind the growth in synthetics.

OEMS DRIVING LUBRICANT UPGRADE

OEMs are driving the trend toward synthetic lubricants in engine and power train applications, as well as in some industrial applications. Governments have been increasingly pressuring OEMs to create more energy and environmentally friendly equipment, while consumers have been demanding more powerful and reliable equipment. OEMs have responded with technological advances in equipment design, creating lighter engines with much higher power density, power trains with 10-speeds or more and designing manufacturing equipment for even faster production rates.

These advanced designs require advancements in lubricants to enable these new engines, power trains and equipment to operate at their peak efficiency for the life of the equipment. OEMs have been actively working with lubricant marketers to co-develop tailored products for these new applications and also have promoted more stringent lubricant standards through industry bodies, such as ACEA, ILSAC, API, JASO, as well as through their own OEM standards such as GM dexos®.

GOVERNMENT REGULATION

These emerging next-generation, global-quality specifications, particularly on automotive engine oils, have been influenced by tighter fuel economy and emissions regulations in the top three major markets. These will be key drivers of synthetics demand in different parts of the world as these specifications tend to trickle down to all markets.

The next quality category for PCEO in the U.S., ILSAC GF-6, likely will be introduced in 2019 and will feature a GF-6B ultra-low viscosity sub-segment geared toward fuel economy. ACEA 2016 has already been introduced and also carries a new C5 low-viscosity fuel economy subcategory. HDEO launched the PC-11 category in December 2016, which also has a low-viscosity fuel economy subcategory, FA-4. These new categories require lubricants to have significantly better performance properties than previous specifications and bring the lubrication dynamics closer to a boundary friction region where fluid film and additive chemistry will play a much more crucial role in protecting the metallurgy.

In addition to the fuel economy regulations, in Europe environmental protection legislation has tightened specifications on exhaust emission for passenger cars and commercial vehicles. In European Union (EU) countries, the European Commission has enforced the Euro VI standards for passenger cars and heavy vehicles. Emission standards also are tightening in parts of Asia-Pacific. In countries like China and India, vehicle emission standards are being upgraded to BS VI (Euro VI)/Standard V. In Japan the “post-new long-term regulations” released in 2009 have an emission standard level of close to Euro VI. In South Korea, in September 2015, all passenger cars, SUVs and minivans were required to meet the Euro VI norms.

These emissions regulations will require more extensive exhaust after treatment, which is sensitive to metal or ash content in lubricants. This metal or ash content comes from the additives designed to protect not only the metal surfaces from deposits and wear but also the base oil from degradation. As a result, the metal/ash content in lubricants is being reduced to protect emissions systems, which will further the need for synthetic lubricants as synthetic base oils are more resistant to degradation and thermal breakdown.

GROWING SUPPLY OF GROUP III/III+

Growth in supply of API Group III/III+ base stocks, the leading base stock type for formulating synthetic lubricants, will be a major volume driver of synthetic/semi-synthetic lubricants. The supply of API Group III/III+ base oils has increased from 7% of the total base oil supply in 2007 to 14% in 2015, with the industry facing an oversupply at present. As a result, Group III base stocks have to compete with Group II base stocks in many applications, bringing downward pressure on its price. Group III prices are the lowest in Asia-Pacific, as Asia is a key global supplier of this product.

The technical demand for Group III/III+ base stocks in the finished lubricant market exists in low-viscosity grades of PCMO and HDMO, low-viscosity ATF, general industrial oils offering low-temperature performance, and lubricants with a synthetic claim. However, due to current oversupply, Group III/III+ base stocks are experiencing a marketing push in finished lubricant products such as mid-viscosity PCMO and HDMO grades where Group II can be used, based on improved performance claims. Synthetic base stocks, such as PAOs, are used to blend ultra-high-performance automotive engine oils, such as PCMO 0W-30/20/16, synthetic gear oils and synthetic industrial lubricants. The supply of PAOs has increased by nearly 20% between 2011 and 2014, although that growth has slowed. Group III+ base stocks are technically suitable to replace PAOs in most applications. However, the currently limited availability of Group III+ in the merchant market is driving the demand for more expensive PAOs.

On the supplier front, synthetic penetration is growing among mid-tier and lower-tier suppliers as well as retailers and installers choosing to market their own brands of synthetics in direct competition to those from the leading established market players. This will result in the dilution of the synthetics aura, perhaps leading to a lower price premium compared to conventional lubricants. Overall, synthetic lubricants are transitioning from premium products to products with a broader appeal, with the category no longer the domain of global major oil companies. With competition fierce in this segment, it is becoming more important to educate consumers about the differences between various synthetic lubricants.

Synthetic base stocks come in many forms and from many sources. Some provide better low-temperature properties while sacrificing oxidative stability while others provide both excellent oxidative stability and low-temperature performance, sacrificing solvency and seal compatibility. With the vast differences between types of base stocks, synthetic base stocks can be used by lubricant marketers as a reason-to-believe for consumers. Examples include Valvoline’s NextGen base on re-refined oil, Shell’s Pennzoil Platinum PurePlus based on gas-to-liquid technology and BP’s Castrol EDGE Bio-Synthetic based on plant material. With various sources of synthetic base oils available, base oil suppliers and lubricant marketers can find differentiation within base oils as well as the final product. This will help in expanding the high performance lubricant market, including synthetic lubricants.

CHANGING CONSUMER PREFERENCES

Commercial fleets, manufacturers and consumers share a common desire when it comes to their lubricants—less is more. Ideally lubricants would be fill for life or provide long enough service life that maintenance would be effortless. Commercial fleets and manufacturers are facing the same economic situation with the world digging out from a recession. All efforts are on keeping equipment running as long as possible and reducing maintenance costs. The new generation of consumers is viewing vehicles as a mode of transportation and as such wish to spend as little time as possible in the care and maintenance of the vehicle. These trends are likely to increase the use of synthetic lubricants, which can offer longer service life and potentially reduce overall maintenance costs.

SOLITARY BRIGHT SPOT

Kline projects the synthetic lubricants market will grow at a compound annual growth rate of 6.2% and account for nearly 22% of the overall lubricants market by 2020. Capturing a share of this growing segment will be difficult as competition is heating up. Lubricant marketers will need to understand their consumers better and communicate the benefits and differences of synthetic lubricants, not only versus conventional fluids but versus other synthetic products.

David Tsui is a Project Manager at Kline & Co. in the Energy practice. You can reach him at david.tsui@klinegroup.com

David Tsui is a Project Manager at Kline & Co. in the Energy practice. You can reach him at david.tsui@klinegroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries including lubricants and chemicals. Learn more at www.klinegroup.com.