India’s winning strategy

Milind Phadke | TLT Market Trends April 2017

Growth opportunities continue for the world’s third-largest consumer of finished lubricants.

© Can Stock Photo / snehitdesign

KEY CONCEPTS

•

In 2016 India accounted for about 6% of global lubricants demand, ranking it third worldwide behind the U.S. and China.

•

In the last few years, India’s overall lubricant demand has slowed due to decreases in the commercial and industrial segments.

•

The overall lubricant demand in India is expected to grow at 2.5% through 2021.

THE INDIAN MARKET has been one of the global lubricants industry’s growth engines. In 2016 India accounted for about 6% of the global lubricants demand, making it the third-largest market behind the U.S. and China. Of the BRIC countries (Brazil, Russia, India and China) touted as growth markets, only India continues to hold the promise of growth. However, even in India, technology, the economy and regulations have subdued growth while at the same time driving an improvement in lubricant quality. This article provides a snapshot of the Indian lubricants market and speculates how it will evolve.

In 2015 the Indian economy stood at $8.7 (

1) trillion (U.S. dollars) with a per capita GDP of $6,700 (U.S.). Unlike China and other export-oriented economies of Asia, economic growth in India is driven primarily by domestic consumption rather than by exports or investment spending. For example, Indian household consumption accounts for nearly 60% of GDP. In contrast, household consumption accounted for about 38% of the Chinese economy. As a result, India was fairly insulated from the adverse impacts of the global recession in 2008.

The subsequent contraction in energy prices has had a huge positive impact on the India economy given that India is a significant importer of crude oil. The reduction in the crude oil import bill has provided the government some maneuvering room to address its budget deficit and pursue new programs. As a result, the economic growth rate strengthened from 6.6% in 2011 to 7.6% in 2015. Despite a strengthening of the economic growth rate, finished lubricant demand slowed from 4.7% in 2011 to 1.1% in 2015. What is happening?

MARKET SLOWDOWN

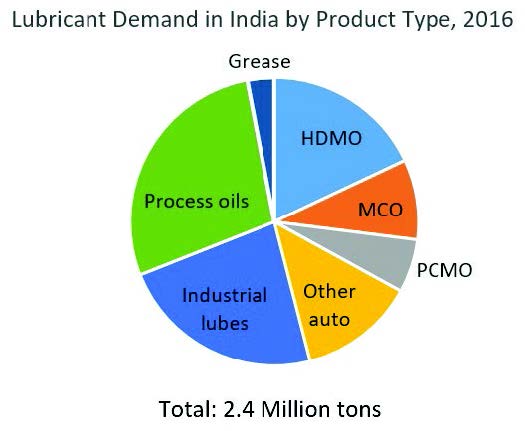

The Indian lubricant market is estimated at about 2.4 million tons, including process oils (

see Figure 1). Industrial fluids, including process oils, general industrial oils, industrial engine oils and metalworking fluids, account for about 50% of the total demand. On the automotive side, heavy-duty motor oils (HDMO) is the largest product category, accounting for under 20% of the total market, while motorcycle oils (MCO) and passenger car motor oils (PCMO) together account for 15% of the total market.

Figure 1. Overall lubricant demand in India has slowed down due to a decrease in the commercial and industrial segments.

Figure 1. Overall lubricant demand in India has slowed down due to a decrease in the commercial and industrial segments.

In the last few years, overall lubricant demand has slowed due to a decrease in the commercial and industrial segments. Key commercial lubricant sectors such as mining have contracted due to the cancellation of mining contracts by the government. Only the consumer segment (covering motorcycles, passenger cars and taxis) exhibited some growth. Between 2010 and 2015, sales of motorcycles, scooters and passenger cars grew at 4%, 20% and 8% per year, respectively. During the same period, sales of commercial vehicles (including trucks and buses) grew at 0.6%. As only 15% of the market (including PCMO and MCO) is exhibiting some growth and the rest of the market is flat, the overall lubricant demand growth has slowed considerably during the last few years. Besides economic factors, quality improvements and extension of drain intervals also have played their part in dampening lubricant demand growth.

LUBRICANT QUALITY EVOLUTION

The overall penetration of synthetic and semisynthetic lubricants in India is just under 6%. The penetration of synthetics is highest in the consumer segment.

Consumption of synthetic PCMO and passenger car diesel oil (PCDO) is estimated to be 25% despite the price-sensitive nature of consumers. Synthetic and semisynthetic lubricants are catching up fast among economy and mid-tier car OEMs due to the high-performance requirement in new cars. Up until the last decade, Indian OEMs such as Tata Motors and Maruti did not endorse the use of synthetic lubricants. Some oil companies have partnered with OEMs of premium cars for the use of synthetic engine oils and ATF. The authorized service centers of these OEMs recommend synthetics.

Today, most of the new models introduced by Indian OEMs also recommend the use of synthetics. For example, synthetic SAE 5W-30 is commonly used both in factory and service fill of Maruti Suzuki and Hyundai cars. SAE 5W-40 penetration is very small compared to 5W-30, as they are expensive and used mainly in luxury cars from such OEMs as Mercedes-Benz, BMW and Volkswagen. Some OEMs have now started to recommend SAE 0W-20 grade. For instance, Maruti Swift and Ciaz cars in petrol versions have a recommendation of using 0W-20. In partnerships with OEM, oil companies are promoting synthetic grades for use in small and midsized cars. Besides OEM partnerships, lubricant marketers also are working at increasing consumers’ and mechanics’ awareness of the benefits of using synthetic products. Indicative of the synthetic growth potential in the consumer segment is the fact that penetration of 5W-xx and 0W-xx grades will grow from 25% of total in 2016 to 35% by 2021.

Unlike the consumer segment, in the commercial on-highway segment there is minimal use of synthetic lubricants. All the major OEMs, such as Tata, Ashok Leyland and Eicher, recommend conventional engine oil. Tata Motors, the largest player in the on-highway commercial segment, recommends oils meeting the API CH-4 service category. For this category, there is no real requirement for synthetic oils. The use of synthetics is done solely at the end-user’s discretion. However, the higher price of synthetic lubricants is a significant deterrent in their use. In contrast, in the commercial off-highway segment, there is a growing use of synthetics in mining and construction fleets. Unlike the consumer segment, there is no significant shift to lighter viscosity grades. HDMO demand will continue to be dominated by 15W-xx and 20W-xx grades for the foreseeable future, dampening the potential for synthetic products.

In its efforts to contain a growing pollution, the Indian government has issued notifications for the implementation of Bharat Stage VI (BS-VI) standards. BS norms are equivalent to corresponding Euro norms but applied with a time lag. Presently, BS-IV norms are followed in 13 major Indian cities while the rest of the country practices BS-III norms. Under the notification issued in 2016, India will directly leapfrog from BS-IV norms to BS-VI by 2020. While the quality of fuel (conforming to BS-VI quality) and changes to vehicle’s hardware (for example, use of diesel particulate filter [DPF] and selective catalyst reduction [SCR]) are touted as major means to achieve the stringent norms, lubricant quality will have its own role to play. This implies a greater focus on the use of cleaner lubricants (blended with Group II, III or synthetic base stocks), which have lower sulfur content, and the market will witness rapid movement toward lighter grades such as SAE 5W-xx and 0W-xx.

Finally, in the industrial segment (including process oils), the use of synthetics and semisynthetics is about 3% of total demand. Criticality of operation, cost of equipment downtime, OEM recommendations and product customization can often drive synthetic usage.

MARKET OUTLOOK

India’s economic growth is projected to strengthen from 7% real GDP growth in 2016 to 8% by 2018 (

2), though the demonetization of high-value currency carried out in November 2016 may dampen growth.

Various government programs directed toward infrastructure development (in particular roadways), voluntary fleet modernization program (V-FMP) and development of so-called smart cities will help kick-start growth in the commercial lubricant segment. The Union Ministry of Road Transport, Highways and Shipping in India have announced highway projects in various states to develop land transportation infrastructure. These include investments upward of $11.1 billion (U.S.) in Maharashtra, $8.1 billion (U.S.) in Uttar Pradesh, $2.4 billion (U.S.) in Punjab and $1.6 billion (U.S.) in West Bengal.

The smart cities plan aims to develop infrastructure in cities to cope with the growing urban population in the country. Under this program, selected cities in 22 states of India will be developed as urban settlements to offer hospitable and better structured living conditions for residents.

The mining sector may see a revival in the near future. In 2015 the Indian government implemented a new foreign direct investment (FDI) policy and allocation mechanism to allocate 31 blocks out of 204 blocks with more than 100 more blocks to be auctions in the near future. New mining blocks would mean demand for newer equipment and improved utilization of the existing mining fleet.

Under the proposed V-FMP program, the ministry of road transportation has proposed incentivizing vehicle owners who scrap their old vehicles and purchase newer vehicles. Under V-FMP it is proposed that the vehicles bought before March 31, 2005, or those that are below BS-IV norms, could be scrapped in lieu of which the vehicle owners would receive benefits in the form of scrap value for old vehicle, discounts from OEM for new vehicle and limited exemption from excise duty. However, with the proposed rollout of the new tax regimen—Goods and Services Tax (GST)—in India, there have been some objections to handing out partial excise duty exemption. To date, the ministry of road transport and the finance ministry are ironing out the issues to pave the way for V-FMP. Once this program is implemented, it will help older vehicle fleet (which use heavier monogrades and SAE 20W-40) be replaced by modern vehicle fleet (which use SAE 15W-40 or even 10W-xx grades).

The consumer segment’s growth is driven by the increase in the passenger car and motorcycle population, as well as the rise in small car and two-wheeler exports. On the other hand, the increasing penetration of synthetics and extension of drain intervals will dampen demand growth. The growth of electric scooters and electric cars also will dampen lubricant demand growth.

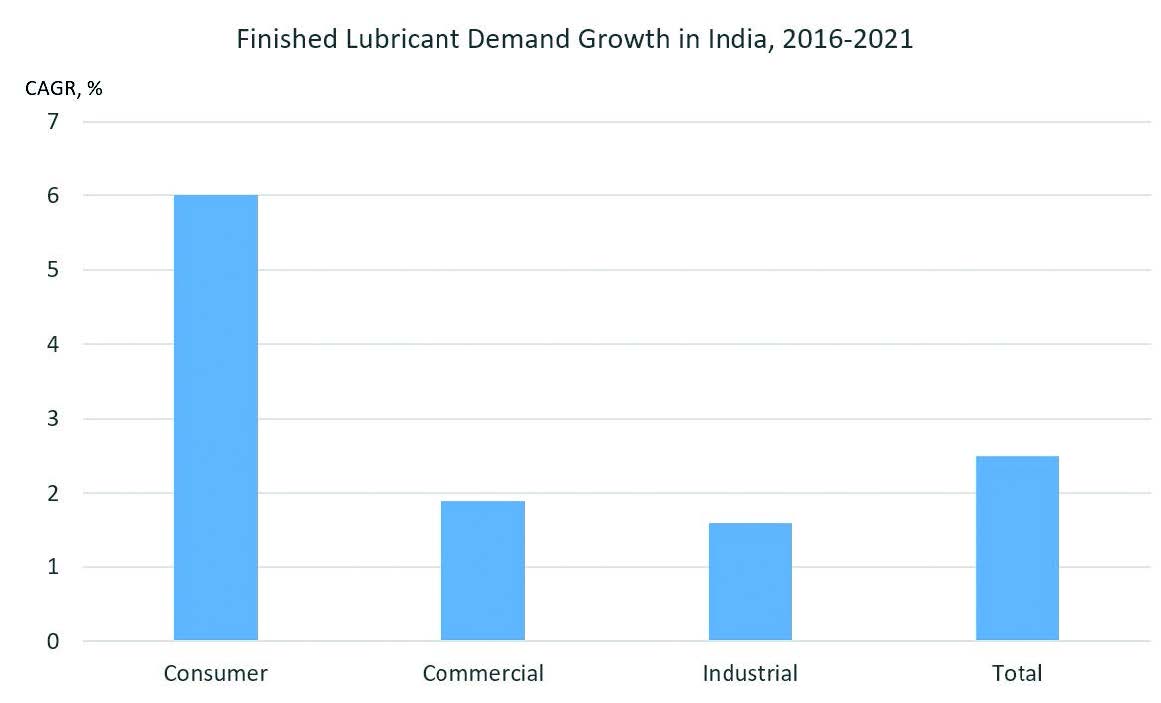

For the industrial sector, lubricant demand will be driven by growth in power generation capacity, as well as growth in the cement and steel industries to support infrastructure development discussed earlier (

see Figure 2). In addition, government initiatives like Make in India also will have a positive impact on demand for industrial lubricants. On the other hand, equipment modernization, use of high-performance lubricants and better maintenance practices (including oil condition monitoring and onsite recycling) will dampen demand growth.

Figure 2. The lubricant demand in India is expected to grow over the next four years.

Figure 2. The lubricant demand in India is expected to grow over the next four years.

As a result of these factors, the overall lubricant demand in India is expected to grow at 2.5% over the period from 2016-2021. This includes strong growth in the consumer segment and low to moderate growth in the commercial and industrial segments. In the PCMO segment, demand will continue to move toward lighter viscosity grades. In the MCO segment, the use of two-stroke oils will decline, and demand for four-stroke oils, in particular 10W-xx grades, will grow. The HDMO market will not see any significant shift in viscosity grades used.

SUMMARY

India continues to present growth opportunities for the finished-lubricants industry. Growing disposable incomes and changing lifestyle needs drive growth in the two-wheeler and passenger car populations. The taxi segment is growing rapidly in metro cities as taxi aggregators proliferate. The concept of bike taxis also is being introduced. Along with the demand growth, there is a remarkable shift toward better quality lubricants in all products in this segment.

Commercial lubricant demand is expected to increase as the various infrastructure initiatives pick up. Engine oil demand will not see much movement beyond 15W-40. Monogrades will decline. Industrial demand relies on the success of various infrastructure and industrial projects. However, any sharp and unexpected change in the global economy and unsuccessful implementation of government projects will have a negative impact on the growth of finished lubricant demand.

REFERENCES

1.

Source: The World Fact Book, CIA. GDP measured at Purchasing Power Parity (PPP).

2.

The Economist Intelligence Unit.

Milind Phadke is a director at Kline & Co. in the Energy practice. You can reach him at Milind.Phadke@KlineGroup.com

Milind Phadke is a director at Kline & Co. in the Energy practice. You can reach him at Milind.Phadke@KlineGroup.com.

Kline is an international provider of world-class consulting services and high-quality market intelligence for industries including lubricants and chemicals. Learn more at www.klinegroup.com.